Billionaire Michael Saylor ignited fresh speculation this week after sharing a Bitcoin chart featuring a new set of mysterious green dots, prompting questions across the market about what they represent and whether they signal another wave of aggressive buying.

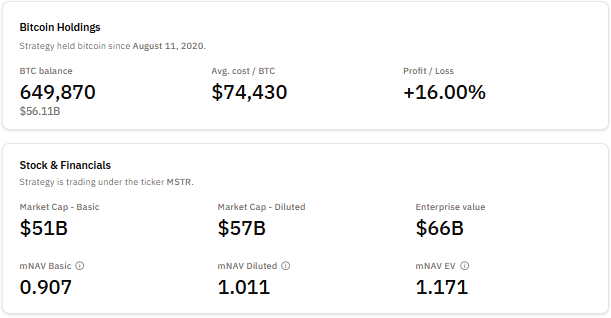

The chart, posted alongside new data on Strategy’s rapidly expanding Bitcoin position, showed a total of 87 purchase events, bringing the company’s holdings to 649,870 BTC worth about $59.45 billion at an average cost of $74,433 per coin.

The familiar orange dots reflected each individual accumulation since 2020, while the green dotted line captured immediate attention as traders debated its meaning.

Analysts later clarified that the green dotted line represents Strategy’s average purchase price, a rolling figure that updates only when new Bitcoin is acquired.

It reflects the company’s dynamic cost basis rather than Bitcoin’s price or any form of prediction.

With each new buy, the line shifts depending on whether Bitcoin was purchased above or below the previous average.

Because Strategy’s positions are large, some buying events have pushed the line sharply higher, especially between 2024 and 2025, when the firm accelerated accumulation during Bitcoin’s run toward the $100,000 region.

The chart confirmed that Strategy’s portfolio remains profitable, with the Bitcoin stack up 22.9% as of Nov. 30.

Bitcoin has been trading in the $95,000 to $110,000 range in late 2025, keeping the company comfortably above its $74,433 average cost.

Yet while the holdings show gains and the “green line” hints at more aggressive buying according to some analysts, Strategy’s stock has fallen more than 60% from recent highs, and this disconnect is feeding new questions about the long-term sustainability of Saylor’s strategy.

Strategy Signals It May Sell Bitcoin if Market Pressures Mount

In a development that marks a shift from years of strict “never sell” messaging, Strategy quietly acknowledged that Bitcoin sales are now possible under specific stress conditions.

CEO Phong Le said the company would consider selling some of its holdings only if two events occur at once: if Strategy’s market-to-net-asset-value ratio falls below one and if the company cannot raise new capital.

Le noted that he does not want to be the executive who sells Bitcoin but added that financial discipline must take priority in a hostile market.

He described a scenario where selling a portion of the treasury becomes mathematically justified to protect what he calls “Bitcoin yield per share,” especially if issuing new equity becomes more dilutive than liquidating a small fraction of BTC.

The company’s mNAV is currently 1.01, but this level has been unstable throughout 2025.

Earlier in the year, the ratio traded as high as 3.3, but by mid-November it slipped under 1.0 for the first time since Strategy began acquiring Bitcoin.

A drop below one means the market values the company at less than the worth of its Bitcoin holdings, undermining the premium that allows Strategy to raise capital cheaply.

Le warned that if the company cannot access cash while operating below that threshold, selling becomes an option of last resort.

Strategy’s $21B Fundraising Stands Firm as Bitcoin Drops 32% From All-Time High

The company secured $11.9 billion through common equity, $6.9 billion through preferred equity, and $2 billion via convertible debt across seven different securities.

Investor appetite remains strong, even as the firm faces roughly $800 million in annual dividend obligations tied to its preferred shares.

Le said the plan is to maintain these payments using capital raised at a premium, adding that consistent dividend performance helps strengthen market confidence.

Strategy also introduced a new “BTC Credit” dashboard last week to reassure investors amid volatile market action.

MSCI is considering a new rule that would remove companies from its Global Investable Market Indexes if 50% or more of their assets are held in digital assets such as Bitcoin. The proposal appears simple, but the implications are far-reaching. It would affect companies like Michael Saylor’s Strategy (formerly MicroStrategy), Eric and Donald Trump Jr’s American Bitcoin Corp (ABTC), and dozens of others across global markets whose business models are fully legitimate, fully regulated, and fully aligned with long-standing corporate treasury practices.

The purpose of this document is to explain what MSCI is proposing, why the concerns raised around Bitcoin treasury companies are overstated, and why excluding these firms would undermine benchmark neutrality, reduce representativeness, and introduce more instability—not less—into the indexing system.

