Cryptocurrency exchanges are the backbone of the digital asset economy. They enable users to buy, sell, and trade cryptocurrencies securely while supporting liquidity, price discovery, and market growth.

As the crypto market continues to mature, businesses entering this space or scaling existing platforms must make one critical decision early on:

Choosing the right cryptocurrency exchange development company.

Image is created by ChatGPT

The wrong partner can lead to security gaps, scalability issues, regulatory trouble, and delayed launches. The right one accelerates time-to-market, ensures compliance, and builds long-term competitive advantage.

This guide explores what to look for in a crypto exchange development company and why ITIO Innovex is a preferred choice for businesses worldwide.

Understanding Cryptocurrency Exchange Development Services

Cryptocurrency exchange development services involve building, customizing, and deploying secure platforms that allow users to trade digital assets efficiently.

These services typically include:

Core Features of Cryptocurrency Exchange Development

1. Scalable Platform Architecture

A well-designed exchange must handle high transaction volumes while maintaining performance, uptime, and data integrity. Scalability is critical for future growth.

2. User Interface (UI) & User Experience (UX)

An intuitive, trader-friendly interface improves adoption, reduces friction, and enhances retention especially for first-time users.

3. High-Performance Trading Engine

The trading engine is the heart of the exchange. It must support:

Fast order matching

Multiple order types

Real-time price updates

High concurrency

Security & Compliance: Non-Negotiables in Crypto Exchange Development

1. Advanced Security Measures

A reliable exchange integrates:

Multi-factor authentication (MFA)

End-to-end encryption

Cold and hot wallet architecture

DDoS protection and monitoring

2. Regulatory Compliance

Adherence to global standards such as:

AML (Anti-Money Laundering)

KYC (Know Your Customer)

is essential for legal operation and long-term trust.

🔔 Thinking of Launching a Crypto Exchange? Pause Here

Before investing heavily, a short technical review can save months of rework and costly mistakes.

👉 DM us directly or book a free consultation with ITIO Innovex 🌐 https://itio.in/ 📩 Message us on LinkedIn or request a callback

Let’s build a secure, scalable, and future-ready crypto trading platform together.

Conclusion

Choosing the best cryptocurrency exchange development company is a strategic decision that directly impacts security, scalability, and long-term success.

By evaluating experience, customization capabilities, compliance readiness, and technical support, businesses can avoid costly missteps. ITIO Innovex delivers all of this making it a reliable partner for cryptocurrency exchange development in today’s fast-evolving digital asset landscape.

In an era where digital payments dominate everyday transactions — from online shopping and mobile wallets to contactless in-store purchases — the security of cardholder data has never been more critical. The Payment Card Industry Data Security Standard (PCI DSS) stands as the global benchmark for protecting sensitive payment information. Developed by the PCI Security Standards Council (PCI SSC), it applies to any organization that processes, stores, or transmits credit or debit card data.

Generative AI

1. Exploding Cyber Threats and Data Breaches

Cyberattacks targeting payment systems have surged. Ransomware, phishing, supply-chain exploits, and advanced persistent threats (APTs) are common. Non-compliant businesses face higher breach risks — studies show compliant organizations experience up to 50% fewer incidents. A single breach can expose thousands of card records, leading to massive fraud and identity theft. PCI DSS enforces controls like encryption, access restrictions, and vulnerability management to minimize these risks.

2. Building and Maintaining Customer Trust

Consumers now prioritize security when choosing where to shop. A visible commitment to PCI DSS signals reliability — think “Your card details are safe with us.” In contrast, a breach erodes trust overnight, resulting in lost customers, negative reviews, and long-term reputational damage. Compliant businesses often see higher conversion rates and loyalty because customers feel protected.

3. Avoiding Severe Financial and Legal Penalties

Non-compliance carries heavy costs:

Fines from card brands (up to $100,000+ per month in severe cases)

Increased transaction fees

Liability for fraud losses and breach-related expenses (legal fees, notifications, credit monitoring)

Potential loss of payment processing privileges

With stricter enforcement under v4.0.1 — including mandatory MFA for admin access, enhanced password policies, anti-phishing measures, and continuous monitoring — regulators and acquirers are less tolerant of lapses.

4. Enabling Secure Digital Innovation

Modern businesses rely on cloud services, APIs, e-commerce platforms, and third-party processors. PCI DSS v4.0.1 introduces flexibility (e.g., customized approaches and targeted risk analysis) while raising the bar on emerging risks like payment page skimming and insecure authentication. Compliance helps organizations innovate safely — adopting new tech without exposing card data.

