What I’d Teach a New 1-Minute Trader About Indicators

If a new trader came to me today and said, “I want to trade the 1-minute chart — what indicators should I use?” I wouldn’t open a chart. I…

If a new trader came to me today and said, “I want to trade the 1-minute chart — what indicators should I use?” I wouldn’t open a chart. I…

Michael Saylor says Strategy’s evolving capital-markets machine is starting to resemble a “central bank of Bitcoin,” positioning the company as a conduit between traditional money markets and the Bitcoin network. In an interview with Gatecast, the Strategy executive chairman argued the firm’s shift toward perpetual preferred equity and “digital credit” instruments is designed to fund continuous bitcoin accumulation while stripping out refinancing risk.

Saylor traced the company’s pivot to the COVID-era shock of 2020, when “the physical economy of the world came to a grinding halt and the financial system was turned upside down.” Facing what he framed as an existential decision, he said Strategy discovered Bitcoin during “the war on COVID and the war on currency,” and used it to “escape a pretty miserable existence and turned into something digital and modern and much better.”

That transformation now sits on a scale Saylor claims is often misunderstood. Addressing criticism that Strategy is simply levering up to buy more Bitcoin, he said the firm has raised roughly $44 billion over the past year and a half and characterized “most of that” as equity rather than debt. “There isn’t really leverage,” Saylor said. “Equity is capital that you have forever. We’re funneling that capital into the crypto economy. We’re buying Bitcoin.” He added that Strategy has acquired “about $48 billion worth of Bitcoin” across “like 88 different transactions,” purchasing “as soon as we raise the capital.”

When asked whether Strategy is still just a buyer or something closer to a “shadow central bank of Bitcoin” given its holdings, Saylor leaned into the analogy. “Bitcoin is digital capital. It is the world reserve capital network. It’s replaced gold as the global non-sovereign store of value for the human race,” he said. Then came the framing: “Banks normally buy credit. We actually sell credit. So what we’re doing is the reverse of commercial banking, retail banking. It is sort of like central banking. We are sort of like the central bank of Bitcoin.”

Saylor’s “central bank” claim hinges on a product stack meant to translate Bitcoin’s balance-sheet asset into yield-bearing instruments for investors who won’t hold BTC directly. He described STRC as “a currency that’s pegged to the dollar” and “backed […] with Bitcoin,” with proceeds recycled into BTC purchases. In his telling, that mechanism links “the Bitcoin economy” to “the traditional finance economy and to the money markets of the world.”

Michael Saylor: “We are sort of like the central bank of Bitcoin.” pic.twitter.com/IyZ9EHLAQn

— TFTC (@TFTC21) January 22, 2026

The more material shift, he argued, is Strategy’s progression away from maturity-driven debt toward perpetual structures. Saylor laid out a four-stage evolution: initial use of credit and leverage, a senior note secured by BTC collateral that the company later refinanced and vowed not to repeat, then non-recourse convertible bonds, an approach he said became constrained by market size and retail inaccessibility and finally “digital credit,” which he described as “an equity […]a perpetual preferred equity.”

In one of his clearest statements of intent, Saylor said Strategy’s priority is to prevent principal from ever coming due. “We don’t want to have leverage. We want to have amplification via equity. We never want the principal to come due. We’d rather pay a higher dividend forever,” he said. “I’d rather pay 10% forever than pay 5% for 5 years.” Strategy, he added, has “announced a $1.44 billion cash reserve for the dividends,” giving it “the option to not raise any capital in the capital markets for up to two years,” and in his view “effectively stripped the credit risk off of the business.”

Saylor also pitched liquidity as a differentiator. He said Strategy has raised $7 billion over the last nine months via these instruments and described an emerging market of about $8 billion outstanding. Where preferred stocks typically trade thinly, he argued Strategy’s “digital credit instruments were trading 30 million a day,” with “Stretch […] more than a hundred million a day,” which he framed as a step-change in market access.

The firm’s investor pitch, as Saylor described it, splits the world into capital and credit buyers. “Bitcoin is digital capital. The world will be built on digital capital. But the world will run on digital credit,” he said, arguing that products like Stretch can offer a money-market-like alternative “powered by digital capital” while sidestepping Bitcoin’s volatility.

At press time, BTC traded at $89,250.

OPINION — The global terrorism landscape in 2026 — the 25th anniversary year of the 9/11 terrorism attacks — is more uncertain, hybridized, and combustible than at any point since 9/11. Framing a sound U.S. counterterrorism strategy — especially in the second year of a Trump administration — will require more than isolated strikes against ISIS in Nigeria, punitive counterterrorism operations in Syria, or a tougher rhetorical posture.

A Trump administration counterterrorism strategy will require legitimacy: the domestic, international, and legal credibility that leverages a wide-range of counterterrorism tools, while engendering international counterterrorism cooperation. Without legitimacy, even tactically successful counterterrorism operations risk becoming illusory, politicized, and ultimately self-defeating.

The terrorist threat landscape

Extremist violence no longer conforms to clean ideological lines. Terrorist objectives and drivers are muddled in ways that are hard to understand — but evolving. There’s little ideological purity with those radicalizing in today’s extremist milieu.

At the same time, state-directed intelligence officers increasingly behave like terrorists. Russian intelligence-linked sabotage plots blur the line between terrorism and hybrid warfare. Islamic Revolutionary Guard Corps officers provide hands-on training to Lebanese Hizballah commanders. Addressing these kinds of risks requires legitimacy, too, especially among allies whose intelligence cooperation, legal authorities, and public support are indispensable.

Nowhere is this threat picture more tenuous than in the Middle East. Hamas’s October 7, 2023, attacks triggered a profound rebalancing of power in the region. Yet, Syria remains unfinished business. Power vacuums there invite foreign jihadists, threaten Israel's border communities, and create future opportunities for Iranian influence to rebound.

A modest but persistent U.S. presence in Syria with a friendly Ahmed al-Sharaa-led government remains a strategic hedge against an Islamic State resurgence, and is a strong signal of U.S. commitment that helps sustain partner confidence. The U.S. counterterrorism presence and alignment with al-Sharaa is not without its risks, though: in December, three Americans were killed by a lone ISIS gunman in central Syria. The country is, and will continue to be, plagued by sectarianism and terrorism, which means that restoring control over a deeply fractured Syria remains fraught.

Taken together, the current transnational terrorism threat landscape is volatile and difficult to predict, a challenge compounded by resource constraints. In such an environment, legitimacy becomes a force multiplier. A belief that America is a ‘force for good’, credible messaging, and confidence that U.S. government action is perceived as just, can go a long way.

This is not an abstract concern. Terrorism today thrives in contested information environments, polarized societies, and fragile states. In short, transnational jihadist networks now coexist with domestic violent extremists, and online radicalization ecosystems that blur the line between terrorism, insurgency, and hybrid warfare. Terrorist propaganda continues to resonate with individuals in the West, especially younger generations who radicalize online. In this environment, legitimacy is no longer a secondary benefit of sound strategy—it is a core guiding principle.

The Trump administration's counterterrorism approach

We are looking for more clarity on the trajectory of Trump 2.0 counterterrorism efforts. It’s still, premature to consider a strategy that has yet to be formally articulated, as many in the counterterrorism community eagerly await its release. History offers a useful reminder. The first Trump administration did not publish its National Strategy for Counterterrorism until its second year. When it appeared in 2018, critics and supporters alike acknowledged that it reflected professional judgment rather than ideological excess. That document recognized terrorism’s evolution and called for strengthening counterterrorism partnerships within the U.S. government, but abroad as well, with a range of longstanding allies.

