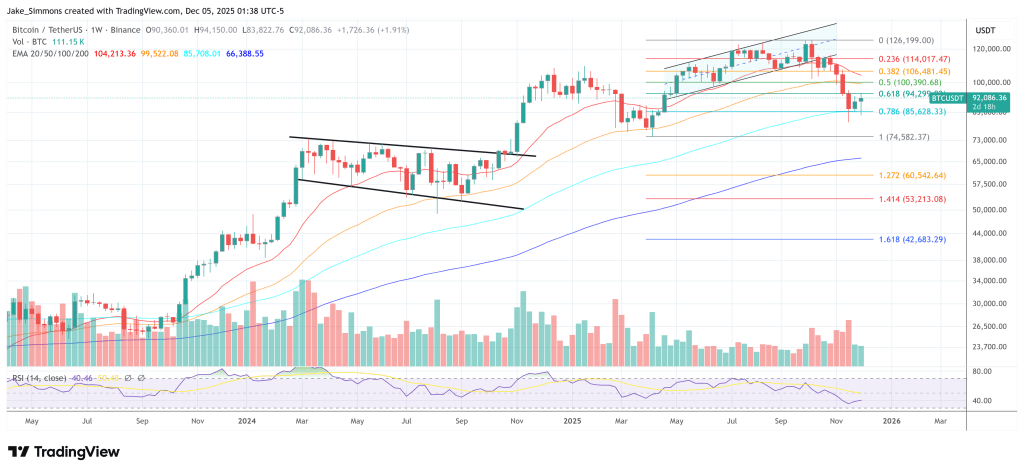

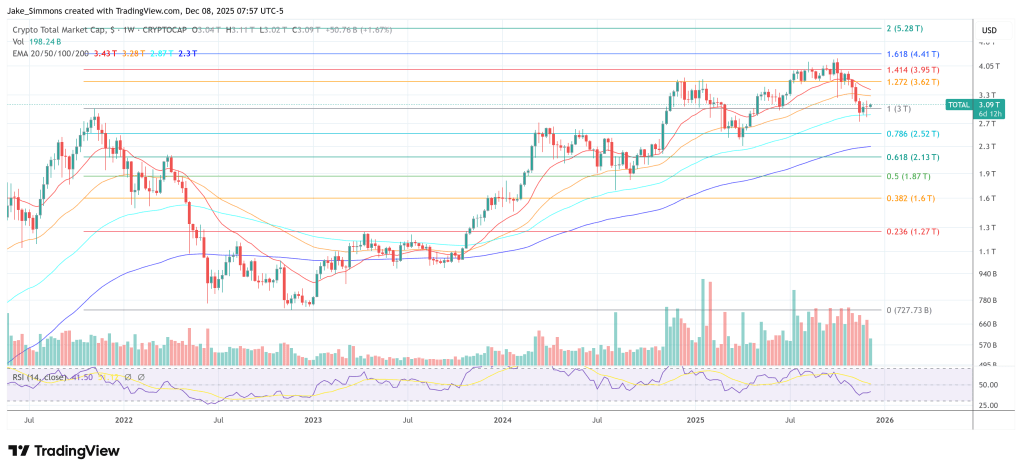

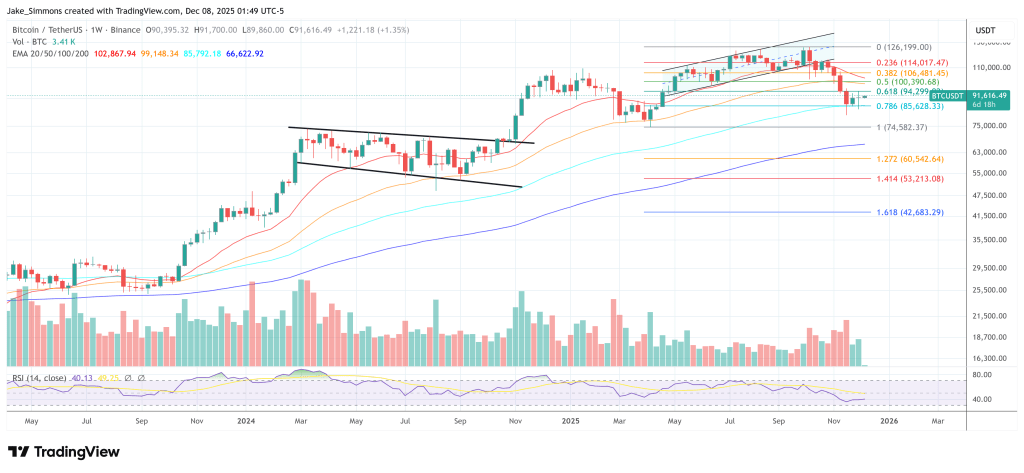

Standard Chartered has sharply reduced its famously bullish Bitcoin roadmap, cutting its 2026 price target in half and acknowledging that its previous near-term projections were too aggressive, even as it keeps an ultra-optimistic long-term view intact.

Standard Chartered Downgrades Bitcoin Price Predictions

In a note shared on X by VanEck head of research Matthew Sigel, Standard Chartered argues that Bitcoin’s traditional halving cycle has been overtaken by ETF-driven flows. The bank writes: “With the advent of ETF buying, we think the BTC halving cycle is no longer a relevant price driver. The logic in previous cycles (when US ETFs did not exist) – i.e., prices would peak about 18 months after each halving and decline thereafter – is no longer valid, in our view.”

The report adds that it will “take a break of the current all-time high ($ 126,000 on 6 October 2025) to prove that; we expect this to happen in H1-2026.”

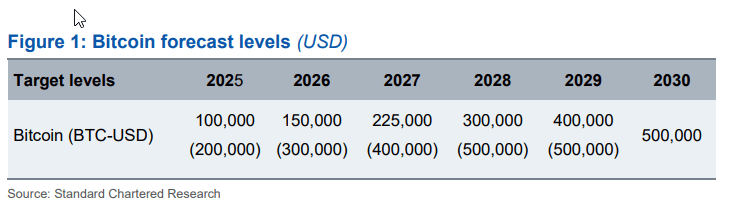

Alongside that shift in framework, the bank re-profiled its multi-year Bitcoin targets. According to the figures shared by Sigel, Standard Chartered has lowered its 2025 forecast from $200,000 to $100,000, its 2026 target from $300,000 to $150,000, its 2027 projection from $400,000 to $225,000, its 2028 estimate from $500,000 to $300,000, and its 2029 prediction from $500,000 to $400,000 while keeping a $500,000 target for 2030.

Geoff Kendrick, Standard Chartered’s head of digital assets research, characterises the recent drawdown as painful but not structural. He describes the current phase as “a cold breeze,” explicitly rejecting the notion of a new crypto winter and noting that the magnitude of the pullback remains consistent with corrections seen in past bull cycles.

At the same time, he points out that weaker valuations for listed Bitcoin treasury companies have curtailed their ability to act as major marginal buyers, leaving spot ETFs as the primary driver of near-term gains.

Wall Street Giant Bernstein Agrees

The downgrade also lands in the context of a broader rethink on Wall Street. One day earlier, on December 8, Sigel shared a separate note from Bernstein that reached a similar conclusion about Bitcoin’s market structure.

Bernstein wrote that “the Bitcoin cycle has broken the 4-year pattern (cycle peaking every 4 years) and is now in an elongated bull-cycle with more sticky institutional buying offsetting any retail panic selling.”

Despite an approximately 30% correction, the firm notes that “we have seen less than 5% outflows via ETFs.” On that basis, Bernstein now moves its 2026 Bitcoin price target to $150,000, sees the cycle “potentially peaking in 2027E at $200,000,” and keeps its long-term 2033 target at roughly $1,000,000 per BTC.

Both Standard Chartered and Bernstein are converging on the same structural message: the halving alone no longer explains Bitcoin’s trajectory. ETF flows, institutional positioning and balance-sheet dynamics are now the core variables, even if their precise price targets and timelines diverge.

Bitwise CIO Matt Hougan says the crypto market is anchored to the wrong mental model. Speaking on the Empire podcast recorded 5 December and released on 8 December, he argued that the traditional “four-year Bitcoin cycle” has lost its explanatory power – and that 2026, which many expect to be a brutal post-halving down year, is far more likely to be an “up year” driven by institutional flows and regulatory tailwinds.

“2026 will not be a bad year, Jason,” Hougan told host Jason Yanowitz. “I think 2026 will be a good year […] I just don’t understand the logical reason why [the four-year cycle] would repeat again. It’s not like built into a mechanical clock. It was driven by specific factors and those factors no longer exist, so it won’t keep happening.”

He acknowledged that recent price action has unnerved investors, with Bitcoin giving back a “Vanguard pump” and selling off into a weekend on no obvious news. But he framed that as positioning and microstructure, not the start of a structural unwind.

“People in crypto over the last two months have learned to be nervous on weekends,” he said, pointing to thin weekend liquidity and Friday macro headlines. He noted that sentiment is depressed even though “the market is flat for the year,” adding: “We’re freaking out about a market that is flat for the year.”

Why The 4-Year Crypto Cycle Is Dead

Hougan broke down the four main explanations traditionally used to justify the Bitcoin cycle and argued each is now materially weaker.

First is the halving itself. “The halving cycle is just not that important,” he said. “It’s half as important as it was four years ago […] a fraction of, you know, a quarter as important as it was eight years ago, a sixteenth, etc. There’s just not that much supply being removed.” As issuance becomes a smaller fraction of total supply and ETF and derivatives flows grow, the mechanical supply shock carries less weight.

Second is the rate cycle. Prior “down years” such as 2018 and 2022 coincided with aggressive rate hikes. “Interest rates are going down,” he said. “So that thesis is just completely invalidated, right? It’s completely different.”

Third is the “blow-up” pattern – Mt. Gox, ICOs, FTX – that historically capped euphoric phases. Hougan allowed that balance-sheet stress in parts of the market is “the strongest case for the four-year cycle repeating,” but he does not expect forced liquidations on the scale of prior collapses. In his view, potential problem entities are more likely to “just not buy as much in the future” rather than being compelled sellers.

Fourth is simple randomness: three similar cycles do not make a law of nature. “Across those four, they’re all much weaker than they were in the past,” he summarised.

Why 2026 Is Poised To Be Better Than 2025

Against that, Hougan set what he sees as a once-in-a-generation shift in regulation and institutional behaviour. “You have a once-in-a-generation regulatory change from severe regulatory headwinds to strong regulatory tailwinds,” he said, and “more importantly, you have this institutional adoption narrative that’s going to overwhelm everything.”

In the last six months, he noted, major US wirehouses have “green-lit crypto exposure.” He singled out Bank of America: “They have $3.5 trillion in assets. One percent is $35 billion. Four percent is like $140 billion. That’s more than the total flows into Bitcoin ETFs so far.” He stressed it is not just one bank: “There are four wirehouses. They’re basically all on now […] the biggest advisory groups all managing many trillions of dollars.”

The catch is timing. Institutional allocations are slow and process-driven. “The average Bitwise client, I think, invests after eight meetings with us,” he said, and some of those are quarterly. That “eight-meeting” lag means the ETF era is still in its early innings; the full impact of platforms being switched on is more likely to manifest through 2026 than in a single explosive quarter.