1. What MSCI Is Proposing

MSCI launched a consultation to determine whether companies whose primary activity involves Bitcoin or other digital-asset treasury management should be excluded from its flagship equity indices if their digital-asset holdings exceed 50% of total assets. The proposed implementation date is February 2026.

The proposal would sweep in a broad set of companies:

Strategy (formerly MicroStrategy), a major software and business-intelligence firm that holds Bitcoin as a treasury reserve.

American Bitcoin Corp (ABTC), a new public company created by Eric and Donald Trump with a Bitcoin-focused balance sheet.

Miners, infrastructure firms, and diversified operating companies that use Bitcoin as a long-term inflation hedge or capital reserve.

These companies are all publicly traded operating entities with audited financials, real products, real customers, and established governance. None are “Bitcoin ETFs.” Their only distinction is a treasury strategy that includes a liquid, globally traded asset.

2. The JPMorgan Warning — And the Reality Behind It

JPMorgan analysts recently warned that Strategy could face up to $2.8B in passive outflows if MSCI removes it from its indices, and up to $8.8B if other index providers follow.

Their analysis correctly identifies the mechanical nature of passive flows. But it misses the real context.

Strategy has traded more than $1 trillion in volume this year. The “catastrophic” $2.8B scenario represents:

Less than one average trading day

~12% of a typical week

~3% of a typical month

0.26% of year-to-date trading flow

In liquidity terms, this is immaterial. The narrative of a liquidity crisis does not match market structure reality. The larger issue is not the outflow itself—it is the precedent that index exclusion would set.

If benchmark providers begin removing companies because of the composition of their treasury assets, the definition of what qualifies as an “eligible company” becomes non-neutral.

MSCI $MSTR DE-LISTING FEAR MONGERING: THE $2.8 BILLION LIE

First: Strategy is at ZERO risk of being delisted from other indices. Second: J.P. Morgan says an MSCI delisting would trigger a $2.8 Billion forced sell off. They are banking on you not knowing the math.

MSCI’s policy position also conflicts with the composition of MSCI’s own assets.

MSCI reports roughly $5.3B in total assets. More than 70%—about $3.7B—is goodwill and intangible assets. These are non-liquid, non-marketable accounting entries that cannot be sold or marked to market. They are not verifiable in the same way that digital assets are.

Bitcoin, by contrast:

Trades globally 24/7

Has transparent price discovery

Is fully auditable and mark-to-market

Is more liquid than nearly any corporate treasury asset outside sovereign cash

The proposal would penalize companies for holding an asset that is far more liquid, transparent, and objectively priced than the intangibles that dominate MSCI’s own balance sheet.

MSCI is a New York based, pubco ( $MSCI) with ~$5.3B in assets on its balance sheet.

70% ($3.7B) of MSCI's assets are classified as “intangible” (goodwill and other intangible assets).

At the same time, MSCI is proposing to exclude companies whose digital asset holdings… pic.twitter.com/dyVwRR2AhH

MSCI is a global standard-setter. Its benchmarks are used by trillions of dollars in capital allocation. These indices are governed by widely accepted principles—neutrality, representativeness, and stability. The proposed digital-asset threshold contradicts all three.

Neutrality

Benchmarks must avoid arbitrary discrimination among lawful business strategies. Companies are not removed for holding:

Large cash positions

Gold reserves

Foreign exchange reserves

Commodities

Real estate

Receivables that exceed 50% of assets

Digital assets are the only treasury asset singled out for exclusion. Bitcoin is legal, regulated, and widely held by institutions worldwide.

Representativeness

Indices are meant to reflect investable markets—not curate them.

Bitcoin treasury strategies are increasingly used by corporations of all sizes as a long-term capital-preservation tool. Removing these companies reduces the accuracy and completeness of MSCI’s indices, giving investors a distorted view of the corporate landscape.

Stability

The 50% threshold creates a binary cliff effect. Bitcoin routinely moves 10–20% in normal trading. A company could fall in and out of index eligibility multiple times a year simply due to price action, forcing:

Unnecessary turnover

Additional tracking error

Higher fund implementation costs

Index providers typically avoid rules that amplify volatility. This rule would introduce it.

5. The Market Impact of Exclusion

Forced Selling

If MSCI proceeds, passive index funds would need to sell holdings in affected companies. Yet the real-world impact is marginal because:

Strategy and ABTC are highly liquid

Flows represent a tiny fraction of normal trading volume

Active managers are free to continue holding or increasing exposure

Access to Capital

Analysts warn that exclusion could “signal” risk. But markets adapt quickly. As long as a company is:

Liquid

Transparent

Able to raise capital

Able to communicate its treasury policy It remains investable. Index exclusion is an inconvenience—not a structural impairment.