What gave that strategy durability was its legitimacy. Authorities were grounded in law, threat assessments were evidence-based, policies were stress-tested for faulty assumptions, and foreign partnerships were treated as strategic assets rather than transactional relationships.

When the Biden administration publicly released a set of redacted rules secretly issued by President Trump in 2017 for counterterrorism operations — such as “direct action” strikes and special operations raids outside conventional war zones — those guidelines explicitly acknowledged the power of legitimacy. Counterterrorism succeeds when allies trust the U.S., and the American public believes force is used proportionately and lawfully.

That legacy of trust matters now more than ever, given signals that a second Trump administration could overcorrect on its counterterrorism priorities by redirecting and focusing resources on far-left extremist groups such as the Turtle Island Liberation Front (TILF) or Antifa, while downplaying far-right extremism—or being distracted from the more dangerous terrorism threats from ISIS and other violent jihadists. As the world recently witnessed during the holidays, from Bondi Beach to Syria, ISIS remains a threat. Far-Left terrorism in the U.S. is on the rise, but far-right terrorism accounts for greater lethality than did the left. And still, after 25 years, it’s ISIS and al-Qa’ida that remain the most persistent and enduring transnational terrorism threat against U.S interests.

The Trump National Security Strategy

It’s concerning that the recently published National Security Strategy (NSS) only tepidly addresses transnational terrorism, but notably links terrorism with cross-border threats and hemispheric cooperation against things like “narco-terrorists,” blurring the traditional separation between transnational organized crime and terrorism.

Still, the Trump administration’s emphasis on drug cartels is justifiable, if it does not detract from broader counterterrorism objectives, such as the ISIS or hybridizing terrorist threats that continue to emerge. Commentators claim, however, that the Trump administration is already losing sight of the ISIS and al-Qa’ida threats, though settling that debate here is quixotic at best — only time will tell.

Besides jihadi threats, the U.S. does not need the unintended consequences and risks of triggering a cycle of cartel retaliation – or provoking greater far-left violence – down-the-line in the U.S. homeland.

Contrastingly, the 2017 National Security Strategy saw radical Islamist terrorism as one of the priority transnational threats that could undermine U.S. security and stability. The strategy highlighted groups such as ISIS and al-Qa’ida as continuing dangers, stressing that terrorists had taken control of parts of the Middle East and remained a threat globally.

The Cipher Brief brings expert-level context to national and global security stories. It’s never been more important to understand what’s happening in the world. Upgrade your access to exclusive content by becoming a subscriber.

Addressing transnational terrorism during the first Trump administration required discipline and steadiness amid predictable frictions at the National Security Council (NSC) among policymakers who wanted a more rapid shift toward other priorities, such as great power competition. Still, terrorist labeling and designations, strategic messaging, and resource allocation for counterterrorism were grounded in evidence rather than politics.

So, overhyping some threats while minimizing others undermines legitimacy, invites backlash, and weakens the very moral authority needed to operationalize a cogent, thoughtful national security strategy. It also erodes trust between the government and the public and leads citizens to second-guess whether they are being told the truth or being led astray. The 2017 NSS carried weight precisely because it was grounded in intelligence, not politics. Moreover, the NSS helped frame the counterterrorism strategy that followed and proved highly effective in keeping Americans safe.

Drawing lessons from the 2018 National Strategy for Counterterrorism

The 2018 National Strategy for Counterterrorism (NSCT) remains a useful foundation for the second Trump administration—not because the world is unchanged, but because it embraced balance. The strategy emphasized foreign partnerships, non-military tools, and targeted direct action when necessary. It recognized a central legitimacy principle: the United States cannot and should not fight every terrorist everywhere with American troops when capable counterterrorism partners can do so in their own backyards, with local consent, and a more granular understanding of the grievances that motivate these terrorist groups and their supporters.

And still, U.S. counterterrorism pressure through direct action remains a necessary tool to disrupt terrorism planning. It seems that the second Trump Administration is following the playbook of the first Trump administration in terms of aggressive counterterrorism kinetic strikes in places like Somalia, Yemen, and Iraq.

President Trump rescinded Biden-era limits on counterterrorism drone strikes, allowing the kind of flexible operational framework used for counterterrorism throughout the President’s first term. Thus far, in the aggressive counter-narcotic campaign in international waters off Venezuela, the standoff U.S. strikes resemble counterterrorism operations in Yemen and Somalia during the first Trump administration. Operationally, direct action remains an indispensable counterterrorism tool for disrupting terror groups overseas, and more U.S. direct action will likely be necessary in West Africa and the Sahel to keep jihadist groups operating there off balance, forcing them to devote more time and resources to operational security.

But pressure without legitimacy is counterproductive. What works against jihadist networks does not necessarily translate cleanly to drug cartels or transnational criminal gangs. So, policymakers must be circumspect that expanding the scope of counterterrorism authorities and terrorist designations to canvas drug cartels, risks the unintended consequences of triggering destabilizing cycles of violence in the future, and straining more traditional counterterrorism resources.

Coming full circle, in light of the U.S. capture of Nicolás Maduro for narcoterrorism-related offenses, the idea of legitimacy will be fiercely debated in the days and weeks ahead. If the Trump National Security Strategy is the roadmap for focusing on narcoterrorism in the Western Hemisphere, then the need for publishing a clarifying and rational U.S. counterterrorism strategy for the rest of the world takes on even greater sense of urgency.

Pushing a boulder uphill

Drawing on past counterterrorism lessons to find a comprehensive strategy—from the Bush administration’s wartime footing, through 8 years of Obama counterterrorism work, to President Trump’s "war on terror" — is a Sisyphean task. But, in the wake of over two decades of relentless overseas counterterrorism work, a few ideas have come into sharper focus:

After more than two decades of counterterrorism, loosening the Gordian knot of modern terrorism requires balance, far greater clarity, and consistent, predictable national leadership.

Above all, counterterrorism strategy requires legitimacy. Without it, counterterrorism becomes reactive and politicized. With it, a Trump 2.0 counterterrorism strategy can still be firm, flexible, and credible in a far more dangerous world.

The Cipher Brief is committed to publishing a range of perspectives on national security issues submitted by deeply experienced national security professionals. Opinions expressed are those of the author and do not represent the views or opinions of The Cipher Brief.

Have a perspective to share based on your experience in the national security field? Send it to Editor@thecipherbrief.com for publication consideration.

Read more expert-driven national security insights, perspective and analysis in The Cipher Brief, because national security is everyone’s business.

Crypto pundit Crypto Chase has explained how Strategy’s Bitcoin holdings is a net negative for BTC’s adoption, especially among large investors. The pundit also ruled out the possibility of capitulation on Michael Saylor’s part, even if the flagship crypto drops below their entry point.

In an X post, Crypto Chase opined that Strategy’s BTC holdings do more to deter institutions and high-net-worth individuals than to attract them. The pundit added that there really isn’t any full-scale capitulation below Saylor’s average entry price of $76,000, as he believes that Saylor and Strategy will hold until zero, except if the board forces them to do otherwise.

This statement followed Strategy’s latest $2.13 billion Bitcoin purchase, which saw the company’s holdings cross the 700,000 BTC milestone. The company now holds 709,715 BTC, which it acquired for $53.92 billion at an average price of $75,979. Meanwhile, Crypto Chase also stated that if the company were to offload these coins, the Bitcoin price would go back to $3,000 or lower.