Hougan also emphasised that advisers optimise for client retention, not absolute performance. “The one thing a financial adviser doesn’t want to do is have a meeting with their client where something is down 50% and their client fires them,” he said. That is why reduced volatility, cleaner regulation and mainstream narratives like “Bitcoin as digital gold” and “stablecoins and tokenization as new financial rails” matter so much.

On supply dynamics, he pushed back on two recurring fears: “OG whales dumping” and MicroStrategy as a forced seller. He argued that much of the apparent “selling” by long-term holders is actually upside being sold via covered calls. Whales come to Bitwise and similar firms, he said, saying: “I have a hundred million of Bitcoin […] can you write covered calls against this?” That “effectively introduces new supply into the market” without coins moving on-chain.

On MicroStrategy, he was categorical: “From a data perspective [it is] just strictly untrue that it will be forced to sell its Bitcoin.” The company has meaningful cash to service interest, no principal due until 2027, and manageable maturities relative to its Bitcoin holdings. He agreed with Jeff Dorman’s framing that MicroStrategy is no longer a major marginal buyer but also “not a forced seller.”

Too much pessimism on the timeline.

Brought on @Matt_Hougan to tell us why 2026 will be FAR better than 2025.

Tons of good nuggets in here related to institutions, financial advisors, cycles, and more.

Looking ahead, Hougan expects investors to eventually reframe the current period not as a failed bull cycle but as a behavioural transition through a key level. “We might look back at 2025 at some point and say, ‘Huh, you know what? $100,000 was like a big behavioral cliff we had to get over. Took us like a year,’” he said.

For 2026 specifically, his message is clear: the old four-year pattern “won’t keep happening,” and the combination of regulatory clarity and institutional inflows sets up what he calls an “extraordinarily strong” backdrop rather than a programmed bust.

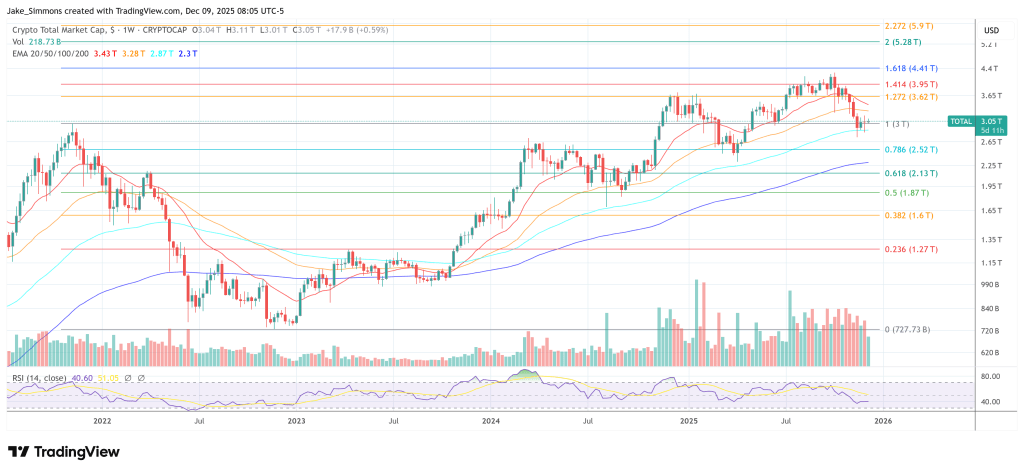

At press time, the total crypto market cap stood at $3.06 trillion.

Featured image from YouTube, chart from TradingView.com

The prospect of a “Trump Fed takeover” is rapidly becoming a central macro theme for 2026, with some traders arguing that markets still underestimate how radical the shift could be for global liquidity – and by extension for crypto.

Macro commentator plur daddy (@plur_daddy) describes it bluntly via X: “The Trump Fed takeover being underpriced is my primary theme going into 2026 (hence my gold bet). This is a momentous shift: the bigger and more convex the catalyst, the more difficult it is for markets to price it in properly.”

Former Fed trader Joseph Wang known as “Fed Guy” echoes the concern from inside the plumbing, warning: “The market underestimates the likelihood of a Trump Fed. The Administration is showing resourcefulness and determination for lower rates. That could set off the blow off top in equities, where implied vol shows speculation still has room to run.”

The Trump Fed Takeover Isn’t Price In

That determination is colliding with a bond market that appears to be pushing back via term premium. Plur highlights the spread between the 12-month T-bill and the 10-year Treasury as a clean gauge of that tension. He notes that the spread “peaked right before inauguration on the generic ‘Trump will run it hot’ viewpoint,” then “got crushed lower as DOGE and Tariffs got priced in.” It bottomed near the tariff lows and “is now back to the highs,” a pattern he reads as term-premium expansion as “a form of protest to [Kevin] Hassett,” Trump’s presumed Fed pick.

Against that backdrop, the administration still has powerful tools to compress term premium without formally announcing quantitative easing. Plur identifies three levers. First, de-regulating banks so they are allowed – in practice, pressured – to hold more Treasuries, boosting structural demand for government paper.

Second, reducing the Treasury’s weighted-average maturity by shifting issuance “to bills over longer dated notes,” which cuts the duration the market has to absorb. Third, specifically for mortgages, “lever up the GSEs to buy MBS,” narrowing mortgage spreads and transmitting easier policy to the housing market even if the policy rate moves more slowly. He argues that “all of these are quite bullish for risk overall but will take time to play out.”

For now, the environment remains awkward for directional risk bets, including crypto. “In the meantime, it has been a choppy and difficult market, across the board. Equity indices have grinded higher but the underlying rotations have been tricky to navigate. QT ended but liquidity is still relatively thin, and the fact that we are going into year end does not help. Better times will come.”

The bullish pivot in his framework arrives with the calendar. “In the new year, fiscal accommodation will re-expand on the implementation of OBBBA (+$10–15bn/mo). Meanwhile we have sell-side macro teams calling for $20–45bn/mo in T-bill repurchasing by the Fed, as soon as Jan 1.”

This mix would directly ease pressures visible in funding markets: “This would go a long way towards easing the current liquidity issues (see the SOFR–IORB spread chart below). This is not classic QE in that there is very little duration being absorbed from the private sector, and mainly has the effect of expanding bank reserves. This is still bullish because bank reserves are tight at the time, which is tied to the repo liquidity issues.”

Will The Crypto Market Rise Again?

On that basis, Plur expects the macro backdrop in 2026 to look “better than H2 ’25 has been, perhaps more on par with parts of 2024.” His expression of the trade is clear: “This should be enough for strong performance on gold given the Fed takeover angle, and continued melt-up in equities and select commodities.”

For Bitcoin and the broader crypto market, however, his stance is notably more cautious. “For BTC it is more difficult to say. My base case continues to be a frustrating period of chop and re-accumulation.” Improved liquidity “should be favorable for BTC,” but he questions whether there will be “a material shift in the supply/demand imbalances we have been seeing,” concluding: “I will keep watching it for now.”

In other words, the Trump Fed trade is already driving high-convexity bets in gold, equities and commodities. Crypto stands to benefit indirectly from easier reserves and lower term premium, but in this framework, the key constraint is no longer just macro liquidity – it is whether fresh demand is strong enough to meet an increasingly inelastic supply in the crypto market.

At press time, the total crypto market cap stood at $3.05 trillion.

Wall Street research firm Bernstein has reiterated one of the boldest long-term calls in traditional finance, confirming a $1 million Bitcoin price target for 2033 while materially revising how and when it expects the market to get there.

Bernstein Keeps $1 Million Price Target For Bitcoin

The latest shift surfaced after Matthew Sigel, head of digital assets research at VanEck, shared an excerpt from a new Bernstein note on X. In it, the analysts write: “In view of recent market correction, we believe, the Bitcoin cycle has broken the 4-year pattern (cycle peaking every 4 years) and is now in an elongated bull-cycle with more sticky institutional buying offsetting any retail panic selling.”

The analyst from Bernstein added: “Despite a ~30% Bitcoin correction, we have seen less than 5% outflows via ETFs. We are moving our 2026E Bitcoin price target to $150,000, with the cycle potentially peaking in 2027E at $200,000. Our long term 2033E Bitcoin price target remains ~$1,000,000.”

This marks a clear evolution from Bernstein’s earlier cycle roadmap. In mid-2024, when the firm first laid out the $1 million-by-2033 thesis as part of its initiation on MicroStrategy, it projected a “cycle-high” of around $200,000 by 2025, up from an already-optimistic $150,000 target, explicitly driven by strong US spot ETF inflows and constrained supply.

Subsequent commentary reiterated that path and framed Bitcoin firmly within the traditional four-year halving rhythm: ETF demand would supercharge, but not fundamentally alter, the classic post-halving boom-and-bust pattern.

Reality forced an adjustment. Bitcoin did break to new highs on the back of ETF demand, validating Bernstein’s structural call that regulated spot products would be a decisive catalyst. However, price action has fallen short of the earlier timing: the market topped out in the mid-$120,000s rather than the $200,000 band originally envisaged for 2025, and a roughly 30% drawdown followed.

What changed is not the end-state, but the path. Bernstein now argues that the four-year template has been superseded by a longer, ETF-anchored bull cycle. The critical datapoint underpinning this view is behavior in the recent correction: despite a near one-third price decline, spot Bitcoin ETFs have seen only about 5% net outflows, which the firm interprets as evidence of “sticky” institutional capital rather than the reflexive retail capitulation that defined previous tops.

In the new framework, earlier targets are effectively rescheduled rather than abandoned. The mid-2020s six-figure region is shifted out by roughly one to two years, with $150,000 now penciled in for 2026 and a potential cycle peak near $200,000 in 2027, while the 2033 $1 million objective is left unchanged.

In that sense, Bernstein’s track record is mixed but internally consistent. The firm has been directionally right on the drivers—ETF adoption, institutionalization, and supply absorption—but too aggressive on the speed at which those forces would translate into price. The latest note formalizes that recognition: same destination, slower ascent, and a Bitcoin market that Bernstein now sees as governed less by halvings and more by the behavior of large, ETF-mediated capital pools over the rest of the decade.

In a fireside chat with Metaplanet CEO Simon Gerovich at BTC MENA 2025, Michael Saylor turned a technical conversation about Bitcoin treasuries into a direct pitch to the Middle East’s sovereign wealth funds and banks, outlining how a nation or large financial institution could attract tens of trillions of dollars and become the “Switzerland” of digital capital.

Saylor and Gerovich began by framing Bitcoin as “digital capital.” As Saylor put it, “Our company pursued a strategy of accumulating digital capital. Bitcoin is digital capital. What do you do when you have capital? You issue credit against it.” Both MicroStrategy and Metaplanet are building balance sheets of Bitcoin and then issuing perpetual preferred instruments as “digital credit” backed by that capital.

Gerovich described Japan as a massive but yield-starved market. “There’s $7 trillion of cash sitting on personal bank accounts, bank balance sheets earning nothing, and corporates have another $4 or $5 trillion.” A Japanese family that puts money in the bank gets “zero.” Even as deflation fades, investors remain “accustomed to zero” and are “desperately looking for yield.”

Metaplanet’s answer is to connect that idle capital to Bitcoin. It launched “Mercury,” a perpetual preferred paying 4.9% in yen with convertibility into equity, which Gerovich called “probably one of the cheapest call options on Bitcoin out there.” Its follow-up product, “Mars” – Metaplanet Adjustable Rate Securities – is designed as a high-yield, Bitcoin-backed instrument that Japanese investors can hold in their securities accounts as a kind of supercharged bank deposit.