Precedent Risk

If MSCI embeds asset-based exclusion rules, it sets a template for removing companies based on their savings decisions rather than their business fundamentals.

That is a path toward politicizing global benchmarks.

6. The Global Competitiveness Problem

Bitcoin treasury strategies are expanding internationally:

Japan (Metaplanet)

Germany (Aifinyo)

Europe (Capital B)

Latin America (multiple mining and infrastructure firms)

North America (Strategy, ABTC, miners, and energy-Bitcoin hybrids)

If MSCI excludes these companies disproportionately, U.S. and Western companies are placed at a competitive disadvantage relative to jurisdictions that embrace digital capital.

Indexes are meant to reflect markets—not pick national winners and losers.

7. MSCI Already Knows That Exclusion Creates Distortion

MSCI’s recent handling of Metaplanet’s public offering shows it understands the risks of “reverse turnover.” To avoid index churn, MSCI chose not to implement the event at the time of offering.

This acknowledgement underscores a broader truth: rigid rules can destabilize indices. A digital-asset threshold creates similar fragility on a much larger scale.

8. Better Alternatives Exist

MSCI can achieve transparency and analytical clarity without excluding lawful operating companies.

A. Enhanced Disclosure

Require standardized reporting of digital-asset holdings in public filings. This gives investors clarity without altering index composition.

B. Classification or Sub-Sector Label

Add a category such as “Digital Asset Treasury–Integrated” to help investors differentiate business models.

C. Liquidity or Governance Screens

If concerns are about liquidity, governance, or volatility, MSCI should use the criteria it already applies uniformly across sectors.

None require exclusion.

9. Why the Proposal Should Be Withdrawn

The proposal does not solve a real problem. It creates several:

Reduces representativeness of global indices

Violates neutrality by discriminating against a specific treasury asset

Creates unnecessary turnover for passive funds

Damages global competitiveness

Sets a precedent for non-neutral index construction

Bitcoin is money. Companies should not be penalized for saving money—or for choosing a long-term treasury asset that is more liquid, more transparent, and more objectively priced than most corporate intangibles.

Indexes must reflect markets as they are—not as gatekeepers prefer them to be.

MSCI should withdraw the proposal and maintain the neutrality that has made its benchmarks trusted across global capital markets.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

For the first time in financial history, a major credit rating agency has formally evaluated a company built on a bitcoin-backed credit model. In news covered by Bitcoin Magazine, the S&P Global Ratings has assigned Strategy Inc (MSTR) a ‘B-’ Issuer Credit Rating with a Stable outlook, recognizing not just the company, but the emergence of Bitcoin as collateral inside the credit system. This marks a watershed moment for corporate finance.Bitcoin-backed credit is no longer theoretical. It is now a rated financial reality.

Why This Moment Matters

Until now, Bitcoin had been accepted by equity markets, ETFs, and corporate treasury conversations — but credit markets remained untouched. Credit markets are where legitimacy is ultimately decided because they determine who can borrow, at what cost, and against which assets.

By rating Strategy Inc, S&P has implicitly acknowledged:

Bitcoin can underpin structured debt and preferred equity.

A bitcoin-backed credit strategy can be modeled, rated, and priced using traditional frameworks.

Bitcoin is shifting from speculative asset to recognized collateral within corporate capital structures.

This is not a marketing milestone — it is a structural one. Bitcoin has entered the language of risk-adjusted return, yield, and covenants.

How S&P Interpreted Strategy’s Bitcoin-Backed Capital Model

The rating is speculative grade, but the Stable outlook is critical. It signals S&P’s belief that Strategy can continue to service obligations and access capital markets without selling its Bitcoin reserves — a foundational principle of bitcoin-backed credit.

S&P’s analysis mentions several possible weaknesses:

High concentration of assets in Bitcoin

Low U.S. dollar liquidity and negative risk-adjusted capital under S&P’s methodology

Currency mismatch: long Bitcoin, short U.S. dollar debt obligations

However, they also credited Strategy with unique structural strengths:

No near-term debt maturities before 2027–2028

Proven access to capital markets — both equity and debt

A capital stack purpose-built to accumulate Bitcoin without diluting shareholders

Active liability management via convertible debt and preferred stock instruments

In short, S&P is signaling that bitcoin-backed credit can function — if managed with discipline.