The pundit warned that there are not even close to enough bids to handle such selling pressure. As such, he believes that Strategy’s Bitcoin holdings would have to be sold over the counter to the U.S. government or Trump to avoid a total collapse of the flagship crypto. However, Saylor has so far asserted that they have no intention of ever selling their BTC holdings.

Crypto Chase also mentioned that fear among uneducated market participants could provide a good entry if the narrative is that Saylor and Strategy would be liquidated if BTC drops below their average entry price. The pundit reiterated that it is game over if that ever happened, though. He is also not confident Bitcoin will rise to new highs anytime soon, noting there is significant overhead and Total Cost of Ownership, with entry points above $100,000.

It is worth noting that Crypto Chase’s statement about Saylor’s Strategy and Bitcoin’s holdings was in response to crypto pundit Ansem’s point of view. In an X post, Ansem said he believes Bitcoin will find its place alongside gold and silver in portfolios and benefit from large, high-net-worth individuals and institutions adding small positions. He remarked that BTC, as a digital analog, is easier to transport across global borders and easier to transact with.

Ansem also noted that Saylor and Strategy’s cost average is currently around $75,000 and that he believes that a drop below that level would be a full-scale capitulation into a generational buying opportunity. From a technical standpoint, the pundit does not think Bitcoin will trade below last cycle’s price peak of $69,000 in 2021.

Automation doesn’t always look dramatic at first. Spot five subtle signs your work is shifting, from oversight to self-serve, and how it adds up over time.

The post 5 Subtle Signs Your Job Is Slowly Being Automated appeared first on TechRepublic.

Automation doesn’t always look dramatic at first. Spot five subtle signs your work is shifting, from oversight to self-serve, and how it adds up over time.

The post 5 Subtle Signs Your Job Is Slowly Being Automated appeared first on TechRepublic.

To all those who are fighting the good fight in the world of cyber, keep collaborating to ensure our world never succumbs to the chaos of the Upside Down.

The post The Upside Down is Real: What Stranger Things Teaches Us About Modern Cybersecurity appeared first on SecurityWeek.

Trump canceled EU tariffs, stocks soared, but crypto struggles. I analyze what’s next for Bitcoin, Ethereum, and altcoins in 2025.

I believe we are entering a pivotal era of convergence in global financial infrastructure. For decades, the correspondent banking system has served as the bedrock of international commerce, providing the necessary trust and regulatory oversight to move trillions of dollars across borders. However, even the most robust systems require modernization to meet the 24/7 demands of today’s digital economy. As I evaluate the landscape in 2026, it is clear that the industry is not moving toward the replacement of traditional banks, but rather a systems phase where legacy strengths are being rewired with digital native speed.

The traditional model of correspondent banking relies on a series of bilateral relationships. A single international wire transfer often passes through multiple intermediary banks. While this structure ensures rigorous compliance and risk management, it inevitably introduces layers of manual reconciliation and settlement windows that are limited by banking hours. This T+3 or T+5 cycle is increasingly being viewed by treasurers as an area where traditional finance and blockchain technology can form a powerful synergy to eliminate capital in transit.

The gap between legacy settlement times and modern expectations is no longer just a technical hurdle: it is a measurable economic opportunity. According to the Bank for International Settlements (BIS), a next generation financial system based on tokenized ledgers can dramatically improve the integrity and accessibility of money. To understand the scale of this opportunity, one must look at the B2B cross border market, which is projected to grow significantly as digital trade accelerates.

I use the term dead liquidity to describe the capital currently held in the suspense accounts of correspondent networks. According to the Financial Stability Board (FSB), progress on global payment speeds remains a priority for the G20. While the target is to have 75% of cross border payments credited within one hour by 2027, the J.P. Morgan 2025 progress review shows that only 33.5% of payments currently reach that target.

In my view, the rise of stablecoins is the market’s response to this need for liquidity mobility. Recent industry reports indicate that B2B stablecoin payment volumes have reached an annualized run rate exceeding 120 billion dollars. This is not a flight away from banking, but a shift toward more efficient rails that banks themselves are beginning to adopt to meet G20 objectives.

One of the most significant advantages of this convergence is what I call Finality Certainty. In traditional correspondent banking, the lack of a unified ledger can sometimes lead to opacity during the settlement process. Stablecoins, particularly those governed by the US GENIUS Act framework, provide on chain visibility and near instant settlement finality.

Because these assets are now recognized by federal legislation as regulated payment instruments, they are increasingly being treated as a true cash equivalent. This allows banks to provide their clients with the best of both worlds: the safety and regulatory protection of a traditional financial institution, combined with the atomic settlement speed of a digital rail. For a corporate treasurer, the ability to see a transaction settle in real time on a public or private ledger is a significant upgrade in risk management and treasury forecasting.

The financial burden of legacy infrastructure has historically been a challenge for mid market companies. A typical international transfer can incur various intermediary fees and currency bid ask spreads. For a business moving 10 million dollars monthly across borders, these overheads can be substantial when calculated across an entire fiscal year.

In 2026, I believe we are seeing an evolution of the middleman. Rather than multiple banks passing the baton as in a relay race, we are moving toward a model where banks act as the regulated gateways to a shared digital ledger. Initiatives like Project Agorá, led by the BIS and seven central banks, are exploring how to integrate tokenized commercial bank deposits with wholesale central bank money. This allows the bank to maintain the customer relationship and compliance oversight while using a more efficient settlement layer to move value instantly.

As I evaluate the competitive landscape for 2026, the benefits of this hybrid approach become undeniable:

I do not believe we will see the total replacement of traditional banks by 2030. Instead, I expect the standard to be programmable treasury, where businesses use traditional rails for local domestic needs but switch to regulated stablecoin rails for international settlement.

This requires a sophisticated bridge: licensed onramp and offramp infrastructure that can handle high volume conversions without compromising compliance. The settlement showdown is not a battle between old and new. It is a collaborative effort to build a more inclusive and efficient global economy. By combining the trust of traditional finance with the efficiency of modern rails, we are finally solving the oldest friction in international trade.

The Settlement Showdown: Why Correspondent Banking and Stablecoins are Converging for Modern Trade was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.

Strategy continues to dominate as the largest Bitcoin treasury company. This time, the company has expanded its holdings, crossing 700,0000 BTC in the process, and currently holds over 3% of the total Bitcoin supply.

Michael Saylor’s Strategy now holds approximately 3.4% of the total Bitcoin supply as the company increased its holdings to over 700,000. In a press release, the company revealed that it acquired 22,305 BTC for $2.13 billion at an average price of $95,284 per Bitcoin last week. It now holds 709,715 BTC, which it acquired for $53.92 billion at an average price of $75,979.

This purchase was Strategy’s largest weekly announcement since November 2024 and its fifth-largest announcement ever. It also came just a week after the company announced it had acquired 13,627 BTC for $1.25 billion. Meanwhile, this latest purchase has come amid a decline in BTC’s price.

Bitcoin dropped below $90,000 yesterday for the first time since the start of the year, dragging the Strategy stock with it. MSTR dropped as much as 8% yesterday, falling to around $160. The stock is still up over 3% year-to-date (YTD). However, it is worth noting that Saylor and his company continue to dilute MSTR shares to buy more Bitcoin. The company sold 10.4 million MSTR shares last week to fund most of this latest purchase.

