Coinbase CEO Shares 6 Takeaways From WEF Davos 2026 – Details

While Binance co-founder and former CEO Changpeng “CZ” Zhao made the headlines following his interview at the just-concluded World Economic Forum, where he called a Bitcoin supercycle in 2026, his crypto counterpart and Coinbase CEO, Brian Armstrong, has come forward with feedback from the global event held in Davos, Switzerland.

Coinbase CEO Praises Trump-Led White House As Most Crypto-Forward Government

In a January 24 post on the social media platform X, Armstrong shared a few key “themes and takeaways” from the latest edition of WEF. After admitting that the conference offered a productive time of meeting people one-on-one, the Coinbase CEO revealed that the major focus was on pushing crypto adoption globally.

Starting his list of takeaways, Armstrong highlighted that everyone was talking about tokenization, which is beginning to expand to every asset class in the world. The crypto leader said to expect some major progress in the tokenization sector in 2026, especially as the Fortune 500 business leaders continuously lean in.

Secondly, the Coinbase CEO shared that crypto legislation and the CLARITY Act were another area of focus, as the government of the day looks to make the United States the crypto capital of the world. According to Armstrong, most of the bank CEOs he met at the WEF in the past week are actually pro-crypto.

Armstrong wrote on X:

One CEO of a top 10 global bank told me crypto is their number one priority, and they view it as existential.

Furthermore, the Coinbase CEO lauded the Trump administration as the most crypto-forward government in the world at the moment. Armstrong acknowledged their progress with the crypto market structure, stating that these clear rules are crucial for global competitiveness and will put money back in people’s pockets.

In what seemed like a cheeky tone, Armstrong mentioned that ESG (Environmental, Social, and Governance) and DEI (Diversity, Equity, and Inclusion) topics didn’t come up throughout the forum. According to the crypto founder, the week felt productive, as it centered around real, global progress — all thanks to BlackRock CEO and new WEF co-chair Larry Fink.

The Coinbase leader touted crypto and AI (artificial intelligence) as the most talked-about technologies in today’s world. Highlighting their compatibility, Armstrong stated that AI agents will eventually default to using stablecoins for payments, as they cannot be KYC’d like human beings.

Finally, Armstrong revealed that the Coinbase, Circle, and Bermuda partnership to build a fully on-chain economy was announced at WEF Davos 2026. “Excited to make progress on this and create a compelling case study for other nations to follow,” the crypto CEO concluded.

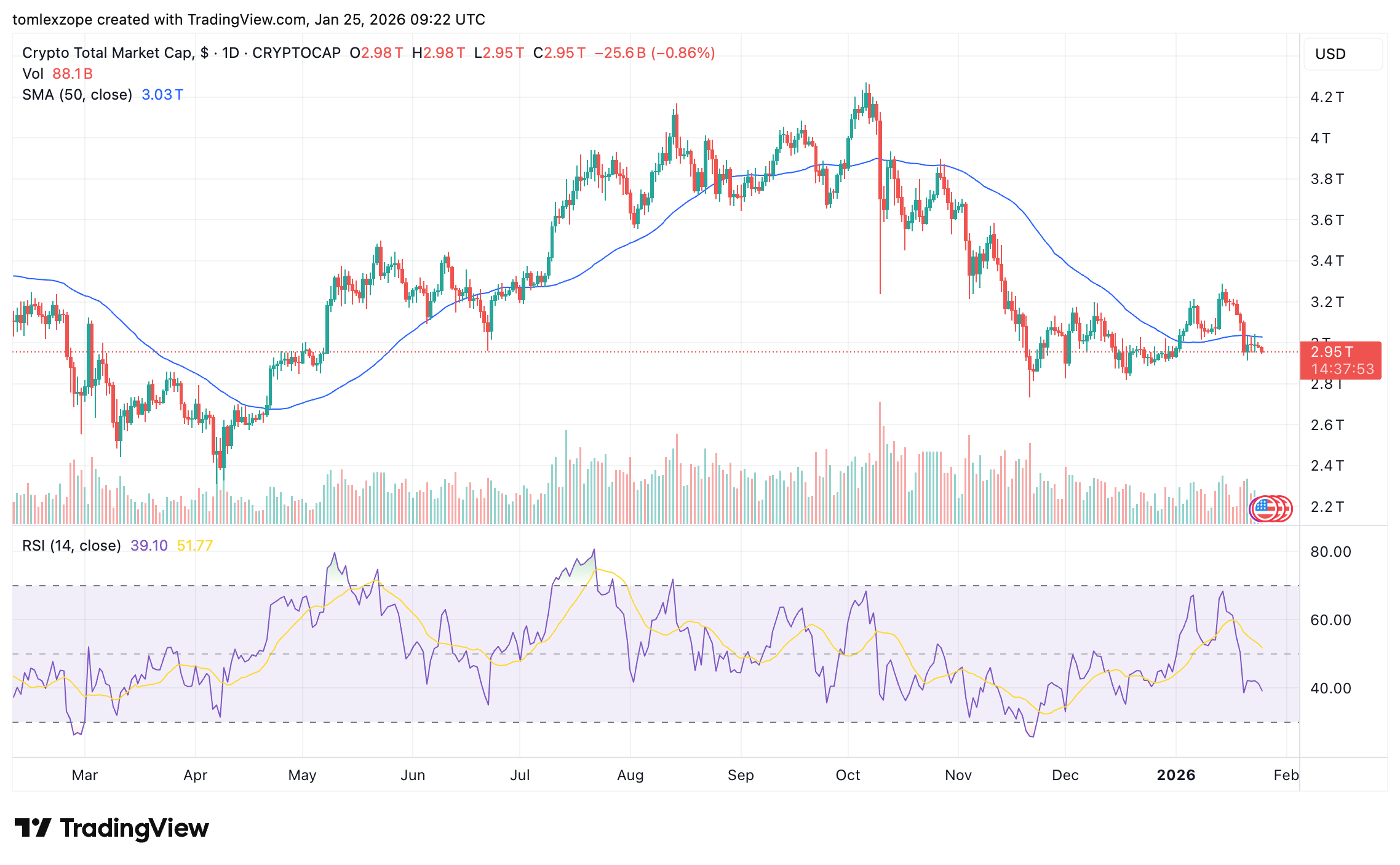

Total Crypto Market Cap At $3.09 Trillion

As of this writing, the global cryptocurrency market has a total capitalization of $3.086 trillion, with Bitcoin retaining its spot as the world’s largest cryptocurrency.

Coinbase rolls out stock trading to select users as CEO Brian Armstrong pursues "everything exchange" vision combining crypto and traditional equities.

Coinbase rolls out stock trading to select users as CEO Brian Armstrong pursues "everything exchange" vision combining crypto and traditional equities.

US Senate Banking Committee postpones Bitcoin and crypto market structure legislation markup after Coinbase and others withdrew their support for the bill

US Senate Banking Committee postpones Bitcoin and crypto market structure legislation markup after Coinbase and others withdrew their support for the bill