Inside Saylor’s Bitcoin Talks With Sovereign Funds

Saylor used this as a template for the Middle East, explaining that he has been on an intensive tour of the region’s power centers. “I’ve been meeting with all the sovereign wealth funds. I’ve been meeting with, I don’t know, 50, 100 different investors, hedge funds, family office investors… I’ve been meeting with regulators in every jurisdiction.” His message is “very, very straightforward”: “We now have digital capital. Bitcoin is digital capital, is digital gold. On top of digital capital, we have a new asset class called digital credit. Digital credit strips the volatility from the capital and provides yield, income.”

To illustrate the appeal, he contrasted capital and credit. Giving a child $1 million of Manhattan land is pure capital with no cash flow. “Or you can give them a credit instrument that pays them $10,000 a month forever, starting now. And so most people want the credit instrument. They don’t want the capital instrument… They’d rather have 10% non-volatile than 30% volatile with no cash flows.” Treasury companies like MicroStrategy and Metaplanet “exist to convert capital into credit.”

Saylor then laid out the blueprint for any ambitious bank in the region: “Have the bank custody Bitcoin. Everybody talks about self-custody. Self-custody for the bank in the country. Buy Bitcoin, have your bank custody the Bitcoin, and then start to offer credit networks on top of the Bitcoin.” If a national bank extends loans such as “SOFR plus 50 basis point loans on Bitcoin,” he argued, then as Bitcoin’s market grows from $2 trillion to $20 trillion, that bank could attract “5% or 10% of it,” pulling in “a trillion dollars or a few trillion dollars” simply because “most big conventional regulated banks don’t handle Bitcoin.”

The “biggest idea” is to turn Bitcoin-backed credit into a bank account that outcompetes the entire global deposit system. By taking digital credit instruments like Stretch or Mars, placing them in a fund that is mostly credit with a currency buffer and reserve layer, Saylor envisions a regulated account that pays around 8% with “vol of zero.” In that setup, “I wire you my billions of dollars or tens of billions of dollars, and you pay me 8% interest every day, zero vol, in a regulated bank, powered by digital credit, which is in turn powered by a treasury company with 5x as much digital capital, over-collateralized.”

In such a regime, he argued, “you could presumably attract 20 trillion dollars or 50 trillion dollars.” For depositors, “the perfect product is a bank account with zero volatility that pays you 400 basis points more than the risk-free rate in your favorite currency.” For Saylor, that account is “the lightsaber of money, the laser beam of money, the nuclear fusion reactor of money.”

He framed it as an open race: “The question is, who wants to be the Switzerland of the 21st century and attract all the money in the world?” In his view, “the answer is going to be whoever appreciates money the most, wants the money the most, that understands technology the best, that is willing to take a courageous stance of conviction with a degree of clarity,” he said.

He concluded: “That is the opportunity, and all the conversations have been extraordinarily energetic, enthusiastic, and I couldn’t be more excited. I think it will happen somewhere in this region. We’ll see where.”

In this powerful fireside chat from the Bitcoin for Corporations Symposium at Bitcoin MENA December 2025, Michael Saylor Executive Chairman of Strategy and S...

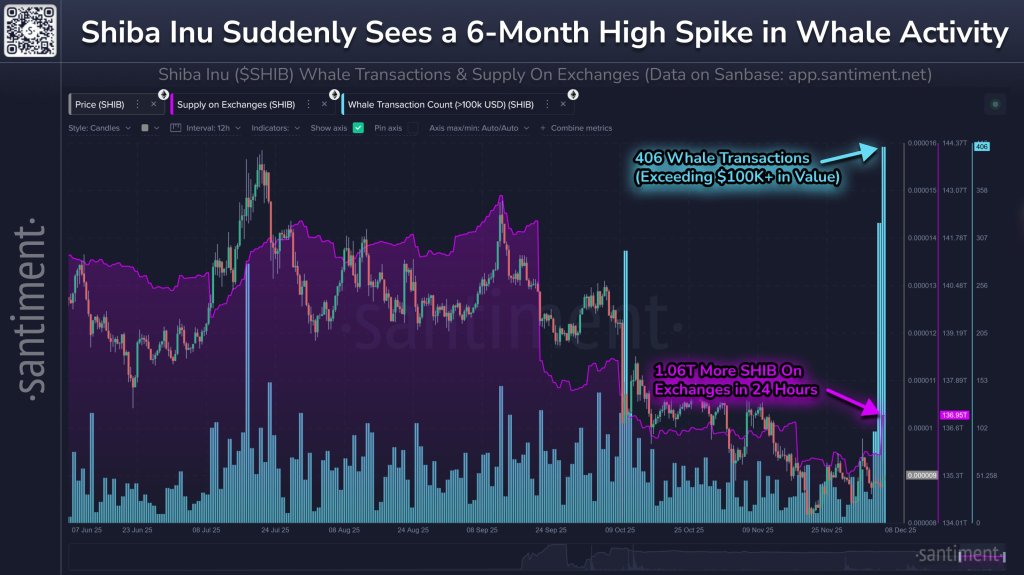

Shiba Inu has just logged its most intense burst of large-holder activity in half a year, raising questions over whether fresh volatility – and potentially renewed selling pressure – is around the corner.

On-chain analytics firm Santiment reported the move on X, highlighting a six-month chart of Shiba Inu’s price, exchange balances and large transfers. According to the firm, “Shiba Inu has seen the highest amount of whale transfers since June 6th today, happening in tandem with a +1.06T net change to the amount of SHIB on exchanges. The #24 market cap in crypto is likely to see high volatility in the coming days.”

What Does This Mean For The Shiba Inu Price?

The chart shows 406 individual transactions exceeding $100,000 in value within a single day, the highest reading since early June. The second-highest peak occurred during the October 10 market meltdown, when roughly 300 SHIB whales were active, and the third came in mid-July, as more than 280 whales executed transfers.

These “whale” transfers represent activity from large holders, trading desks and liquidity providers whose moves can materially affect market liquidity and order-book depth.

At the same time, Shiba Inu’s exchange supply has jumped. Santiment’s overlay of “Supply on Exchanges (SHIB)” reveals a clear, abrupt uptick, annotated as “1.06T More SHIB On Exchanges in 24 Hours.” This reflects a net inflow of around 1.06 trillion tokens into exchange wallets, meaning more SHIB is now sitting in venues where it can be traded immediately.

In market-structure terms, the combination of record recent whale activity and a sharp rise in exchange balances creates conditions that often precede significant price swings. Moving coins from self-custody to exchanges does not guarantee that they will be sold, but it increases the portion of circulating supply that is “sale-ready” and able to hit the order books at short notice.

Whether that translates into an outright dump is not yet visible on-chain. The same footprint could reflect whales preparing to sell, to arbitrage across venues, to supply liquidity, or to rebalance positions in anticipation of broader market moves. Santiment itself stops short of a directional call, limiting its guidance to the expectation that the Shiba Inu token “is likely to see high volatility in the coming days.”

For now, the data point is clear: Shiba Inu’s largest holders have become more active than at any time since early June, and over a trillion additional tokens have shifted onto exchanges in just 24 hours. The direction of the next major move will depend on how that newly mobile supply is deployed.

Ripple has become the most aggressively structured bet in blue-chip crypto after a group of major Wall Street firms wired about $500 million into the company in November, lifting its valuation to roughly $40 billion and making it one of the highest-valued private players in the sector. Bloomberg reported that Ripple’s share sale brought in some of the biggest names of Wall Street but only after investors secured a suite of downside protections.

Wall Street Goes All-In On Ripple

The investor line-up reads like a who’s who of modern market structure: Citadel Securities, Fortress Investment Group, Marshall Wace, Brevan Howard–linked vehicles, Galaxy Digital and Pantera Capital all participated, treating the round at least as much as a structured credit trade as a venture bet.

According to multiple accounts of the deal, several funds underwrote Ripple essentially as a concentrated exposure to XRP itself. Bloomberg’s reporting states that multiple investors concluded at least 90% of Ripple’s net asset value was tied to XRP, with the company controlling about $124 billion of the token at market prices in July.

That XRP cushion has already been tested. XRP is down roughly 40% from its mid-July peak and about 15–16% since late October, yet even after that drawdown, estimates in deal coverage still put the company’s XRP treasury in the tens of billions of dollars, with a large portion locked in escrow and released gradually over time.

The protection that Wall Street insisted on has become the defining feature of the deal. Investors secured the right to sell their shares back to Ripple after three or four years at a guaranteed 10% annualized return, unless the company has gone public by then.

Ripple, conversely, can force a buyback in those same windows only by delivering about 25% annually. On top of that, the funds negotiated a liquidation preference, giving them priority over legacy shareholders in a sale or insolvency.

The numbers involved are non-trivial. FinTech Weekly estimates that if the put option were exercised in full at the four-year mark, Ripple’s cash outlay would approach $700 million–$730 million, irrespective of operating performance or token prices at the time. Those obligations sit alongside an already heavy capital agenda: Ripple has agreed to buy prime-brokerage platform Hidden Road for roughly $1.3 billion and corporate-treasury specialist GTreasury for about $1 billion, while also confirming it has repurchased more than 25% of its outstanding shares.

Banks and trading desks are now treating the November round as a new reference point for crypto credit risk. FinTech Weekly reports that “those terms are now shaping how banks, funds, and trading desks assess Ripple’s balance sheet, exit risk, and future liquidity,” with the three- and four-year exit windows being modeled explicitly alongside XRP price scenarios and rate curves.

Ripple’s management maintains there is “no plan, no timeline” for an IPO, but the structure of the deal effectively date-stamps its private capital: either the company lists or finds new liquidity on favorable terms before the put windows open, or it must fund a secured, fixed-return exit for some of the most sophisticated players on Wall Street.

The coming week concentrates macro and protocol-specific catalysts into a tight window, with the Federal Reserve’s FOMC decision and several high-profile project events landing between December 10 and 12.

#1 Crypto On Alert: Fed’s Dec. 10 Rate Decision

The US Federal Reserve’s FOMC interest rate decision on Dec. 10 looms as a key macro catalyst for crypto. Markets overwhelmingly expect a 25 bps rate cut – about an 87% probability according to Fed funds futures– which would lower the target rate to ~3.5–3.75%. Such a move would be the third cut in as many meetings, signaling a pivot to easing as the Fed prioritizes a faltering job market over inflation.

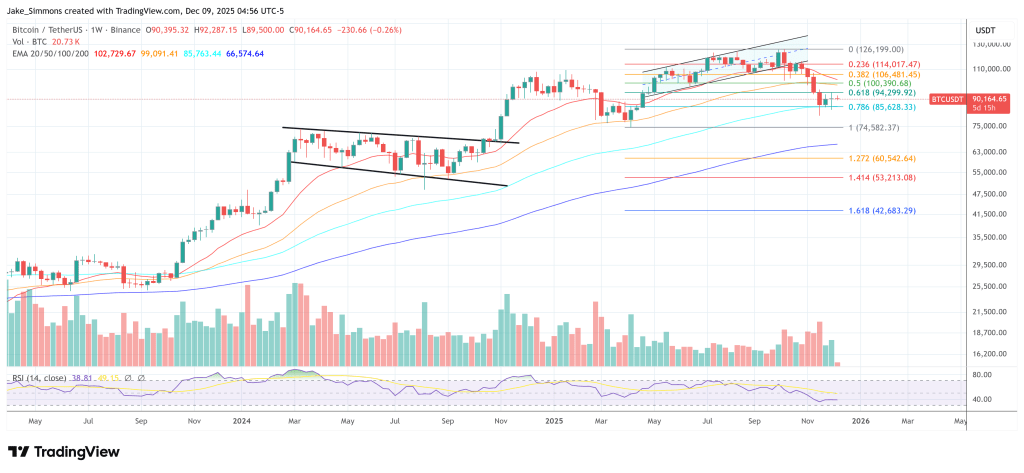

Bitcoin (BTC) has historically reacted sharply to Fed surprises: BTC often faces downward pressure into FOMC announcements, then significant volatility as markets parse the Fed’s language. Indeed, ahead of this meeting, BTC dipped below $88,000 over the weekend on “FOMC nerves” but quickly jumped back above $91,000.