Market analyst Rob noted that Strategy no longer highlights BTC yield as a flagship metric. He further stated that even after buying over 35,000 BTC in the first few weeks of this year, the BTC yield achieved is 0.4%, which amounts to an annualized rate of about 6% to 10%. The analyst also remarked that the law of diminishing Bitcoin yield means the ability to deliver a yield decreases as the BTC stack grows.

With Strategy now holding over 700,000 BTC, Rob explained that it is harder to generate a return. According to him, this means that going forward, the play is more about squeezing the Bitcoin price itself higher rather than increasing the BTC per share. He added that this also explains why MSTR’s mNAV has collapsed to just over 1x.

Crypto commentator Ran Neuner warned that a company like Strategy buying and holding such a large concentration of a reserve asset is not healthy. He added that right now, Saylor and his company are the only ones really buying Bitcoin. Meanwhile, market expert Bit Paine said it is a market failure that Saylor is allowed to buy this much BTC at prices below $100,000.

At the time of writing, the BTC price is trading at around $90,000, down in the last 24 hours, according to data from CoinMarketCap.

Most prop firms believe the hardest part is the evaluation. It isn’t.

The evaluation phase is structured, constrained, and explicit. Traders are told exactly what not to do. Risk is visible. Failure is immediate. Behavior is shaped by clear boundaries.

Funding changes everything.

Once capital scales, rules thin out. The leash comes off, but the thinking framework doesn’t evolve with it.

And that’s where firms quietly lose their best traders.

During evaluations, traders are not learning how to trade profitably.

They are learning how to avoid disqualification.

That distinction matters.

Constraint-driven behavior works when:

Funding removes the binary outcome.

Suddenly, the trader isn’t asking:

“How do I pass?”

They’re asking:

“How do I not give this back?”

That shift is subtle… and lethal if unaddressed.

Most funded traders don’t blow accounts. They decay.

The equity curve doesn’t collapse — it bleeds.

From the firm’s side, this looks like:

From the trader’s side, it feels like:

Silence is often interpreted as stability. This is far from the truth.

Many traders internalize “control risk” as:

“Don’t lose.”

Many firms operationalize risk control as:

“Don’t break rules.”

Neither addresses decision-making quality under scaled capital.

Losses are not the enemy; unexamined behavior is.

A trader can follow every rule and still slowly exit profitability if they’re trading defensively against imagined threats instead of structured risk.

This is especially common among traders who passed evaluations cleanly — because they were good at constraint, not ambiguity.

👉 “Why Most Traders Fail After Passing Prop Firm Evaluations”

The firms that survive long-term don’t simply loosen rules after funding.

They replace constraint with reasoning.

They help traders answer questions like:

This isn’t motivation. It isn’t community hype. And it isn’t more dashboards. It’s thinking infrastructure.

Most firms stop teaching once the account is live.

That’s when teaching should actually begin.

👉 Execution Under Pressure: Why Most Traders Fail When It Actually Matters

When this post-funding gap goes unaddressed, firms experience:

Marketing doesn’t fix this. More flexible rules don’t fix this. Lower fees don’t fix this. The problem isn’t acquisition.

It’s retention through clarity.

If your funded traders are quiet, compliant, and slowly shrinking in activity, that isn’t stability.

It’s uncertainty without guidance.

The firms that win the next phase of this industry won’t be the loudest. They’ll be the ones that understand how traders think once the leash comes off.

If this perspective resonates, it’s likely because you’ve already noticed fragments of it inside your own trader base.

I spend most of my time studying post-evaluation behavior. Not to coach traders emotionally, but to understand how decision-making changes once capital scales.

If exchanging notes on this gap would be useful, a quiet conversation is usually enough to tell whether there’s alignment.

Why Most Prop Firms Lose Traders After Funding (And Mistake Silence for Stability) was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.

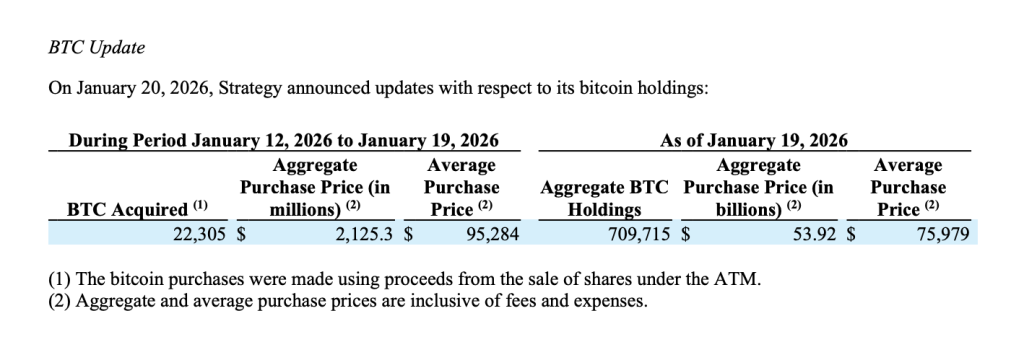

Bitcoin treasury company Strategy has unveiled a new $2.13 billion BTC acquisition, its largest spend since July 2025’s $2.46 billion purchase.

As announced by Strategy co-founder and chairman Michael Saylor in an X post, the company has completed another Bitcoin acquisition, this one involving 22,305 BTC.

According to the filing with the US Securities and Exchange Commission (SEC), the purchase occurred in the period between January 12th and 19th, and cost Strategy $95,284 per token or $2.13 billion in total. The firm sold shares of its STRK, STRC, and MSTR at-the-market (ATM) stock offerings to fund the buy.

Usually, Strategy reveals new acquisitions on Mondays, but this time the announcement has come on a Tuesday. The routine Sunday Saylor post foreshadowing the buy, however, did come on time.

This time, the Strategy chairman made the post with the caption “₿igger Orange.” Many in the community speculated that the caption was a hint at the next purchase from the company being bigger than the last, which already involved a significant sum of 13,627 BTC.

And indeed, not only has the buy been larger, it has in fact been the largest Bitcoin acquisition made by the firm since November 2024 in terms of the number of tokens involved. The larger purchase in that month expanded Strategy’s treasury by a whopping 55,500 BTC.

When considering the USD value, though, the latest acquisition falls short of a purchase from late July 2025, costing the company about $2.46 billion. BTC was trading at a higher value back then, so the larger USD sum got the company a lower amount of coins (21,021 BTC).

Following the latest purchase, Saylor’s firm has crossed the 700,000 BTC milestone, as its holdings have now risen to 709,715 BTC. Strategy spent a total of $53.92 billion on this stack and its current value stands at $63.55 billion, putting it in a profit of nearly 18%.

As Strategy continues to accumulate, it’s solidifying its already dominant position as by far the largest corporate holder of Bitcoin, as rankings from BitcoinTreasuries.net indicate.

Strategy’s closest digital asset treasury competitor isn’t a Bitcoin company, but rather an Ethereum one: Bitmine. Originally a mining-focused firm, Bitmine adopted an ETH treasury strategy in mid-2025 and has quickly established itself in the space, becoming the number one corporate holder of Ethereum and number two in overall rankings behind Strategy.

According to a Tuesday press release, Bitmine has also added to its reserves over the past week, purchasing 35,268 ETH. This has taken the company’s total holdings to 4,203,036 ETH, equivalent to nearly 3.5% of the cryptocurrency’s entire circulating supply.

Bitcoin has been showing bearish momentum recently as its price has declined to the $89,300 level.