5. A Foundation for Broader Cybersecurity Maturity

PCI DSS isn’t just about cards — its 12 core requirements (build and maintain secure networks, protect cardholder data, maintain vulnerability management, etc.) strengthen overall security posture. Many organizations use it as a baseline for GDPR, HIPAA, or ISO 27001 alignment.

Bottom Line in 2026

In a world of nonstop digital transactions and sophisticated cybercriminals, PCI DSS compliance protects customers, safeguards revenue, and demonstrates responsibility. It’s no longer a “checkbox” — it’s a strategic imperative for any business handling payments.

If your organization processes card data, assess your current status against v4.0.1 requirements today. Non-compliance risks far outweigh the effort of achieving it.

What challenges have you faced with PCI DSS? Share in the comments — I’d love to discuss real-world tips!

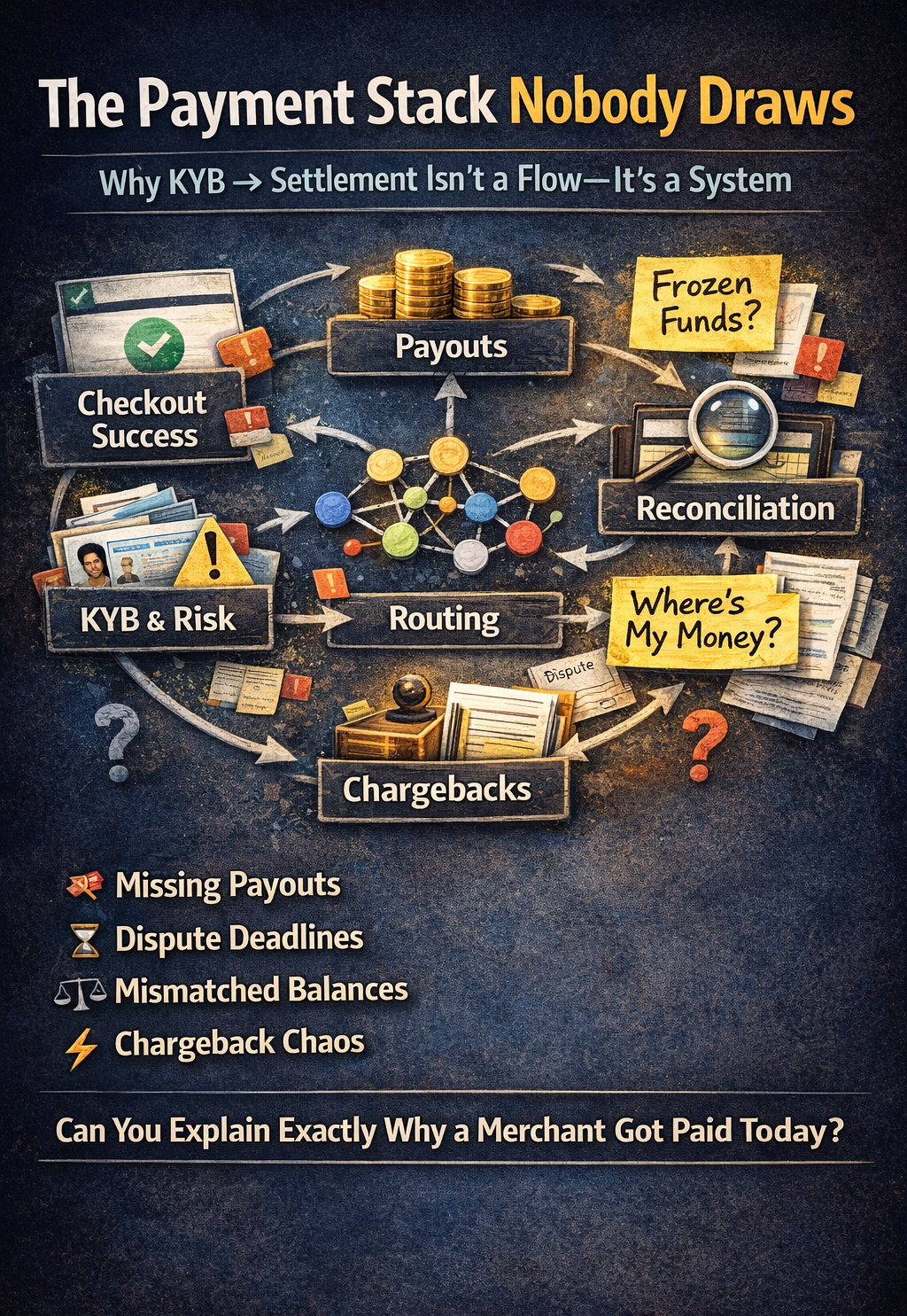

I work in payment infrastructure, and I keep seeing the same pattern across startups, marketplaces, and PSP-style builds.