If the Fed delivers the expected 0.25% cut, it could bolster crypto by improving liquidity conditions and risk appetite. Easing financial conditions have been core to the recent crypto rebound. Any dovish signals may prompt a relief rally in BTC and the broader crypto market.

However, a hawkish surprise – if the Fed were to hold rates steady or sound cautious – risks upsetting this fragile optimism. As reported on NewsBTC, a special focus will be on whether the Fed announces a new program for Treasury bill purchases.

#2 Solana’s Breakpoint (Dec. 11–13)

Solana’s Breakpoint conference kicks off Dec. 11 in Abu Dhabi, and traders are eyeing SOL’s price action around this flagship event. Breakpoint has a track record of stirring excitement – and volatility – in SOL. At the 2023 conference in Amsterdam, for example, SOL surged over 20% to a 14-month high (~$45) as a “flurry of announcements” (like Jump Crypto’s Firedancer client and Google Cloud integrations) dropped during the event.

This year, investors are anticipating major updates once again. The full launch of Firedancer (a high-performance Solana validator) and new ecosystem partnerships are rumored, and Breakpoint acts on investors like a magnet, usually triggering strong FOMO ahead of anticipated news.

If Solana’s team delivers headline-worthy developments, SOL could rally, as happened last year when announcements at Breakpoint corresponded with a price spike. Conversely, if the conference hype fades without new catalysts, short-term traders might take profit. Still, sentiment is clearly bullish going in.

#3 Do Kwon Sentencing (Dec. 11)

The long-awaited sentencing of Terraform Labs co-founder Do Kwon on Dec. 11 could mark a climactic chapter in the Terra/Luna saga. Kwon’s legal fate is largely sealed after he pleaded guilty to fraud in August, but the severity of punishment matters for the market psyche.

US prosecutors have asked for the maximum 12-year prison term for Kwon’s role in the $40 billion Terra meltdown. Paradoxically, traders have taken this bad news as bullish fuel: when the DOJ’s 12-year recommendation hit headlines, LUNC spiked 130% in a day, suggesting speculators see a tough sentence as a form of closure.

The actual sentencing on Dec. 11 could thus be a “sell the news” moment if those gains are purely hype-driven. Any outcome within expectations may prompt profit-taking after the event.

#4 Bittensor’s First TAO Halving (Dec. 12)

Bittensor (TAO), an AI-focused blockchain network, will undergo its inaugural token halving around Dec. 12–14, a pivotal event that echoes Bitcoin’s quadrennial cycle. After this “maturation milestone”, TAO’s issuance rate will be cut from 7,200 tokens per day to 3,600.

The halving cements Bittensor’s hard cap of 21 million TAO (just like BTC’s 21M) and is seen as a key milestone in the network’s maturation”. In the community, bulls have been hyping the “halving = scarcity” narrative for months – daily supply dropping 50% overnight is expected to “fuel scarcity narratives” and amplify TAO’s appeal as the base asset of a decentralized AI economy.

#5 Avalanche Spot ETF Decision

Avalanche (AVAX) could make history this week, as the US SEC faces a Dec. 12 deadline to approve or reject VanEck’s spot Avalanche ETF. This is the final decision date after multiple delays. Approval would mark one of the first mainstream investment vehicles for a “Ethereum-killer” layer-1 token, potentially unlocking new capital for AVAX.

Regulatory watchers are optimistic – Bloomberg ETF analysts Eric Balchunas and James Seyffart put the odds around 90% for approval. They argue that a spot AVAX fund would likely follow the path of recent Bitcoin and Ether ETFs.

#6 Aster’s S4 Buyback Program (Dec. 10)

Aster (ASTER), a DeFi protocol on BNB Chain, is commencing its Season 4 (S4) token buyback program on Dec. 10. Under this program, Aster will allocate 60–90% of all fees collected in Season 4 to buying back ASTER tokens from the open market.

This aggressive buyback scheme is designed to reduce supply and support the token’s price. In fact, the team announced it is accelerating the Phase 4 buybacks, with execution ramped up to roughly $4 million worth of ASTER purchases per day as of Dec. 8. Aster’s developers stated that this acceleration allows them to quickly deploy the fees accumulated since Nov. 10 onto the blockchain to prop up the market “during periods of volatility.”

By their estimates, it will take 8–10 days of these heightened buybacks to catch up, after which daily buybacks will continue at a steady 60–90% of the prior day’s fee revenue for the remainder of Season 4. A dedicated on-chain wallet for the buybacks is to be made public, ensuring transparency as the protocol executes what is essentially a large-scale, programmatic share (token) repurchase.

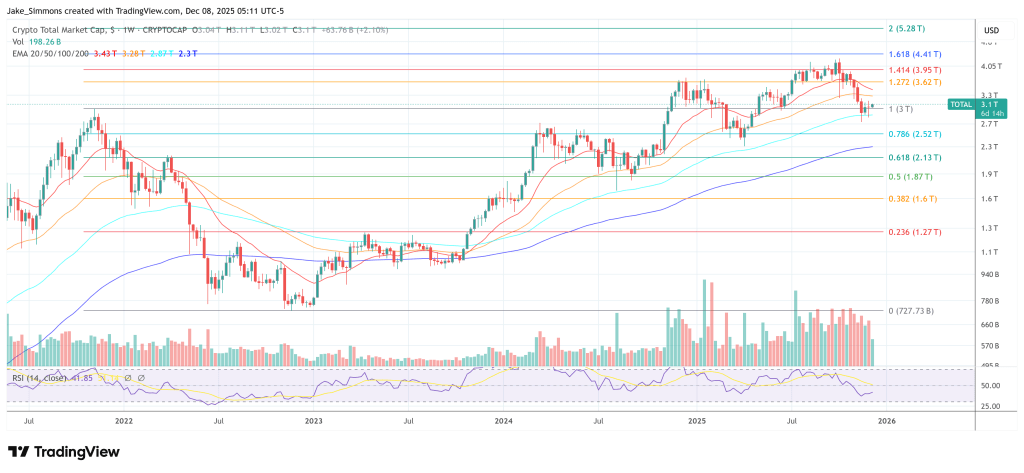

At press time, the total crypto market cap stood at $3.09 trillion.

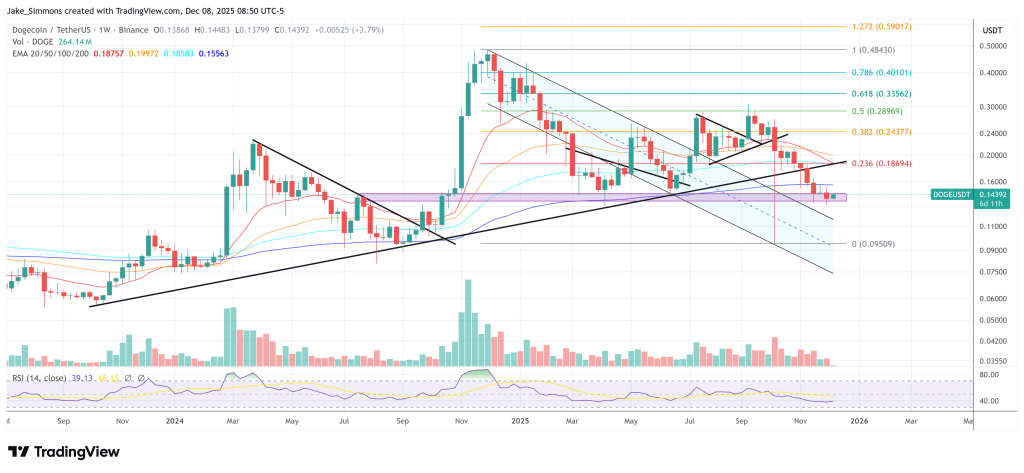

Dogecoin is trading directly on top of a long-term support band defined by its monthly Ichimoku cloud, according to a chart shared by crypto analyst Cantonese Cat (@cantonmeow) via X. The analyst summed it up by saying DOGE is “licking the bottom of its monthly Ichimoku cloud.”

Dogecoin Hovers At Key Monthly Ichimoku Support

The 1-month DOGE/USDT chart on Binance, captured on 7 December 2025, shows Dogecoin at around $0.14050, down about 3.8% for the month so far. The monthly candle opened at $0.14599, reached a high of $0.15340 and a low of $0.13177, underlining relatively tight but clearly downward monthly price action.

On the chart, the Ichimoku indicator uses standard 9-26-52-26 settings. The fast conversion line (Tenkan-sen) currently sits near $0.20092, and the base line (Kijun-sen) around $0.27491. The leading spans that form the cloud are plotted near $0.23792 and $0.26674, producing a forward-projected red Kumo that extends well into 2026.

With DOGE at roughly $0.14, price is trading far below both Tenkan and Kijun and is positioned just at the lower boundary of the projected cloud.

That lower cloud edge, which bends into the low-$0.12 to mid-$0.13 area before flattening, is the zone highlighted by Cantonese Cat. The October monthly candle shows a long lower wick that briefly pierced deep below, toward the mid-$0.06 region, but closed back above the cloud floor. The current, still-forming candle again tests just under that boundary and is, at the time of the snapshot, holding marginally above it around $0.14.

For Ichimoku practitioners, the lower Kumo boundary is often treated as the final structural support in a still-constructive higher-timeframe trend. In this case, the implication of the chart is clear: as long as monthly closes remain above roughly $0.12–$0.14, the multi-year structure can still be interpreted as a long-term bottoming zone rather than a completed breakdown.

In other words, for this analyst, Dogecoin’s prospective bottom hinges on whether that monthly Ichimoku support band in the $0.12–$0.14 range continues to hold.

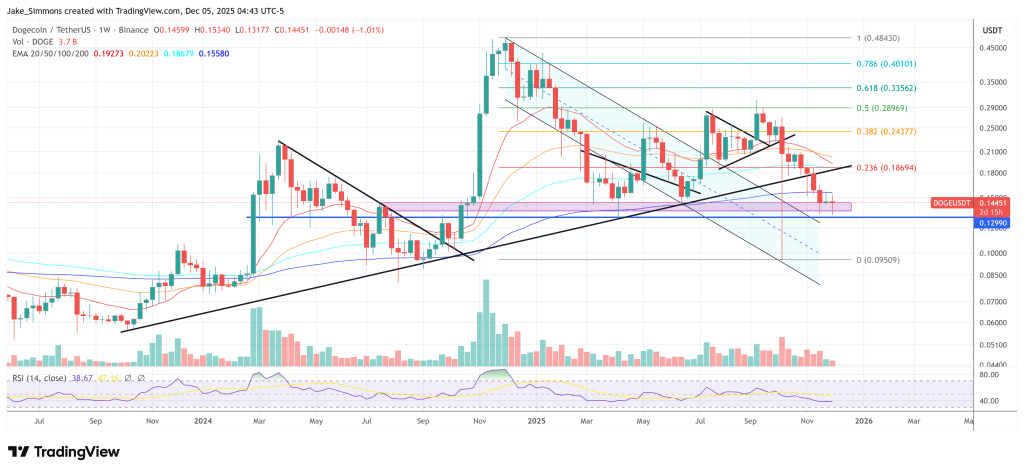

DOGE Sits Inside Key Support Zone In The Weekly Chart

On the weekly DOGE/USDT chart, price is sitting directly in the highlighted red support zone around $0.135–$0.145. This band coincides with a prior multi-week consolidation area and a former horizontal resistance level that capped price before the last major breakout.