Bitcoin Magazine

Strategy Stock ($MSTR) Slides 7% as Aggressive Bitcoin Buying Continues

Strategy (MSTR) made headlines this morning for its continued ambitious Bitcoin accumulation strategy, even as its stock struggles under mounting investor pressure.

On Tuesday, shares of the Bitcoin-focused company fell over 7% in early trading at times, despite the firm officially surpassing the 700,000-BTC milestone.

The latest acquisition, disclosed January 20, adds 22,305 Bitcoin to Strategy’s treasury at an average cost of $95,284 per coin, bringing total holdings to roughly 709,715 BTC. The purchases were funded through the company’s at-the-market (ATM) equity and preferred stock programs, which raised about $2.125 billion in net proceeds between January 12 and 19.

Sales included 2.95 million STRC variable-rate preferred shares and 10.4 million MSTR Class A common shares, with smaller amounts raised via STRK preferred stock.

While the milestone cements Strategy’s position as the world’s largest corporate holder of Bitcoin, representing over 3% of the cryptocurrency’s total circulating supply, the stock decline shows how closely Strategy still follows the price of Bitcoin.

Bitcoin plunged over 5% in just 36 hours, dipping below $90,000 as macro uncertainty and scrutiny of corporate bitcoin treasuries spooked the market. A sharp $4,000 drop Sunday night was fueled by over $500 million in liquidations in crypto derivatives.

Analysts say MSTR’s recent price weakness stems from issuing millions of new shares to buy Bitcoin, with TD Cowen recently cutting its price target to $440 due to a “weaker outlook for Bitcoin yield.”

Despite the sell-off, institutional interest in Strategy remains notable. Last week, Vanguard Group disclosed a $505 million investment in MSTR, marking its first entry into the company’s stock.

Technical analysts point to an inverted head-and-shoulders pattern forming on the daily chart, suggesting a potential bullish reversal if shares can sustain a breakout above $175. Failure to hold above $168 could, however, trigger a drop below $160.

The latest tranche of Bitcoin was acquired at an aggregate cost above Strategy’s historical average of $75,979 per BTC, illustrating the firm’s willingness to continue scaling its holdings despite elevated prices.

Saylor has repeatedly emphasized the company’s long-standing “capital markets-to-Bitcoin” approach, using equity issuance to fund crypto accumulation.

Speaking at the Bitcoin MENA conference last year, Saylor framed Bitcoin as the foundation of a new era in digital capital and credit, not just an investable asset.

Saylor said that major U.S. banks have moved from cautious observers to offering Bitcoin custody and credit solutions.

He argued that, like gold historically, Bitcoin could underpin a global digital credit system, aligning long-term growth with investor returns.

This post Strategy Stock ($MSTR) Slides 7% as Aggressive Bitcoin Buying Continues first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Bitcoin Price Slumps 6% in Two Days, Briefly Falls Below $90,000

Bitcoin price fell sharply over the past 36 hours, sliding more than 5% over that time and briefly dipping below $90,000 early Tuesday as macroeconomic uncertainty and renewed scrutiny of corporate bitcoin treasuries weighed on the market.

The world’s largest cryptocurrency was trading near $95,500 on Sunday night but fell to around $89,800 by Tuesday morning, extending losses that began with a violent sell-off late Saturday and into Sunday evening and Monday morning.

The move erased nearly $5,700 from bitcoin’s price in less than two days, according to Bitcoin Magazine Pro data.

The initial leg lower came Sunday night, when the bitcoin price plunged nearly $4,000 in a two-hour window amid heavy selling across crypto markets.

Around 6 p.m. EST, a wave of liquidation-driven selling hit derivatives markets, wiping out more than $500 million in leveraged long positions in roughly an hour, with total crypto long liquidations topping $525 million during the period.

The sell-off coincided with heightened macro uncertainty after U.S. President Donald Trump announced plans to impose sweeping new tariffs on European nations beginning February 1.

Under the proposal, a 10% tariff would apply to goods from eight countries — Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands and Finland — rising to 25% by June 1 if no agreement is reached.

Trump tied the measures to U.S. efforts to secure Greenland, further escalating transatlantic tensions.

European leaders pushed back strongly, warning the tariff threats could trigger a “dangerous downward spiral.”

All this is happening as gold surges to a new all-time high near $4,750, underscoring a flight toward traditional safe-haven assets as risk markets sold off. This flight hasn’t been reflected in the bitcoin price.

Adding to uncertainty, the U.S. Supreme Court is expected to rule on whether Trump had the authority to impose broad tariffs under emergency powers.

The case centers on the use of the International Emergency Economic Powers Act (IEEPA) to declare trade deficits a national emergency.

A ruling against the administration could force the government to refund more than $100 billion in tariffs already collected, potentially disrupting budget and defense funding assumptions.

On-chain data shows GameStop allegedly transferring a total of 2,396 BTC to Coinbase Prime in January, including 100 BTC on Jan. 17 and 2,296 BTC on Jan. 20.

The transfers represent roughly 51% of the company’s original 4,710 BTC holdings, sparking speculation that the meme-stock retailer may be preparing to sell part of its bitcoin position.

GameStop added bitcoin to its corporate treasury in mid-2025, purchasing 4,710 BTC during a brief window in May at an average price near $106,000 per coin.

While transfers to brokerage wallets are often interpreted as potential selling signals, the company has made no official announcement confirming a sale.

In contrast, Strategy (MSTR), the world’s largest publicly traded corporate bitcoin holder, continued to buy aggressively last week.

The company disclosed the purchase of 22,305 BTC for approximately $2.13 billion at an average price of $95,284 per bitcoin. As of Jan. 19, Strategy holds 709,715 BTC acquired at an average price of $75,979, representing more than 3% of bitcoin’s circulating supply.

Despite the accumulation, Strategy shares fell about 7% in early trading as the bitcoin price slid below $90,000, highlighting the growing sensitivity of bitcoin-exposed equities to short-term price moves.

The bitcoin price is trading at $90,252, down 3% over the past 24 hours on $45 billion in volume, leaving it about 3% below its seven-day high of $93,302.

The network’s market capitalization stands at roughly $1.8 trillion, with 19.98 million BTC in circulation out of a capped supply of 21 million.

This post Bitcoin Price Slumps 6% in Two Days, Briefly Falls Below $90,000 first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Bitcoin Magazine

Michael Saylor’s Strategy ($MSTR) Spends $2.13 Billion to Buy 22,305 Bitcoin

Strategy (MSTR), the world’s largest publicly traded corporate holder of bitcoin, has added another major tranche of BTC to its balance sheet, purchasing 22,305 bitcoin for approximately $2.13 billion over the past week.

The acquisition, disclosed today, was made at an average price of roughly $95,284 per bitcoin, roughly 4% more than current prices. As of Jan. 19, 2026, Strategy now holds a total of 709,715 BTC, acquired for approximately $53.92 billion at an average price of $75,979 per coin.

The latest purchase marks Strategy’s largest weekly bitcoin acquisition since November 2024 and its fifth-largest bitcoin purchase announcement to date.

Led by executive chairman Michael Saylor, the company has continued its aggressive, near-weekly accumulation strategy, using capital markets activity to convert traditional financial assets into bitcoin exposure.

The latest purchase was funded through a combination of common stock issuance and sales of the company’s perpetual preferred equity, Stretch (STRC).

According to regulatory filings, the company raised about $2.125 billion in net proceeds between Jan. 12 and Jan. 19 through its at-the-market (ATM) programs. The bulk of the funds came from the sale of 10.4 million shares of MSTR Class A common stock, generating approximately $1.83 billion.