Teams spend weeks perfecting checkout.

Then they get blindsided by payouts, disputes, mismatched balances, and “why didn’t I get paid?” emails.

Not because the payment gateway failed. But because KYB → risk → routing → settlement → reconciliation was treated like a straight line.

It isn’t.

It’s a system one that has to stay consistent when real money, real merchants, refunds, chargebacks, delayed webhooks, and regulatory scrutiny enter the picture.

If you’re building any of the following, this applies directly to you:

A marketplace (split payouts, vendor settlements)

A SaaS product (subscriptions, prorations, refunds)

Over the past three weeks, I’ve sent 50+ emails to Nigerian businesses — fashion designers in Lagos, freelance developers, gadget retailers, drone wholesalers, and crowdfunding platforms.

The feedback has been surprisingly consistent.

These aren’t isolated complaints. They’re systemic infrastructure gaps.

The pattern is clear:

Businesses are losing 10–15% to international payment fees

Freelancers are watching Naira devaluation eat their savings in real-time

E-commerce businesses are dealing with failed cross-border transactions

Operations teams face manual reconciliation nightmares

There’s constant fear of frozen accounts when accepting international payments

Traditional payment rails weren’t built for this moment. Banks can’t solve it. Payment processors won’t solve it. Someone has to create the alternative.

BillingBase is non-custodial crypto billing infrastructure for global businesses.

Let me break down what that actually means:

Non-custodial means payments go directly to YOUR wallet. We never hold your funds. We don’t control your money. We don’t have the ability to freeze your account. You maintain complete custody while we handle the infrastructure.

Crypto billing infrastructure means we provide the payment primitives you’re already familiar with — checkout links, subscriptions, refunds, webhooks, invoicing — except they work with stablecoins instead of traditional payment rails.

For Nigerian businesses, this means we understand the specific problems you face: Naira devaluation, international payment friction, high platform fees, and the need for dollar-denominated earnings that hold their value.

Here’s what you can do with BillingBase:

Accept stablecoin payments: USDT, USDC, DAI, and CNGN (Naira-pegged)

Use familiar tools: Payment links, recurring subscriptions, one-time payments, refunds, webhooks, and a dashboard to track everything

Get built-in protection: Chainalysis wallet screening, transaction-level risk checks, KYB verification, and audit trails for compliance

Why We’re Starting with a Beta

We don’t have all the answers yet.

What we know:

Nigerian businesses need better cross-border payments. Naira devaluation makes dollar earnings critical. Platform fees (Upwork’s 15%, Stripe’s 3.9%, PayPal’s conversion markups) are too high. International customers increasingly pay with stablecoins. Operations teams need reconciliation tools that traditional banks don’t provide.

What we need to validate:

Core features: Which payment primitives matter most? Do fashion designers prioritize deposit handling or subscription billing? Do freelancers want simple payment links or full API integration? Where’s the acceptable onboarding friction threshold?

Compliance: What documentation feels reasonable versus invasive? KYB is necessary, but where’s the line between thorough and annoying?

Infrastructure: Which blockchains — Base (lowest fees), Polygon (widely supported), Arbitrum (fast settlement)? Do businesses care, or just want “cheapest and fastest”? USDC (dollar-pegged) or CNGN (Naira-pegged)?

Integrations: QuickBooks? Xero? Google Sheets? Slack notifications when payments arrive?

Questions only real usage can answer:

How do designers handle deposits versus final payments?

Do freelancers prefer shareable links or automated invoicing? What reporting do finance teams need?

How often do merchants convert stablecoins to Naira?

What’s the right balance between automated risk controls and merchant control?

We can’t answer these in a vacuum. We need real businesses using BillingBase with real customers.

We’re looking for specific businesses where stablecoin payments solve real problems.

1. SME Businesses with Global Clients Fashion designers, bridal boutiques, custom clothiers, bespoke service providers with international clients who ship worldwide or provide remote services.

Your pain: 3–7 day payment delays, high cross-border fees, difficult deposit handling, currency conversion losses.

What you get: Instant stablecoin settlement, payment links for deposits/finals, dollar-denominated earnings, free integrated website during beta.

2. Freelancers & Service Providers Developers, designers, consultants, educators working directly with clients or through Upwork/Fiverr/Toptal.