Over the past several candles, weekly closes have clustered inside this zone while wicks repeatedly probe through it, underlining how aggressively the market is testing this level. The current candle trades near $0.14392, keeping Dogecoin inside the upper half of the support block but still below the 20-, 50-, 100- and 200-week EMAs, with the 200-week EMA at $0.15563 now just overhead.

At the same time, DOGE has clearly lost the rising black trendline that had connected higher lows from the left side of the chart. After breaking beneath this trend support, the DOGE price dropped sharply. The intersection of the broken trendline and the nearby moving averages now forms an overhead supply region, meaning price is compressing between these levels and the red horizontal support zone.

Crypto markets head into this week’s Federal Reserve meeting focused less on rate cut and more on whether Jerome Powell quietly declares the start of quantitative easing (QE). The key question on Wednesday for macro-sensitive traders is whether the Fed shifts into a bill-heavy “reserve management” regime that starts rebuilding dollar liquidity, even if it refuses to call it QE.

Futures markets suggest the rate decision itself is largely a foregone conclusion. According to the CME FedWatch Tool, traders are assigning roughly 87.2% odds to a 0.25 percentage point cut, underscoring that the real uncertainty is not about the size of the move, but about what the Fed signals on reserves, T-bill purchases and the future path of its balance sheet.

Former New York Fed repo specialist and current Bank of America strategist Mark Cabana has become the focal point of that debate. His latest client note argues that Powell is poised to announce a program of roughly 45 billion dollars in monthly Treasury bill purchases. For Cabana, the rate move is secondary; the balance-sheet pivot is the real event.

Cabana’s argument is rooted in the Fed’s own “ample reserves” framework. After years of QT, he contends that bank reserves are skirting the bottom of the comfortable range. Bill purchases would be presented as technical “reserve management” to keep funding markets orderly and repo rates anchored, but in practice they would mark a turn from draining to refilling the system. That is why many in crypto describe the prospective move as “stealth QE,” even though the Fed would frame it as plumbing.

What This Means For The Crypto Market

James E. Thorne, Chief Market Strategist at Wellington Altus, sharpened the point in X post. “Will Powell surprise on Wednesday?” he asked, before posing the question that has been echoing across macro desks: “Is Powell about to admit on Wednesday that the Fed has drained the system too far and now has to start refilling the bathtub?” Thorne argues that this FOMC “is not just about another token rate cut; it is about whether Powell is forced to roll out a standing schedule of bill-heavy ‘reserve management’ operations precisely because the Fed has yanked too much liquidity out of the plumbing.”

Thorne ties that directly to New York Fed commentary on funding markets and reserve adequacy. In his reading, “By Powell’s own framework, QT is done, reserves are skirting the bottom of the ‘ample’ range bordering on being too tight, and any new bill buying will be dressed up as a technical tweak rather than a confession of error, even though it will plainly rebuild reserves and patch the funding stress that the Fed’s own over-tightening has triggered.” That framing goes to the heart of what crypto traders care about: the direction of net liquidity rather than the official label.

Macro analysts followed closely by digital-asset investors are already mapping the next phase. Milk Road Macro on X has argued that QE returns in 2026, potentially as early as the first quarter, but in a much weaker form than the crisis-era programs.

They point to expectations of roughly 20 billion dollars a month in balance-sheet growth, “tiny compared to the 800bn per month in 2020,” and stress that the Fed “will be buying treasury bills, not treasury coupons.” Their distinction is blunt: “Buying treasury coupons = real QE. Buying treasury bills = slow QE.” The takeaway, in their words, is that “the overall direct effect on risk asset markets from this QE will be minimal.”

That distinction explains the tension now gripping crypto markets. A bill-only, slow-paced program aimed at stabilizing short-term funding is very different from the broad-based coupon buying that previously compressed long-term yields and turbo-charged the hunt for yield across risk assets. Yet even a modest, technically framed program would mark a clear return to balance-sheet expansion.

For Bitcoin and the broader crypto market, the immediate impact will depend less on Wednesday’s basis-point move and more on Powell’s language around reserves, Treasury bill purchases and future “reserve management” operations. If the Fed signals that QE is effectively starting and the bathtub is starting to be refilled, the liquidity backdrop that crypto trades against in 2026 may already be taking shape this week.

At press time, the total crypto market cap was at $3.1 trillion.

Michael A. Gayed, portfolio manager at Toroso Investments and publisher of macro research service The Lead-Lag Report, has put the XRP community on alert after a series of posts teasing a major related initiative.

Gayed Teases Yen-XRP Strategy

Gayed, a CFA charterholder known for his bearish, risk-focused market commentary, first flagged the cryptocurrency on December 4, posting: “Might do something related to XRP.” A day later he tied that tease directly to his broader macro outlook, writing: “You know how I always say we’re fucked? It’s time to find a way to profit from it. Might involve the Yen. And XRP.”

On December 6, he indicated that his interest in the token would not be a one-off remark, stating: “Going to do a long form post on XRP shortly.” In a separate message the same day he warned followers, “Might get annoying as fuck about XRP,” and urged them: “Put your notifications on for my account.”

The tone shifted further on December 7 from exploration to concrete signaling. Responding to speculation that he was chasing social metrics, Gayed insisted: “It’s not engagement farming. I’m working on something big. Big hint will be revealed this Thursday.” Without specifying whether he is referring to research, a trading strategy, or a product, he made clear that the token will be central to whatever he is preparing.

In a final note to close out that sequence, Gayed addressed the community directly: “Goodnight XRP army. I wrote this song. It’s yours now.” The song, shared with his followers, has since been circulated by prominent accounts, cementing his outreach to one of crypto’s most vocal retail bases.

What makes this notable is not just the content of the posts, but who is posting them. Gayed operates at the intersection of traditional asset management, ETF work and cross-asset macro research. His Lead-Lag framework is built around intermarket signals and risk regimes, and he has repeatedly warned of underpriced systemic risk in global markets.

Against that backdrop, the line “Might involve the Yen. And XRP” suggests he is working on a structured macro thesis that somehow connects currency dislocations, his negative outlook and the token. However, he has not yet disclosed any specific trade structure, allocation decision or product plan.

As of now, the verifiable facts are limited: Gayed has promised a long-form analysis, has stated he is “working on something big,” has explicitly rejected the idea that this is “engagement farming,” and has linked the token and the yen to his long-standing message that markets are in a precarious state. The exact nature, timing and market impact of his planned initiative remain unknown.

Until he publishes the promised long-form piece or a formal announcement, holders and broader market participants only know one thing for sure: a high-profile macro and ETF strategist has decided to make XRP a central theme of his upcoming work—and he wants everyone watching when he does.

EMJ Capital CEO Eric Jackson has laid out one of the most aggressive long-term bitcoin targets in the space yet, arguing in an interview with reporter Phil Rosen that the cryptocurrency could reach $50 million per coin by 2041. His projection is tied to a thesis that bitcoin will evolve from “digital gold” into the core collateral layer of the global financial system.

Jackson said his thinking grows out of the same “hundred bagger” framework he used when buying beaten-down equities like Carvana. He recalled entering Carvana after its share price collapsed from around $400 to roughly $3.50 in 2022, at a time when sentiment was almost universally hostile. “You would hear things like, that’s run by a bunch of criminals. This is what a bunch of idiots. Like you’d have to be an idiot to let your company go from $400 this year to $450 or $350 rather,” he told Rosen.

For Jackson, that period illustrated how markets behave at extremes. “It’s human nature almost that when you’re in the moment of max pain or pessimism, you can only see what’s right in front of you,” he said. Yet the underlying product remained strong: “It wasn’t a broken platform. It wasn’t a broken service […] they would tell you they loved it. It was so easy. It was the best customer experience they had.” From there, he could “envision how they were going to be like a much more profitable business” once the company focused on profitability and addressed its debt.

Jackson’s Long-Term Thesis For Bitcoin

He applies the same long-horizon lens to bitcoin, arguing that the day-to-day ticker and polarized narratives obscure its structural potential. “We get so tied to turning on the TV and just seeing, like, what’s the price of Bitcoin today […] Some people are bearish and they say, oh, it’s a Ponzi scheme. And some people are bullish and they just, you know, throw these like kind of pie in the sky targets that you can’t really tie to reality,” Jackson said. “It’s kind of hard to latch on to like, what is the value of this thing?”

Jackson begins with the common “digital gold” framing. He asks how large the gold market is, how many central banks and sovereigns hold it and why. “Could Bitcoin be as big as gold one day? That seems like a safe assumption,” he argued, adding that because it is “digital” and “programmable” rather than a “hunk of rock,” younger generations may prefer it as a store of value. But he stresses that this is only part of the story, as bitcoin has not become a medium for daily transactions “since the guy who bought pizza with Bitcoin back in like 2011.”

The “penny dropped,” he said, when he began to think in terms of what he calls the “global collateral layer” that underpins borrowing by sovereigns and central banks. Historically, that base layer moved from gold to the Eurodollar system from the 1960s onward, and today is heavily intertwined with sovereign debt. “All the countries around the world issue debt and then they kind of borrow against that and they do their daily like government transactions,” he noted, but “there are problems with that.”

In Jackson’s “Vision 2041,” bitcoin replaces the Eurodollar and, functionally, becomes the neutral asset that other balance sheets are built upon. He argues that bitcoin is “much superior” as collateral because it is digital and “apolitical,” sitting outside central banks and the influence of “whoever the latest treasury secretary here is in the US.”

As with the Eurodollar, he does not see this as a direct attack on the dollar or Treasuries, but as a new underlying layer: “There’s some underlying thing that a lot of other countries and the financial systems borrow against to kind of do things.”

Eric Jackson (@ericjackson) expects bitcoin to hit $50 million by 2041.

Looking ahead 15 years, Jackson envisions sovereigns that currently issue and roll debt instead “rely on Bitcoin,” because “over time, like that’s much more logical.” Given the “enormous” scale of the sovereign debt world, he argues that if bitcoin becomes the dominant collateral substrate, its price per coin would need to reach orders of magnitude above current levels—hence his $50 million-by-2041 target.

A new a16z crypto research paper argues that apocalyptic narratives about quantum computers instantly killing Bitcoin are badly misaligned with reality, and that the real risk for blockchains lies in long, messy migrations rather than a sudden “Q-Day” collapse. The piece has already triggered a sharp rebuttal on X from investors who say the threat is closer and harder than a16z suggests.

Bitcoin Isn’t Doomed By Quantum Computing: a16z

In the article “Quantum computing and blockchains: Matching urgency to actual threats,” a16z research partner and Georgetown computer science professor Justin Thaler sets the tone early, writing that “Timelines to a cryptographically relevant quantum computer are frequently overstated — leading to calls for urgent, wholesale transitions to post-quantum cryptography.” He argues that this hype distorts cost–benefit analyses and distracts teams from more immediate risks such as implementation bugs.