An additional $294.3 million was raised through the issuance of roughly 2.95 million STRC preferred shares. Smaller amounts were generated via STRK preferred stock, while no shares were issued under the STRF or STRD programs during the period.

Despite the continued accumulation, Strategy shares were under pressure in early trading, falling about 5% as bitcoin prices slid below $91,000. The pullback follows a broader crypto market sell-off after BTC traded above $94,000 late last week.

With more than 709,000 bitcoin now held, Strategy controls over 3% of bitcoin’s total circulating supply.

Several weeks ago, the company also announced they are increasing their U.S. dollar reserve to $2.25 billion, up from $1.44 billion in December, intended to support dividend payments on preferred shares and interest obligations on outstanding debt.

BREAKING:

— Bitcoin Magazine (@BitcoinMagazine) January 20, 2026STRATEGY BUYS ANOTHER 22,305 #BITCOIN FOR $2.1B pic.twitter.com/Rt9XSMP7QK

Earlier this month, the company was relieved of some selling pressure when MSCI concluded its review of digital asset treasury companies and decided not to exclude them from its major global equity indexes.

The index provider said bitcoin-heavy firms will remain eligible under existing rules while it conducts further research on how to distinguish operating companies from investment-like entities.

The decision eased months of market anxiety after MSCI had proposed reclassifying companies with more than 50% of assets in digital assets as fund-like and therefore ineligible for inclusion.

Companies like Strategy, along with industry groups, pushed back strongly, warning that exclusions could trigger billions of dollars in forced passive selling.

Spends $2.13 Billion to Buy 22,305 Bitcoin 2")

This post Michael Saylor’s Strategy ($MSTR) Spends $2.13 Billion to Buy 22,305 Bitcoin first appeared on Bitcoin Magazine and is written by Micah Zimmerman.

Billionaire Michael Saylor’s Strategy has added another 22,305 bitcoin to its balance sheet spending approximately $2.13 billion as the company continues its aggressive accumulation strategy.

Strategy has acquired 22,305 BTC for ~$2.13 billion at ~$95,284 per bitcoin. As of 1/19/2026, we hodl 709,715 $BTC acquired for ~$53.92 billion at ~$75,979 per bitcoin. $MSTR $STRC $STRK $STRF $STRD $STRE https://t.co/6hpAeOxp2I

— Strategy (@Strategy) January 20, 2026

The purchase disclosed on January 20, follows sales conducted under Strategy’s at-the-market (ATM) equity and preferred stock programs between January 12 and January 19, 2026. The bitcoin was acquired at an average price of approximately $95,284 per BTC, inclusive of fees and expenses.

As of January 19, Strategy now holds a total of 709,715 bitcoin acquired for roughly $53.92 billion at an average price of $75,979 per BTC.

According to the filing, Strategy raised approximately $2.125 billion in net proceeds during the period through a combination of equity and preferred stock issuance. The majority of capital was generated through sales of STRC variable-rate preferred shares and MSTR Class A common stock.

Notably, Strategy sold 2.95 million STRC shares for $294.3 million in net proceeds and issued 10.4 million MSTR shares, generating $1.83 billion. Smaller amounts were raised through STRK preferred stock sales, while no issuance occurred under STRF or STRD during the period.

The company confirmed that proceeds from the ATM program were used directly to fund bitcoin purchases, reinforcing its long-standing capital markets-to-bitcoin conversion strategy.

With the latest acquisition, Strategy’s bitcoin holdings have grown by more than 22,000 BTC in a single week, cementing its position as the largest corporate holder of bitcoin globally.

At current levels, the company’s aggregate holdings represent over 3% of bitcoin’s total circulating supply. While the average purchase price of recent acquisitions sits above Strategy’s historical cost basis, management has repeatedly emphasized long-term accumulation over short-term price sensitivity.

The disclosure shows that while the latest tranche was acquired near recent market highs, Strategy’s blended acquisition price remains materially lower due to earlier purchases made at discounted levels.

Strategy’s continued use of preferred stock issuance and equity sales reflects a deliberate effort to diversify funding sources while minimizing operational cash flow dependence.

The firm still has more than $8.4 billion of MSTR stock and billions in preferred securities available for future issuance under its ATM programs.

Despite heightened volatility in crypto markets and ongoing regulatory uncertainty, Strategy has maintained its bitcoin-centric capital allocation framework, positioning BTC as its primary treasury reserve asset.

The latest purchase shows Strategy’s unwavering conviction in bitcoin as a long-duration store of value and monetary asset. By systematically converting capital raised in traditional markets into bitcoin exposure, the company continues to operate as a leveraged proxy for institutional bitcoin adoption.

As of January 19, Strategy’s balance sheet reflects not just scale but persistence — a defining feature of its approach as bitcoin enters a more institutionally driven phase of market maturity.

The post Billionaire Michael Saylor’s Strategy Buys 22,305 Bitcoin for $2 Billion – Is Something Big Coming? appeared first on Cryptonews.

I remind CIOs, “You will always be transforming.” Every two years, new business drivers emerge, such as the pandemic from 2020-2022 and automation-driven efficiencies from 2023-2024. We’re now in the gen AI era, where most CIOs are under pressure to shift from driving broad experiments to delivering business value and ROI.

As a result, CIOs need to refocus their strategies and communicate an updated vision for transformation. My 2025 article on what’s in and out for digital transformation stressed the importance of developing transformational leaders and AI-ready employees while avoiding AI moonshots and ending lift-and-shift cloud migrations.

In 2026, experts suggest that CIOs must transform IT, transition AI to customer experience (CX) opportunities, and double down on data governance and security.

In 2025, I wrote about how AI is the end of IT as we know it and how CIOs are rethinking IT for the agentic AI era. World-class IT organizations are setting higher expectations, partnering with departments on AI change management, and committing to lifelong learning.

With all the AI innovations impacting IT, CIOs will need to refocus their digital operating models to deliver more capabilities faster, at lower cost, and with higher resiliency.

Sesh Tirumala, CIO at Western Digital, says, “Velocity gets us ahead, resilience keeps us steady, and adaptability ensures we stay ahead. Direction matters, and in 2026, velocity is the real currency of success.”

How can CIOs aim higher when CEOs and boards are demanding ROI from AI? Jay Upchurch, CIO at SAS, says the best and brightest CIOs will snap up commercial responsibilities. “Top CIOs will sell customers and their divisional peers on technology like CMOs, and answer the constant call to do more with less like CFOs.”

I expect many CIOs will reorganize IT in 2026. Some will be mandated to reduce costs and headcount, while others will drive efficient collaboration in their product management, agile, and DevOps practices. Top CIOs will seek opportunities to guide reorganization across the enterprise as agentic AI creates new workflow patterns and cross-department collaboration opportunities.

“CEOs will conclude that AI adoption is no longer a technology problem but a workforce and management problem,” says Florian Douetteau, co-founder and CEO of Dataiku. “Instead of selling cloud migrations and data platforms, consultants will start selling organizational rewiring to prepare for AI-run operations. This shift creates tension inside enterprises because it surfaces the real blocker: leadership culture, not technology.”

Raja Roy, senior managing partner in the office of technology excellence at Concentrix, adds, “The new priority: operating models that support rapid learning, collaboration, and real-time evolution, keeping the human/AI balance aligned to the right tasks, whether an interaction calls for a human touch or machine efficiency.”