Your pain: 10–15% platform fees, poor PayPal conversion rates, dollar invoices settled in devalued Naira, no professional low-cost direct payment option.

What you get:0.5% transaction fees, payment link dashboard, dollar earnings protected from devaluation, automatic receipts and audit trails.

Your pain: Slow, expensive wire transfers, high cross-border fees, poor reporting, and difficulty tracking recurring contributions.

What you get: Donation links (one-time/recurring), lower fees, instant international contributions via stablecoins, and clean reporting for finance teams and donors.

What we’re NOT looking for (yet):

High-volume enterprises: If you’re processing 10,000 transactions per day, we’re not ready for you. We’re optimizing for businesses with 10–500 transactions per month during beta.

Businesses requiring instant Naira conversion: We don’t provide off-ramp services yet. You’ll need your own method to convert stablecoins to Naira if needed (P2P platforms like Binance, Bybit, or local exchanges work well).

Companies needing white-label solutions: If you want to rebrand BillingBase as your own product, that’s not our focus right now.

Anyone expecting zero bugs: This is a beta. There will be rough edges. If you need production-perfect software on day one, wait for our public launch later this year.

What Beta Participants Get

1. Free Integration & Setup

No setup fees: Most payment platforms charge $500-$2,000 for integration. We don’t.

No monthly subscription during beta: Use BillingBase for free while we’re testing.

Transaction fees waived for first 90 days (or first 100 transactions): Whichever comes first. After that, standard fees apply (0.5% or lower depending on volume).

One-on-one onboarding support: We’ll walk you through wallet setup, dashboard usage, and first transactions. No “figure it out yourself” documentation dumps.

2. Custom Solutions Based on Your Business Type

For fashion designers: We’ll build you a one-pager website with integrated payment links. Free during beta. Professional design. Consultation booking system if needed.

For e-commerce businesses: We’ll integrate BillingBase API directly with your existing website. Custom checkout flow. Webhook setup. Testing support.

For freelancers: Payment link dashboard optimized for invoicing. Easy sharing via email, WhatsApp, or social media. Automatic receipt generation.

For educators: Subscription billing for courses or memberships. Payment links for one-time consultations or content. Recurring payment automation.

3. Direct Access to the Team

Weekly feedback calls (optional): Tell us what’s working and what’s broken.

Slack/WhatsApp channel with founders: Direct line to Ngozi and the team. No support ticket black holes.

Priority bug fixes: If something breaks, we fix it fast. Beta participants get priority.

Your input shapes the product roadmap: We’re not building in isolation. If you need a feature, we’ll consider adding it based on beta feedback.

4. Early Mover Advantage

Lifetime discounted pricing after beta: When we launch publicly, you’ll pay less than new customers — forever.

Featured case studies (with permission): If you’re willing, we’ll showcase how you’re using BillingBase. Good for your brand, good for ours.

First access to new features: New integrations, reporting tools, or blockchain support? Beta participants see it first.

Referral program with revenue share: Refer other businesses to BillingBase and earn a percentage of their transaction fees.

What We’re Asking From You

This isn’t passive testing. If you just want to “try it out and see,” that’s not what we need.

Time Commitment:

30–60 minutes: Initial setup (wallet, KYB verification, dashboard walkthrough, first test transaction)

15–30 minutes periodically: Feedback calls (every 2 weeks to monthly, depending on usage)

24–48 hour response time: When we ask “Can you try this again and tell us what happened?”

5–10 minutes monthly: Survey on feature usage and pain points

Honesty Requirement:

We need brutal feedback, not polite validation.

Tell us what’s confusing, broken, or doesn’t fit your workflow. Share what your customers say — positive and negative. If onboarding felt complicated, the dashboard doesn’t make sense, or a feature exists but you don’t understand why you’d use it, tell us. Screenshots help. Screen recordings are better.

We’re not looking for cheerleaders. We’re looking for honest partners who’ll tell us when we’re wrong.

Real Usage:

Use this with real customers. Test transactions catch bugs, but real revenue matters more. We can’t improve what we don’t see in production.

Send a payment link to a real client. Use BillingBase for a real deposit. Integrate it and see if customers choose the crypto option. We’re not asking you to bet your entire business on this, but we need real scenarios to see what happens when money is on the line.

Patience:

There will be bugs — we’ll fix them fast. Some features won’t exist yet — we’re prioritizing based on feedback. Documentation might be incomplete — we’re improving it weekly.

Beta means “we’re still learning.” If you need production-perfect software on day one, wait for our public launch.