Thaler defines a “cryptographically relevant quantum computer” (CRQC) as a fully error-corrected machine capable of running Shor’s algorithm at a scale where it can break RSA-2048 or elliptic-curve schemes like secp256k1 in roughly a month of runtime. In his assessment, a CRQC in the 2020s is “highly unlikely,” and public milestones do not justify claims that such a system is probable before 2030.

He stresses that across trapped-ion, superconducting and neutral-atom platforms, no device is close to the hundreds of thousands to millions of physical qubits, with the required error rates and circuit depth, that would be needed for cryptanalysis.

Instead, the a16z piece draws a sharp line between encryption and signatures. Thaler argues that harvest-now-decrypt-later (HNDL) attacks already make post-quantum encryption urgent for data that must remain confidential for decades, which is why large providers are rolling out hybrid post-quantum key establishment in TLS and messaging.

But he insists that signatures, including those securing Bitcoin and Ethereum, face a different calculus: they do not protect hidden data that can be retroactively decrypted, and once a CRQC exists, the attacker can only forge signatures going forward.

On that basis, the paper claims that “most non-privacy chains” are not exposed to HNDL-style quantum risk at the protocol level, because their ledgers are already public; the relevant attack is forging signatures to steal funds, not decrypting on-chain data.

Bitcoin-Specific Headaches

Thaler still flags Bitcoin as having “special headaches” due to slow governance, limited throughput and large pools of exposed, potentially abandoned coins whose public keys are already on-chain, but he frames the time window for a serious attack in terms of at least a decade, not a few years.

“Bitcoin changes slowly. Any contentious issues could trigger a damaging hard fork if the community cannot agree on the appropriate solution,” Thaler writes, adding “another concern is that Bitcoin’s switch to post-quantum signatures cannot be a passive migration: Owners must actively migrate their coins.”

Moreover, Thalen flags a “final issue specific to Bitcoin” which is its low transaction throughput. “Even once migration plans are finalized, migrating all quantum-vulnerable funds to post-quantum-secure addresses would take months at Bitcoin’s current transaction rate,” Thaler says.

He is equally skeptical of rushing into post-quantum signature schemes at the base-layer. Hash-based signatures are conservative but extremely large, often several kilobytes, while lattice-based schemes such as NIST’s ML-DSA and Falcon are compact but complex and have already produced multiple side-channel and fault-injection vulnerabilities in real-world implementations. Thaler warns that blockchains risk weakening their security if they jump too early into immature post-quantum primitives under headline pressure.

Industry Split On The Risk

The most forceful pushback has come from Castle Island Ventures co-founder Nic Carter and Project 11 CEO Alex Pruden. Carter summed up his view on X by saying the a16z work “wildly underestimates the nature of the threat and overestimates the time we have to prepare,” pointing followers to a long thread from Pruden.

Pruden begins by stressing respect for Thaler and the a16z team, but adds, “I disagree with the argument that quantum computing is not an urgent problem for blockchains. The threat is closer, the progress faster, and the fix harder than how he’s framing it & than most people realize.”

He argues that recent technical results, not marketing, should anchor the discussion. Citing neutral-atom systems that now support more than 6,000 physical qubits, Pruden points out that “we now have a non annealing system with more than 6000 physical qubits in the neutral atom architecture,” directly contradicting any implication that only non-scalable annealing architectures have reached that scale. He notes that work such as Caltech’s 6,100-qubit tweezer array shows large, coherent, room-temperature neutral-atom platforms are already a reality.

On error correction, Pruden writes that “surface code error correction was experimentally demonstrated last year, moving it from a research problem into an engineering problem,” and points to rapid advances in color codes and LDPC codes.

He highlights Google’s updated “Tracking the Cost of Quantum Factoring” estimates, which show that a quantum computer with about one million noisy physical qubits running for roughly a week could, in principle, break RSA-2048 — a twenty-fold reduction from Google’s own 2019 estimate of twenty million qubits.

“Resource estimates for a CRQC running Shor’s algorithm have dropped by two orders of magnitude in six months,” he notes, concluding, “To say that this trajectory of progress might potentially deliver a quantum computer before 2030 is not an overstatement.”

Where Thaler emphasizes HNDL as an encryption problem, Pruden reframes blockchains as uniquely attractive quantum targets. He stresses that “public keys used in digital signatures are just as easy to harvest as encrypted messages,” but in blockchains those keys are directly tied to visible value. He points out that “these public keys are distributed & directly associated with value ($150B for Satoshi’s BTC alone),” and that once a quantum adversary can forge signatures, “If you can forge a signature, you can steal the asset regardless of when that original UTXO/account was created.”

For Pruden, this economic reality means “the economic incentives simply and clearly point to blockchains as being the first cryptographically relevant quantum use case,” even if other sectors also face HNDL risks. He adds that “blockchains will be far slower to migrate than centralized systems. A bank can upgrade its stack. Blockchains must reach global consensus, absorb performance trade-offs from PQ signatures, and coordinate millions of users to migrate their keys.”

Invoking Ethereum’s multi-year shift from proof of work to proof of stake, he writes, “The closest thing was the ETH 1.0 to 2.0 transition which took years, and as complex as that was, a PQ migration is much harder. Anyone who thinks this is a matter of swapping a few lines of signature code has simply never shipped, deployed, or maintained a production blockchain.”

Pruden agrees with Thaler that panic is dangerous, but flips the conclusion: “I agree that rushing is dangerous. But that is exactly why work must begin now. The most likely failure mode is that the industry waits too long, and then a major QC milestone triggers a panic.” He closes by saying he disagrees that “quantum computing is progressing slowly,” that “blockchains are less vulnerable than systems exposed to HNDL risk,” or that “the industry has years of slack before action is needed,” arguing that “All three assumptions are at odds with reality.”

Tom Lee has reiterated one of the most aggressive Ethereum targets in the market, telling attendees at Binance Blockchain Week on 4 December that ETH could eventually trade at $62,000 as it becomes the core infrastructure for tokenized finance.

“Okay, so let me explain to you why Ethereum, now that we’ve talked about crypto, […] is the future of finance,” Lee said on stage. He framed 2025 as Ethereum’s “1971 moment,” drawing a direct analogy to when the US dollar left the gold standard and triggered a wave of financial innovation.

Lee’s Thesis For Ethereum

“In 1971, the dollar went off the gold standard. And in 1971, it galvanized Wall Street to create financial products to make sure the dollar would be the reserve currency,” Lee argued. “Well, in 2025, we’re tokenizing everything. So it’s not just the dollar that’s getting tokenized, but it’s stocks, bonds, real estate.”

In his view, this shift positions ETH as the primary settlement and execution layer for tokenized assets. “Wall Street is, again, going to take advantage of that and create products onto a smart contract platform. And where they’re building this is on Ethereum,” he said. Lee pointed to current real-world asset experiments as early evidence, noting that “the majority of this, the vast majority, is being built on Ethereum,” and adding that “Ethereum has won the smart contract war.”

Lee also stressed that ETH’s market behavior has not yet reflected that structural role. “As you know, ETH has been range bound for five years, as I’ve shaded here. But it’s begun to break out,” he told the audience, explaining why he “got very involved with Ethereum by turning Bitmine into an ETH treasury company, because we saw this breakout coming.”

The core of his valuation case is expressed through the ETH/BTC ratio. Lee expects Bitcoin to move sharply higher in the near term: “I think Bitcoin is going to get to $250,000 within a few months.” From there, he derives two key ETH scenarios.

First, if the ETH/BTC price relationship simply reverts to its historical mean, he sees substantial upside. “If ETH price ratio to Bitcoin gets back to its eight year average, that’s $12,000 for Ethereum,” he said. Second, in a more aggressive case where ETH appreciates to a quarter of Bitcoin’s price, his long-standing $62,000 target emerges: “If it gets to 0.25 relative to Bitcoin, that’s $62,000.”

“I think Ethereum’s going to become the future of finance, the payment rails of the future and if it gets to .25 relative to Bitcoin that’s $62,000. Ethereum at $3,000 is grossly undervalued.” pic.twitter.com/VydvLou9IE

Lee links these ratios directly to the tokenization narrative. “If 2026 is about tokenization, that means Ether’s utility value should be rising. Therefore, you should watch this ratio,” he told the crowd, arguing that valuation should track growing demand for ETH blockspace and its role as “the payment rails of the future.”

He concluded with a pointed assessment of current levels: “I think Ethereum at $3,000, of course, is grossly undervalued.”

Crypto analyst Miles Deutscher has issued one of the most forceful bottom calls of this cycle, assigning a 91.5% probability that Bitcoin’s low is already in. In a X thread on December 4, he wrote: “F*ck it. I’m putting my neck on the line here. I’m 91.5% certain that the BTC bottom is in. And if it is, A LOT of people are about to be caught offside.”

Is The Bitcoin Bottom In?

Deutscher bases his conviction on four “pillars”: market reaction to news, the historical behaviour of FUD events, a shift in flows, and an improving global liquidity backdrop. Each pillar is scored in an internal model that culminates in a 91.5/100 bullish reading.

He starts with price behaviour versus headlines. Over recent days, he notes, the market has digested an “influx of bad news” – including renewed Tether FUD, another round of “China banning crypto,” MicroStrategy scrutiny and concerns around a Bank of Japan–driven yen carry trade unwind.

“Despite all this bad news, price rallied,” he writes, calling this “the first time since the major selloff began” that Bitcoin has responded positively to a destructive news cycle. He underscores an old trading adage: “The reaction to news is more important than the news itself. This tells you everything you need to know.”

The second pillar is a systematic look at whether such FUD clusters tend to coincide with local lows. Deutscher says he backtested “every single time Tether, China, BOJ, and Microstrategy FUD entered the market” in a similar way. His conclusion is stark: “Every single time, these FUD events marked a local bottom. Tether FUD = bottom.

China ‘banning’ crypto = bottom. Bank of Japan/carry trade concerns = bottom. Microstrategy FUD = bottom.”

On this basis, his AI model assigns the maximum score of 28/28 to this pillar. He cautions that “in isolation, this factor doesn’t matter much,” but argues that, combined with the first pillar, it “starts to paint a convincing bull case.”

The third pillar is flows, which he calls “the most critical factor (net buy/sell pressure).” For the past weeks, flows were “aggressively negative” with OG whales selling and ETFs dumping. Recently, he argues, this picture has changed. ETF inflows are “starting to stabilise & uptick,” treasury-company holdings remain stable, and “OG whales have stopped relentlessly dumping (this is clear on the orderbooks).” This earns a 22.5/25 score in his model. He adds one key caveat: as long as DATs exist, “there are material risks.”

The fourth pillar is the liquidity and macro environment. Deutscher notes that market liquidity had been tightening for months, but now “things are shifting back toward increased market liquidity,” with global financial conditions “reloosened to near highs.” He highlights “macro tailwinds” and adds that a new, potentially more dovish Fed chair is coming and “QT has now officially ended.” This set of factors receives a 9/10 score in his framework.

Aggregating all four pillars leads to the headline figure: “With all four market pillars taken into account, we arrive at a final score of 91.5/100.”