Recommendation: CIOs should review IT’s structure and agile practices to increase the effectiveness of delivering AI innovations and improve operational resilience.

Data governance is a critical function in global regulated enterprises, where governance, risk, and compliance (GRC) are critical top-down mandates. Midsize organizations are catching up, as they evolve to data-driven organizations and centralize data for AI initiatives.

While governing relational databases and warehouses is a relatively mature process, deploying agentic AI capabilities requires new tools and practices to extend data governance to unstructured data sources.

“Unstructured data now moves too fast for manual oversight, and organizations can finally govern it as it’s created instead of cleaning it up later,” says Felix Van de Maele, CEO of Collibra. “In 2026, human judgment still matters, but AI-assisted systems, not spreadsheets or static controls, will carry the day-to-day load.”

Van de Maele suggests that AI-powered metadata generation for unstructured data, with integrated data practices for building reliable AI at scale is in, while CIOs should move away from manual tagging, siloed datasets, and one-time compliance efforts.

Additionally, many data governance leaders must get more granular controls on who gets access to what data. Authorizing users to full datasets and file systems is no longer sufficient as more organizations deploy AI agents on top of whatever data an employee can access.

“Many organizations do not know where their sensitive data lives, who can access it, or how much is exposed across cloud and SaaS systems,” says Yair Cohen, co-founder and VP of product at Sentra. “Leaders in 2026 will treat governance as an engineering practice by embedding classification, tagging, and access rules directly into data pipelines, warehouses, and AI workflows.”

Recommendation: CIOs should be paranoid about data risks, take a sponsorship role in data governance, and ensure that improving data quality is prioritized in every AI initiative.

In 2025, I warned CIOs about promoting AI as a driver of productivity and efficiency. Eventually, the CFO wants to see ROI, and this is one reason we saw significant technology layoffs in 2025.

I compiled over 50 expert predictions around 2026 on AI, from agentic workflows improving operations through gen AI embedded in customer experiences. I believe AI will have its Uber and Airbnb moment in 2026, as startups revolutionize customer experiences and disrupt slower-moving business-to-consumer (B2C) enterprises.

One easy way to embrace AI-enabled customer experiences is to upgrade call centers and chatbots without major infrastructure investments. Rob Scudiere, CTO at Verint, says, “Brands can layer an AI-powered chatbot onto their existing application instead of replacing an outdated telephony system and interactive voice response (IVR).”

When considering improving customer experiences, Pasquale DeMaio, VP of Amazon Connect, says to embrace systems that leverage AI and human strengths. “In customer support, agentic AI will manage routine requests while human agents will address complex issues with empathy and nuance, guided by AI insights and recommendations.”

CIOs should recognize a paradigm shift in UX, as data entry forms, customer journeys, and prescriptive reports get replaced with agentic AI capabilities. Focusing on AI in customer support is an easy entry point, as the entire customer experience, especially in ecommerce and SaaS tools, requires redesigning with AI capabilities.

“AI agents will become the frontend of the company as the primary starting point for any and all external contact,” says Antoine Nasr, head of AI at Forethought. “End-users will no longer have to try and navigate to the correct department and tool to get the help or information they need — they will simply interact with the company’s public AI agent in natural language. With that, agent design will become a key concern for several functions, not just customer support.”

Recommendation: Product-based IT organizations are a step ahead in anticipating how AI will evolve CX, and they should plan to segment and learn from early AI adopters.

Several research reports in 2025 highlighted how few AI experiments are being deployed into production and delivering business value. CEOs and boards will demand that CIOs narrow the portfolio of AI experiments and have real plans to deliver ROI from AI investments.

Conal Gallagher, CISO and CIO at Flexera, says in the next era of AI, execution matters more than experimentation. “CIOs will only continue to face bigger challenges and pressure to move beyond the AI experimentation phase and deliver clear, actionable, and measurable business outcomes.”

AI agents from top enterprise SaaS and security companies follow common patterns. These AI agents focus on a primary employee workflow, connect to multiple data sources, and aim to do more than complete tasks. CIOs will have to demonstrate the business value of how these AI agents guide employees in making smarter, faster decisions and the financial impacts of AI-revolutionized workflows.

“Agentic AI delivers measurable ROI in months, not years, because it replaces entire processes, not just parts of them,” says Luke Norris, co-founder and CEO of KamiwazaAI. “Each successful deployment accelerates the next, creating a self-funding innovation loop. More and more enterprises will be realizing this compounding ROI in the coming 6-12 months.”

Experts offer guidance on transitioning from an experimental to an outcome-based mindset. Kerry Brown, transformation evangelist at Celonis, says after years of big AI investment, it’s time to rethink end-to-end processes rather than just adding more automation on top.

“Leaders need to empower employees with visibility into how work really happens, and give them ownership in redesigning it,” says Brown. “When teams have that context and agency, they become true drivers of transformation and help create a faster, more direct path to ROI.”

Ed Frederici, CTO at Appfire, adds, “What’s out in 2026 is treating AI as a standalone, isolated initiative, and the next wave of digital transformation moves beyond scattered pilots to full operational integration. CIOs will treat AI as core business infrastructure rather than a special project — holding it to the same expectations for accuracy, security, and performance as every other critical system.”

Recommendation: Organizations with too many independently running AI experiments should revisit their AI governance strategy, communicate clear objectives, and prioritize where to build AI delivery plans.

Nearly every transformational technology started with a gold rush to deliver innovations, and bolting on security afterward. CIOs will face pressure to move last year’s AI experiments into production this year, and we’ll have to see to what extent security will be implemented in initial deployments.

Many experts chimed in on where CIO’s need to get ahead of the curve. Here are three recommendations:

Recommendation: CIOs must partner with CISOs, legal, and risk management to clearly define AI security non-negotiables, platforms, and implementation requirements.

CIOs should expect the unexpected in 2026, whether driven by volatile economic conditions, new AI capabilities, or headline-making security incidents. My back-to-basics recommendations for digital transformation in 2026 aim to guide CIOs toward growth opportunities while improving operational resiliency.

수십 년 동안 IT 운영 매뉴얼은 대개 50페이지 분량의 빽빽한 PDF 문서였다. 사람이 만들고 사람이 읽도록 설계된 문서는, 감사가 필요해질 때까지 디지털 저장소 어딘가에서 방치되는 경우가 대부분이었다. 그러나 2026년에 접어든 지금, 전통적인 SOP는 사실상 수명을 다한 상태다. 이제 이 매뉴얼의 주된 사용자가 사람이 아니기 때문이다.

시스템은 점점 더 에이전트 기반으로 진화하고 있다. 단순히 대시보드를 감시하는 수준을 넘어, 스스로 사고하고 계획하며 인프라 내 변경을 실행하는 자율형 에이전트가 배치되고 있다. 이들 에이전트는 PDF 문서를 읽을 수 없고, 법률 용어로 작성된 보안 정책의 취지를 해석하지도 못한다. 자율형 IT 시대에 통제력을 유지하려면 고정된 규칙에 머무르지 않고 ‘에이전트 헌법’, 즉 앤트로픽이 제시한 ‘헌법 중심 AI(Constitutional AI)’를 기업 환경에 적용해야 한다. 이는 AI의 문제점을 AI가 스스로 검증하고 고치기 위한 시스템을 의미한다.

과거 IT 거버넌스는 사후 대응만 가능한 ‘체크리스트’ 방식이었다. 그러나 오늘날 기업은 정책을 코드로 구현하는 ‘PaC(Policy as Code)’로의 전환이 필요하다.