Implications for the S&P 500 and Institutional Legitimacy

Strategy Inc met the S&P 500 inclusion criteria in profitability and market capitalization but was passed over in 2024, widely believed to be due to its Bitcoin-heavy balance sheet. That decision now appears less defensible.

With a formal credit rating, the company shifts from “unrated anomaly” to “rated issuer.” For institutional capital, that distinction matters.

Index committees can now reference a risk rating — not just a narrative.

Treasury teams and insurers can benchmark exposure to bitcoin-backed credit against traditional corporate debt.

This increases (not guarantees) the probability of future index inclusion and passive capital flows.

Bitcoin entering equity indices begins with Bitcoin entering the credit models behind them.

Bitcoin-Backed Credit: The Ideal State of Treasury Strategy

This rating does more than validate Strategy — it validates the architecture of bitcoin-backed credit as the superior evolution of corporate treasury management.

Phase 1 was equity-funded Bitcoin accumulation — high growth but shareholder dilution. Phase 2 introduced convertible debt and preferred equity — allowing companies to acquire Bitcoin through capital markets rather than operating earnings. Phase 3, now underway, is full institutional recognition of bitcoin-backed credit — rated, benchmarked, and capable of scaling.

This is the endgame:

Use capital markets to borrow in fiat

Use proceeds to acquire Bitcoin

Service liabilities without selling reserves

Increase Bitcoin-per-share over time, without issuing new common stock

With S&P formally rating Strategy’s issuer credit, this model moves from innovation to infrastructure.

Why Corporate Finance Leaders Need to Pay Attention

This rating does not compel companies to adopt Bitcoin. But it removes the claim that Bitcoin cannot be integrated into traditional credit systems.

From now on:

Bitcoin can be factored into risk-weighted capital models and treasury policy.

Credit and liquidity committees must understand how bitcoin-backed credit affects financing costs, refinancing risk, and balance sheet leverage.

Investors can now compare Bitcoin-based capital structures against other high-yield or hybrid debt strategies.

Boards can no longer dismiss Bitcoin as “unratable” or “unclassified.”

A New Chapter for Corporate Finance and Capital Markets

What makes this moment different isn’t that another institution “acknowledged” Bitcoin. That’s happened before with ETFs, GAAP accounting changes, and treasury allocations.

What’s different is where the recognition has now occurred: Not in equity markets. Not in payment networks. But in credit — the foundation of corporate finance and monetary systems.

When a credit rating agency like S&P evaluates a company built on Bitcoin, it does three things that have never happened before:

It forces Bitcoin into risk models normally reserved for banks, sovereigns, and investment-grade corporations.

It legitimizes bitcoin-backed credit as a structure that can be analyzed, refinanced, and scaled — not dismissed as speculative.

It signals to other corporates and lenders that they must now understand Bitcoin not as an investment, but as collateral.

This rating does not mean the model is risk-free. It means the model is real enough to underwrite, stress test, and lend against.

That is the real inflection point — not that S&P approved of Bitcoin, but that they were forced to measure it.

Disclaimer: This content was written on behalf of Bitcoin For Corporations. This article is intended solely for informational purposes and should not be interpreted as an invitation or solicitation to acquire, purchase or subscribe for securities.

Prenetics Global Limited (NASDAQ: PRE), a Hong Kong-based health sciences company, announced today the successful pricing of a public equity offering expected to generate approximately $48 million in gross proceeds, with the potential to raise up to $216 million if all accompanying warrants are exercised.

The company has a disciplined Bitcoin accumulation plan, purchasing one bitcoin per day since August 1, 2025, and currently holds approximately 275 BTC, valued at $31 million as of October 27.

Prenetics said the offering attracted a distinguished group of institutional and individual investors, including major crypto platforms and financial firms such as Kraken, Exodus (NYSE: EXOD), GPTX by Bitcoin mining pioneer Jihan Wu, American Ventures LLC, XtalPi (2228.HK), DL Holdings (1709.HK), and Mythos Group, among others.

The offering, led by sole placement agent Dominari Securities LLC, consists of 2,992,596 Class A ordinary shares and/or pre-funded warrants, along with Class A and Class B warrants exercisable for up to 5,985,192 additional shares.

The Class A warrants carry an exercise price of $24.12 — 50% above the offering price of $16.08 — while the Class B warrants are exercisable at $32.16, or a 100% premium. Both warrants are immediately exercisable upon issuance and have five-year terms.

High-profile strategic investors like Aryna Sabalenka, the world No. 1 tennis player, and Adrian Cheng, a prominent Asian entrepreneur, also increased their stakes in the company. David Beckham is also a prominent backer.