Deutscher, however, explicitly lists caveats. He points out that US markets “have been on a massive run” and may need to cool off, that DATs “are still seeing some short-term pressure,” and that ETF flows “can flip negative at any time.” His conclusion is probabilistic rather than absolute: “Markets are a game of probabilities, and I think the odds are in favour of the bottom being in – given the extreme FUD we’ve had and the market’s reaction to it.”

Crypto research firm Delphi Digital argues that global dollar liquidity has quietly flipped from a structural headwind to a marginal tailwind for risk assets for the first time since early 2022 – with 2026 emerging as the key inflection point for digital assets.

In a macro thread on X, Delphi says “the Fed’s rate path heading into next year is the clearest it’s been in years.” Futures imply another 25-basis-point cut by December 2025, taking the federal funds rate to roughly 3.5–3.75%. “The forward curve prices at least 3 more cuts through 2026, putting us in the low 3s by year-end if the path holds,” the firm notes.

Short-term benchmarks have already adjusted. According to Delphi, “SOFR and fed funds have drifted toward the high 3% range. Real rates have rolled over from their 2023–2024 peaks. But nothing has collapsed. This is a controlled descent rather than a pivot.” The characterization is important: this is not a return to zero rates, but a gradual easing that removes pressure on duration and high-beta assets.

The more consequential shift is in the liquidity plumbing. “QT ends on December 1. The TGA is set to draw down rather than refill. The RRP has been fully depleted,” Delphi writes. “Together, these create the first net positive liquidity environment since early 2022.”

Crypto Bulls Can Rejoice As The Macro Regime Is Shifting

In a follow-up post, the firm is explicit: “The Fed’s liquidity buffer is gone. Reverse Repo Balances collapsed from over $2 trillion at the peak to practically zero.” In 2023, a swollen RRP allowed the Treasury to refill its General Account without directly draining bank reserves, because money-market funds could absorb issuance out of the RRP. “With the RRP now at the floor, that buffer no longer exists,” Delphi warns.

From here, “any future Treasury issuance or TGA rebuild has to come directly out of bank reserves.” That forces a policy choice. As Delphi puts it, “The Fed is left with two options: let reserves drift lower and risk another repo spike or expand the balance sheet to provide liquidity directly. Given how badly 2019 went, the second path is far more likely.”

In that scenario, the central bank would shift from shrinking its balance sheet to adding reserves, reversing a core dynamic of the past two years. “Combined with QT ending and the TGA set to draw down, marginal liquidity is turning net positive for the first time since early 2022,” Delphi concludes. “A key headwind for crypto could be fading.”

For the crypto market, the firm frames 2026 as the pivotal year: “2026 is the year policy stops being a headwind and becomes a mild tailwind. The kind that favors duration, large caps, gold, and digital assets with structural demand behind them.”

Rather than calling for an immediate price spike, Delphi’s thesis is that the macro regime is shifting toward a more supportive, liquidity-positive backdrop for Bitcoin and larger crypto assets as policy eases and the era of aggressive balance-sheet contraction comes to an end.

At press time, the total crypto market cap was at $3.1 trillion.

Bitwise Chief Investment Officer Matt Hougan is pushing back against one of the loudest bearish narratives around bitcoin treasury company Strategy (MSTR, formerly MicroStrategy): that it could be forced into a liquidation of its roughly $60 billion bitcoin stack. In his latest CIO memo, Hougan writes bluntly that “Michael Saylor and Strategy selling bitcoin is not one of” the real risks in crypto.

Will Strategy Sell Its Bitcoin?

The immediate trigger for market anxiety is MSCI’s consultation on whether to remove so-called digital asset treasury companies (DATs) like Strategy from its investable indexes. Nearly $17 trillion in assets tracks those benchmarks, and JPMorgan estimates index funds might have to sell up to $2.8 billion of MSTR if it is excluded.

MSCI’s rationale is structural: it views many DATs as closer to holding companies or funds than operating companies, and its investable universes already exclude holding structures such as REITs.

Hougan, a self-described “deep index geek” who previously spent a decade editing the Journal of Indexes, says he can “see this going either way.” Michael Saylor and others are arguing that Strategy remains very much an operating software company with “complex financial engineering around bitcoin,” and Hougan agrees that this is a reasonable characterization. But he notes that DATs are divisive, MSCI is currently leaning toward excluding them, and he “would guess there is at least a 75% chance Strategy gets booted” when MSCI announces its decision on January 15.

He argues, however, that even a removal is unlikely to be catastrophic for the stock. Large, mechanical index flows are often anticipated and “priced in well ahead of time.” Hougan points out that when MSTR was added to the Nasdaq-100 last December, funds tracking the index had to buy about $2.1 billion of stock, yet “its price barely moved.”

He believes some of the downside in MSTR since October 10 already reflects investors discounting a probable MSCI removal, and that “at this point, I don’t think you’ll see substantial swings either way.” Over the long term, he insists, “the value of MSTR is based on how well it executes its strategy, not on whether index funds are forced to own it.”

The more dramatic claim is the so-called MSTR “doom loop”: MSCI exclusion leads to heavy selling, the stock trades far below NAV, and Strategy is somehow forced to sell its bitcoin. Here Hougan is unequivocal: “The argument feels logical. Unfortunately for the bears, it’s just flat wrong. There is nothing about MSTR’s price dropping below NAV that will force it to sell.”

He breaks the problem down to actual balance sheet constraints. Strategy, he says, has two key obligations: about $800 million per year in interest payments and the need to refinance or redeem specific debt instruments as they mature.

Smaller DATs Are The Bigger Problem

On interest, the company currently has approximately $1.4 billion in cash, enough to “make its dividend payments easily for a year and a half” without touching its bitcoin or needing heroic capital markets access. On principal, the first major maturity does not arrive until February 2027, and that tranche is “only about $1 billion—chump change” compared with the roughly $60 billion in bitcoin the company holds.

Governance further reduces the likelihood of forced selling. Michael Saylor controls around 42% of Strategy’s voting shares and is, in Hougan’s words, a person with extraordinary “conviction on bitcoin’s long-term value.” He notes that Saylor “didn’t sell the last time MSTR stock traded at a discount, in 2022.”

Hougan concedes that a forced liquidation would be structurally significant for bitcoin, roughly equivalent to two years of spot ETF inflows dumped back into the market. He simply does not see a credible path from MSCI index mechanics and equity volatility to that outcome “with no debt due until 2027 and enough cash to cover interest payments for the foreseeable future.” At the time of writing, he notes, bitcoin trades around $92,000, about 27% below its highs but still 24% above Strategy’s average acquisition price of $74,436 per coin. “So much for the doom.”

Hougan ends by stressing that there are real issues to worry about in crypto—slow-moving market structure legislation, fragile and “poorly run” smaller DATs, and a likely slowdown in DAT bitcoin purchases in 2026. But on Strategy specifically, his conclusion is direct: he “wouldn’t worry about the impact of MSCI’s decision on the stock price” and sees “no plausible near-term mechanism that would force it to sell its bitcoin. It’s not going to happen.”

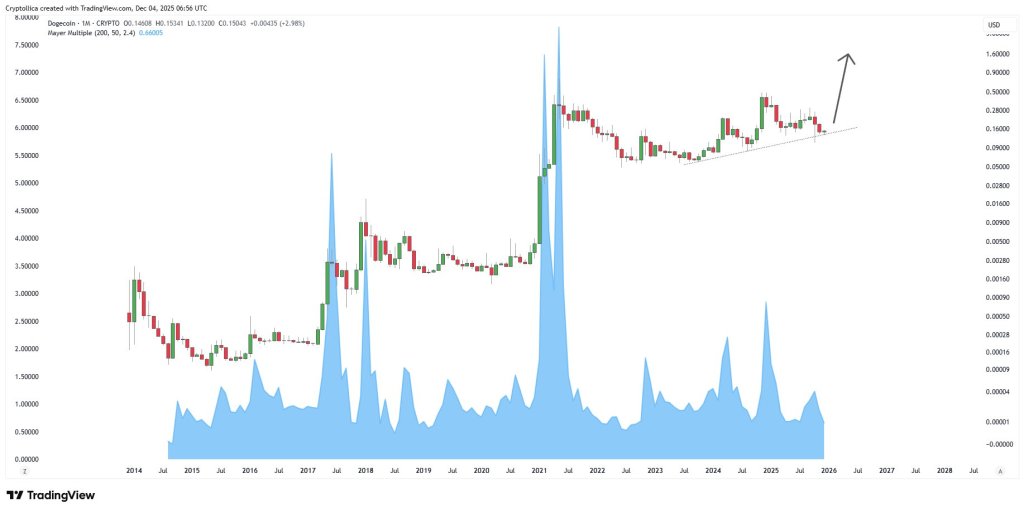

Dogecoin is hovering near $0.15, but a cluster of technical and on-chain indicators shared on X suggests the market structure is far healthier than during the last bear phase, prompting fresh upside calls from analysts.

Dogecoin Could Target $1.30

Trader Cryptollica posted a long-term monthly DOGE chart with the Mayer Multiple and a clear message: “DOGE Target > $1.30.” The Mayer Multiple, using 200- and 50-period moving averages with a 2.4 threshold, sits at 0.66005. Visually, that is far below the spikes above 5 that accompanied the 2017 and 2021 blow-off tops, indicating that Dogecoin is not yet in the overheated conditions historically associated with major market peaks.

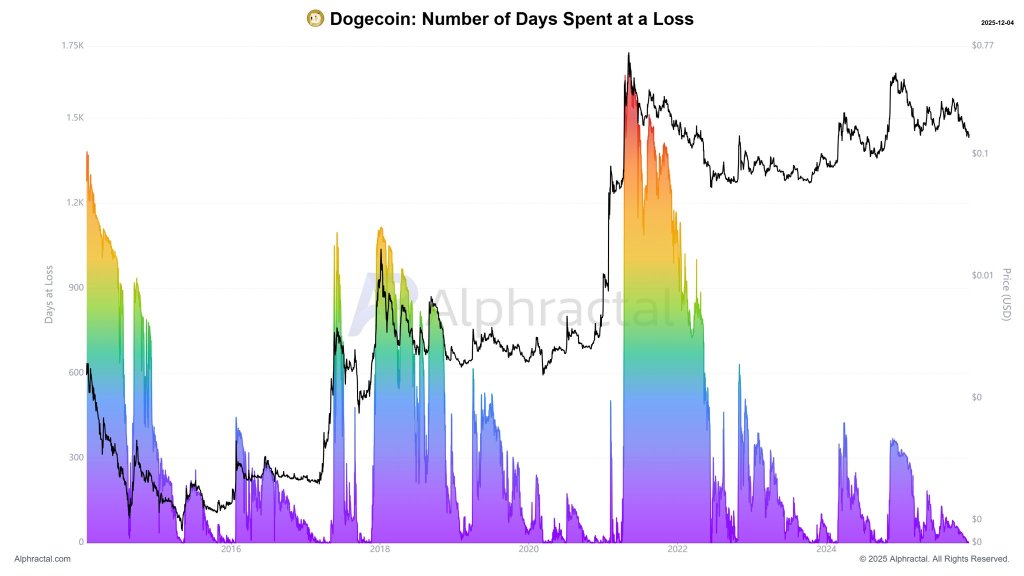

Cryptollica also highlighted an Alphractal chart titled “Dogecoin: Number of Days Spent at a Loss.” The series overlays DOGE’s price with a multicolour histogram of how long coins have been held in unrealised loss.