이런 전환은 근본적인 변화를 의미한다. IT 전문가의 역할은 ‘운영자’에서 ‘의도 설계자’로 변화하고 있다. IT 직원은 더 이상 시스템을 직접 조작하는 사람이 아니라, 자율 시스템이 따라야 할 행동 규칙을 설계하는 주체가 되고 있다.

기업이 ‘킬 스위치’에 대한 통제권을 유지하면서 AI 역량을 확장하려면, ‘자율성의 계층 구조’에 초점을 맞출 필요가 있다. 이는 1978년 연구자 토머스 셰리던와 윌리엄 버플랭크의 기초 연구에서 제시된 프레임워크에 기반한 개념이다.

중앙화된 헌법 체계를 구현하면, 중앙 IT의 관리 및 감독 없이 배포되는 섀도우 AI 에이전트로 인한 리스크를 완화할 수 있다.

이른바 ‘헌법’은 코드가 아니라, 엔지니어의 경험과 판단이 집약된 사람의 문서다. 따라서 사람의 역할은 여전히 중요하다.

2020년대 후반에도 PDF 형식의 기존 SOP에 의존한다면, IT 운영은 비즈니스의 발목을 잡는 병목으로 전락할 가능성이 크다.

지금 바로 취해야 할 단계는 다음과 같다.

dl-ciokorea@foundryco.com

Ed Forst never served in the Navy, but the metaphor he uses to describe the role the General Services Administration would make any admiral proud.

Forst, who has been at the helm of GSA since late December, believes agencies, like ships, have two distinct compartments. One is to focus on the mission. The other is the engine room that makes the mission run.

“I think in every business, every enterprise, every agency, every department, and what I think makes great sense, and I believe the President does too, is, let’s advance mission and let’s have the engine room, what’s behind the curtain, consolidate and get even better. That’s where I see GSA in the federal government. We’re the engine room,” Forst said at the Coalition for Common Sense in Government Procurement winter conference on Jan. 14. “Now, interestingly, GSA is its own agency, so we happen to have both. We’ve got mission and the engine room as well. So I think because of that, we really do appreciate the mission piece of that and serving our stakeholders and our constituents.”

For GSA, being that engine room in part means making acquisition less burdensome, cheaper and more agile so agency customers can meet their mission needs more quickly.

GSA has been pursuing several initiatives over the last year to fine tune the acquisition piece of the engine room.

Laura Stanton, the deputy commissioner of GSA’s Federal Acquisition Service, said between the Office of Centralized Acquisition Services (OCAS), the OneGov initiative and the implementation of changes from the Federal Acquisition Regulation rewrite, GSA is delivering speed to acquisition like never before.

For example, OCAS now centrally buys for three agencies: the Office of Personnel Management, the Small Business Administration and the Department of Housing and Urban Development. Stanton said GSA brought on OPM and SBA in about a month.

Stanton said OCAS is using an opt-in approach to help agencies and trying to relieve some of the burden on GSA’s Assisted Acquisition Service.

“We’re having conversations with a number of agencies about what are their needs. One of the things that we set up OCAS to be able to support is the buying of common goods and services,” Stanton said. “We also recognize that there are mission critical items that and there’s common things that are mission critical that can be used for governmentwide contracts, and then things where there are specialized contracts. So we’re having those types of conversations with a number of agencies at this point.”

Under the OneGov program, GSA has signed 18 agreements to reduce the price of commonly used software across government. Additionally, 45 agencies have taken advantage specifically of the enterprisewide agreements for artificial intelligence tools.

“This is a radical shift in how we think about it, and how we think about how we come to market, and also how we want you to treat us as a customer,” Stanton said at the conference. “This requires changes, not only on the government side, but it’s also going to require changes on the industry side to make that happen. We want to be better aligned when it comes to terms pricing and performance, when it comes to all aspects of that.”

Forst said he was especially focused on the performance aspects of the equation for GSA.

He said measuring performance, and holding organizations and people accountable are among his key focuses areas.

“We’re putting out some priorities for having deliverables. I’m committing every quarter and I’m going to report on ourselves on that,” he said. “I think we’re all better if we find a way to talk about measurement or metrics, whatever you want to call it. There’s a common language and vocabulary about that, so I am a big proponent.”

Forst said he will be looking at both the performance of FAS in terms of “revenue,” as well as their performance relative to peer organizations.

“If you had a record year, you’d probably beat plan. All that should be good. That’s absolute measurement. That’s you versus you. And I think that’s important. I think it’s also really important to accompany that with who’s in your peer group and how did they do? I think the relative performance matters a ton as well,” he said. “You could be down 7% and on an absolute basis, angst to death over down seven if your peer group’s down 15, that’s a home run. So I think it’s important. But if you had a record year and you’re up 6% and your peer group’s up 12%, I’d say good record, but you underdelivered versus the other side. I think we have to be honest with ourselves and look at both us versus us over the time series, and look at us versus a peer group. That seems to make sense.”

Forst said GSA plans to bring in a peer group analysis to raise their awareness and their overall performance.

The third piece of moving bringing speed to capability is the FAR rewrite. GSA will begin implementing the FAR changes within its own acquisition regulations in the coming weeks. It already issued deviations to the current FAR to begin the process.

Jeff Koses, GSA’s senior procurement executive, said in a post on LinkedIn that they have “limited the issuance of mandatory acquisition policies to my office, the Office of Acquisition Policy. Legacy mandatory policy will have to be reissued at the agency level, converted to discretionary guidance, or cancelled.”

Koses said GSA will begin culling down 500 pages of its acquisition manual, 300 pages of office policy, 500 pages of FAS policy and another 500 pages of Public Buildings Service policy and then 1,000 pages of real property leasing policy.

Larry Allen, the associate administrator in the Office of Governmentwide Policy, said at the CGP conference that GSA, in helping out the FAR Council, is working closely with OFPP to get all of the rulemaking completed by the end of the fiscal year.

“It may be delayed a little bit because we had a little shutdown in the fall, but that tells you exactly what type of timetable we are on. It’s aggressive, and you will see change, and we want you to be part of that change,” Allen said.

Stanton added that GSA understands the FAR rewrite has moved quickly and is addressing complex acquisition issues that will take time for government and industry to wrap their arms around.

“When we think about this year, it’s going to be a year of both adopting and adaptation, and acceleration all at the same time, and that becomes really challenging to do,” she said.

Stanton said another key initiative kicking into gear this year is GSA’s review of its multiple award schedule catalog. She said the driving theory is how can the agency operate it more efficiently and deliver more value to agency customers.

“I look at the at the catalog that we run for the multiple award schedule and it has over 100 million items in it. Only 1% or fewer of those items sell, and so this is putting burden on all of you, making sure that you’re meeting all of our terms and conditions, that those items are Trade Agreements Act (TAA) compliant, that they meet the government standards, and that the pricing is fair and reasonable,” she said. “We have contracting officers who have to evaluate those items, and what is the value that either you or the government is getting for that work? I think that this is a big opportunity for us to truly assess where is the government’s demand. As we’re also moving into making transactional data reporting mandatory, how do we effectively have a catalog that delivers on what the government needs? How do we meet those needs effectively? How do we move quickly if we have something that’s not in the catalog? It’s a lot easier to move quickly if we’re not burdened by putting things in there that are not actually being used.”

The post Forst: GSA is the ‘engine room’ that runs government first appeared on Federal News Network.

© AP Photo/Jacquelyn Martin, File