Prenetics’ supplement brand IM8 hit $100 million ARR in 11 months and aims for $180–$200 million in 2026 within the $704 billion global market, the company said.

CEO Danny Yeung highlighted the company’s dual focus on health supplements and cryptocurrency.

“IM8 has huge global potential, evidenced already by our extraordinary traction across multiple markets. We’re particularly honored to have the backing of a distinguished group of new and existing strategic investors who share our confidence in our dual-engine strategy,” Yeung said.

Bitcoin accumulation: One bitcoin per day

As mentioned earlier, Prenetics has a Bitcoin accumulation plan, purchasing one bitcoin per day since August 1, 2025, and currently holds approximately 275 BTC, valued at $31 million as of October 27.

Financially, Prenetics will hold roughly $100 million in cash post-offering, bringing its total liquidity — including Bitcoin holdings — to around $131 million.

The company also plans to review and divest non-core business units to focus resources on IM8 and Bitcoin initiatives.

The offering is expected to close on or around October 28, 2025, pending customary conditions. Prenetics positions itself as pursuing a bold long-term ambition: to reach $1 billion in annual revenue alongside $1 billion in Bitcoin holdings within the next five years, combining health supplement growth with cryptocurrency accumulation as a cornerstone of its corporate strategy.

IM8’s operational performance underscores the brand’s subscription-driven growth model, with more than 12 million servings shipped to over 420,000 customer orders across 31 countries.

Average order values have risen from $110 to $145 following the launch of IM8’s Daily Ultimate Longevity product, reflecting strong consumer demand for premium offerings.

German fintech company aifinyo AG (Ticker: EBEN) has announced its ambitious plan to become Germany’s first pure-play Bitcoin treasury company, with a target of accumulating over 10,000 Bitcoin by 2027. The announcement marks a significant milestone for corporate Bitcoin adoption in Europe’s largest economy.

The company has already invested €3 million in Bitcoin purchases, complemented by an additional €3 million investment from strategic partner UTXO Management. Aifinyo plans to convert future operating profits from its B2B payments business into Bitcoin purchases, creating what Garry Krugljakow, the company’s head of Bitcoin strategy, describes as a “self-reinforcing cycle.”

“Within five years at most, every DAX company will have to consider whether they need Bitcoin on their balance sheet – as inflation protection and strategic reserve,” Krugljakow stated. “We’re proving today that it works — with a German business model, German regulation, and a global Bitcoin strategy.”

Aifinyo operates Smart Billment, a digital invoice management platform serving approximately 8,000 B2B customers. This operational foundation provides steady capital inflows for its Bitcoin accumulation strategy. The company’s regulatory framework is particularly noteworthy, as it operates two supervised subsidiaries: aifinyo finance GmbH and aifinyo payments GmbH, with Bitcoin custody handled through institutional cold storage solutions at German custodians.

UTXO Management’s co-founder, Tyler Evans, who made an early decision to invest in aifinyo, noted: “It was high time Germany got a Bitcoin treasury approach of this quality. Here all the factors for success come together: profitable business, experienced management, and a solid regulatory framework.”

The timing of aifinyo’s initiative coincides with growing corporate Bitcoin adoption globally. As of October 2025, publicly traded companies hold over $110 billion worth of Bitcoin, with Strategy (formerly MicroStrategy) alone holding approximately 640,400 BTC worth roughly $70 billion.

The company joins the Bitcoin for Corporations initiative, which currently represents 38 member companies holding 69% of all corporate Bitcoin holdings. “Corporate bitcoin adoption continues to expand its global footprint,” said George Mekhail, Managing Director of Bitcoin for Corporations at BTC Inc. “We’re thrilled to welcome aifinyo as the first Bitcoin Treasury company in Germany.”

Aifinyo CEO Stefan Kempf summarized the company’s vision: “We’re building the first German Bitcoin-Maschine. Every invoice our 8,000 customers pay now generates Bitcoin for our shareholders.“

For Germany, traditionally known for its financial conservatism, this development signals a significant shift in corporate treasury management strategies, potentially paving the way for broader institutional Bitcoin adoption in Europe.

aifinyo AG is the member of Bitcoin for Corporationsconnected to Bitcoin Magazine via shared ownership, as BTC Inc operates Bitcoin For Corporations, a platform focused on corporate adoption of Bitcoin.

aifinyo AG is a portfolio company of UTXO Management, a regulated capital allocator focused on the digital assets industry. Bitcoin Magazine is owned by BTC Inc., which operates UTXO Management. UTXO invests in a variety of Bitcoin businesses, and maintains significant holdings in digital assets.