Earlier cycle lows around 2014–2015 and the post-2021 unwind show extended peaks above roughly 1,200–1,500 days at a loss. In the latest segment, that metric has compressed back toward the lower end of the scale, resembling the early reset phases that preceded previous advances, and signalling that the proportion of long-suffering holders has markedly declined.

DOGE On-Chain Data Looks Strong

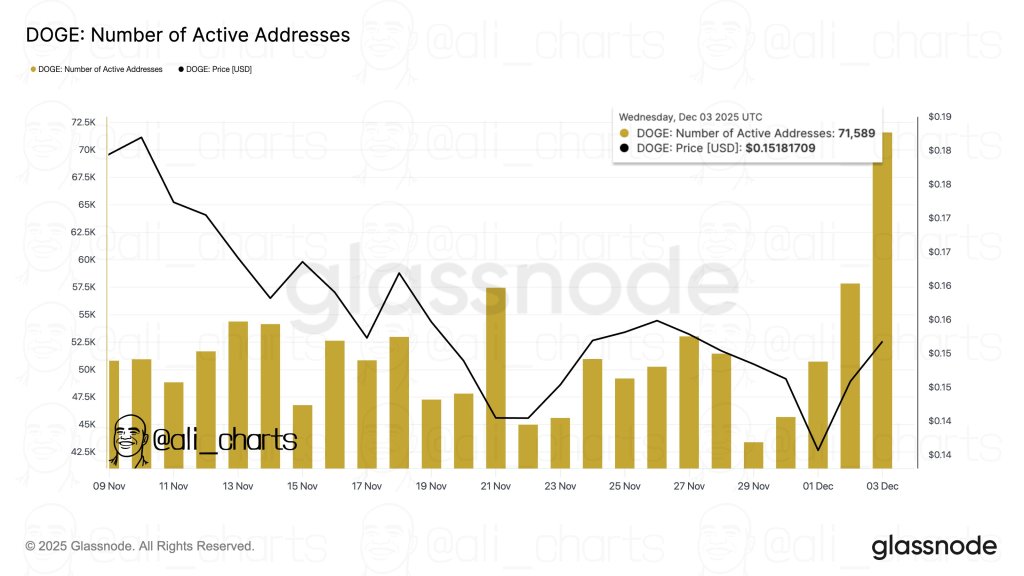

On the shorter-term on-chain side, Ali Martinez (@ali_charts) pointed to a sharp rebound in network activity. “Dogecoin just saw 71,589 active addresses. The biggest spike since September,” he wrote, sharing Glassnode data.

The chart “DOGE: Number of Active Addresses” plots daily active addresses as yellow bars against the DOGE price in black. From early November, activity ranged around 45,000–47,500 addresses while price drifted lower from about $0.17 to $0.14. On December 3, active addresses jumped to 71,589 as price recovered to $0.15181709, signalling a broadening of participation rather than a purely price-driven move.

Ali also drew attention to whale behaviour. Posting a Santiment chart of balances held by addresses with between 1,000,000 and 100,000,000 DOGE, he noted: “480 million Dogecoin bought by whales in 48 hours!”

The grey area representing holdings in this band trends down from around 35.6 billion DOGE in mid-October to below 28 billion by late November while price falls from above $0.18 to about $0.135, indicating sustained distribution. In the final days of the chart, holdings rose again to roughly 28.45 billion as price rebounded from $0.14 to $0.15, confirming a renewed net accumulation phase among large holders.

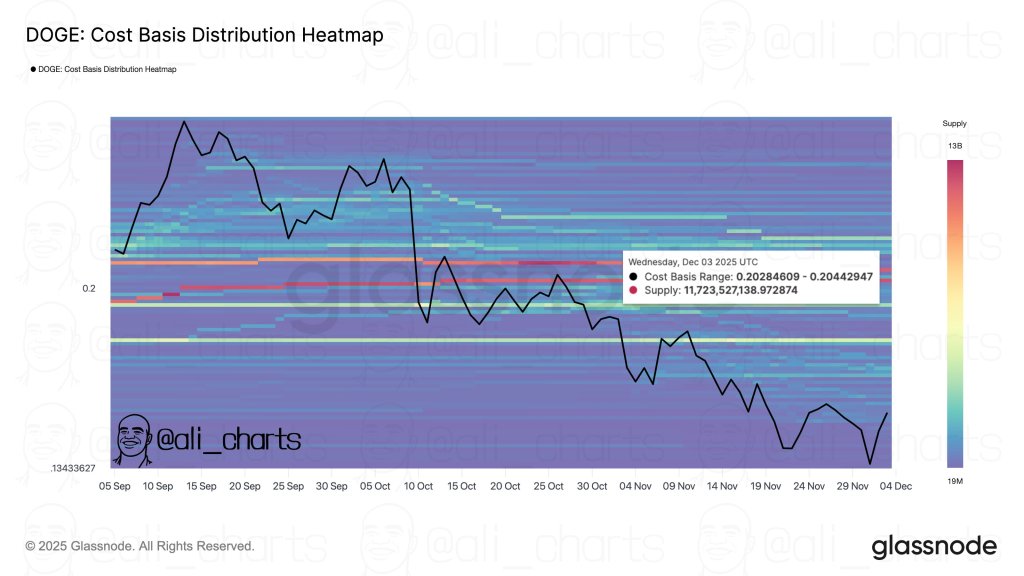

A third chart from Ali, “DOGE: Cost Basis Distribution Heatmap,” defines the next major technical hurdle. “$0.20 is the key resistance for Dogecoin. That’s where 11.72 billion $DOGE were accumulated,” he wrote.

The Glassnode heatmap highlights a dense band between $0.20284609 and $0.20442947, with an annotated supply of 11,723,527,138.97 DOGE whose on-chain cost basis lies in that range. This cluster marks a heavy realised-price node where a large volume of coins moves from loss to breakeven as spot revisits $0.20, creating a clearly defined resistance zone.

In combination, subdued valuation on the Mayer Multiple, a reset in “days at a loss,” the largest active-address spike since September, recent whale accumulation of 480 million DOGE and a well-defined $0.20 cost-basis wall form a favourable on-chain basis. Whether those higher levels are reached will depend on the market’s ability to absorb the 11.72 billion DOGE supply stacked around $0.20 and sustain the recent improvement in on-chain activity and large-holder demand.

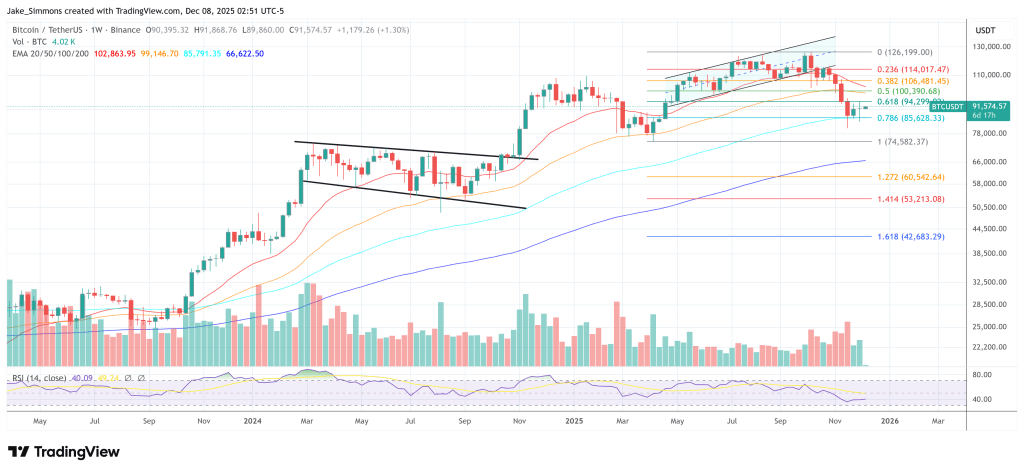

Bitcoin is again trading under the shadow of a potential yen carry-trade shock as markets head into the 9–10 December FOMC meeting and a likely hawkish turn from the Bank of Japan at the December 18-19 meeting. The setup echoes last summer’s episode, when a policy shift in Tokyo triggered rapid deleveraging across risk assets, including crypto.

Will The Bitcoin Price Crash Next Week?

Analyst Benjamin Cowen explicitly links today’s environment to that July shock. He reminded followers that “in July 2024, the Fed cut rates while the BOJ raised rates, leading to the unwind of the carry trade. Bitcoin capitulated into it, and found a low 1 week later.” He added, “Good chance this happens again on December 10th (Fed cuts, BOJ raises rates). So maybe Bitcoin finds a low mid-Dec?”

The precise sequencing last year was more nuanced – markets aggressively priced Fed easing while the BoJ surprised with a hike – but the core mechanism Cowen highlights is the same: when US policy is moving toward looser conditions just as Japan tightens, the long-running yen carry trade becomes unstable and high-beta assets sell off hard.

Truflation’s thread lays out why this matters for Bitcoin and the wider crypto market. Large institutions and commercial banks “borrow money in Yen where interest rates are historically and famously low, and use that money to invest in the US.” They can park the funds in interest-bearing instruments to “earn healthy 3–4%” on the spread, or “more often, they invest in stocks and bonds to get way more.” This is reinforced by a BoJ policy of keeping the yen cheap against the dollar.

The danger arises when stocks fall and the yen starts to rise or is expected to rise. Then “institutional and Commercial borrowers may exit, so as not to get stuck with significant losses on their Yen debts.” They “sell whatever assets they purchased in the US and get back into Yen to pay back their loans in Japan, resulting in a cascade of US asset sales and Yen purchases.” After “years of Yen carry trade being a relatively safe way for big banks and institutional investors to make easy money,” even a modest normalization can force broad, mechanical de-risking — and Bitcoin, as a liquid, leveraged risk asset, sits directly in that firing line.

Crypto trader Kevin (@Kev_Capital_TA) underscores how tight the current window is. He notes that “we have the Fed’s preferred measure to track inflation via the Core PCE inflation and then the FOMC all in the next six days,” followed by a BoJ press conference on 19 December that will be “massive for Dollar, short end and long end of the yield curve not to mention Yen carry trade fears.” In a separate post, he stresses that “the JP10Y continues to make new highs. Pretty big deal folks,” highlighting that Japanese yields are grinding higher into that meeting and increasing pressure on the BoJ to act.

A few days ago, BitMEX founder Arthur Hayes connected that macro repricing directly to Bitcoin’s latest leg down. “BTC dumped cause BOJ put Dec rate hike in play. USDJPY 155–160 makes BOJ hawkish,” he argues, framing the sell-off as a funding shock rather than a crypto-native event.

Into December, futures and economist surveys put the probability of a Fed cut at roughly 80–87% for the 9–10 December meeting, even as the committee remains divided. At the same time, the BoJ is openly signalling it will “consider the pros and cons” of a hike at its 18–19 December meeting, with markets now pricing a high likelihood of tightening and 10-year JGB yields near multi-decade highs.

That combination — Fed easing expectations plus BoJ tightening risk — is exactly the configuration that threatens the yen carry and makes a repeat of July 2024’s pattern plausible: a sharp flush in Bitcoin and other risk assets, followed by a bottom once forced deleveraging runs its course.

At Binance Blockchain Week on December 3, Ripple Labs CEO Brad Garlinghouse argued that a rare alignment of regulatory change, institutional demand and real-world utility is setting up crypto for what he called powerful “macro tailwinds” heading into 2026.