Learn how breakeven analysis helps SaaS and tech teams understand when revenue covers costs, optimize pricing, and build profitable, scalable growth models.

Learn how breakeven analysis helps SaaS and tech teams understand when revenue covers costs, optimize pricing, and build profitable, scalable growth models.

AI Meets Blockchain Lending: Smarter Credit, Lower Risk, and Faster Decisions

The future of finance isn’t just digital — it’s intelligent. For years, blockchain has transformed how we build trust in financial systems. But now, artificial intelligence (AI) is adding something blockchain alone couldn’t: judgment.

Together, AI and blockchain lending platforms are creating a world where credit decisions are faster, risk is lower, and finance becomes fairer — powered by data, not paperwork.

Traditional credit systems are broken. They depend on outdated data, slow verification, and biased scoring models.

Borrowers with strong repayment behavior but no formal history — like freelancers, gig workers, or small business owners — are often rejected. Lenders, on the other hand, struggle to evaluate real-time risk or detect fraud quickly enough.

The result? Slow approvals, rising defaults, and missed opportunities for millions of borrowers worldwide.

That’s where AI + blockchain step in to rebuild trust — not with paperwork, but with precision.

🧩 Why AI and Blockchain Are the Perfect Pair

Think of blockchain as the memory of finance — secure, transparent, and tamper-proof. And think of AI as its intelligence — the ability to analyze, learn, and make predictions.

Together, they solve the two biggest challenges in lending:

Trust

Accuracy

Blockchain records every transaction immutably, while AI interprets that data to make smarter lending decisions. The result? AI blockchain finance systems that are not only transparent — they’re adaptive and predictive.

⚙️ How It Works: Smarter Lending with AI and Blockchain

Data Collection (On-Chain + Off-Chain): AI gathers transaction histories, payment patterns, and asset ownership directly from blockchain ledgers and verified external sources.

Risk Analysis: Machine learning models assess borrower profiles and market behavior in real time — detecting early signs of default or fraud.

Smart Contract Lending: Loans are issued through smart contracts — automated agreements that enforce terms, manage collateral, and trigger repayments without intermediaries.

On-Chain Credit Scoring: Instead of relying on paper-based credit reports, blockchain-based on-chain credit scoring builds a transparent reputation for each borrower.

Continuous Learning: As borrowers repay or default, AI models learn and adjust risk parameters — making the system smarter over time.

This synergy creates an ecosystem where every decision is data-backed, verifiable, and lightning fast ⚡

💡 Real-World Use Cases of AI + Blockchain Lending

Let’s see what this looks like in action 👇

1. DeFi Lending Platforms AI monitors liquidity pools and borrower patterns in real time, flagging risky loans automatically. Combined with smart contract lending, this prevents defaults before they happen.

2. NBFC Blockchain Integration Traditional NBFCs use AI-driven risk control to analyze both blockchain data and traditional metrics — cutting loan processing times from days to minutes.

3. Token-Based Microcredit Systems AI tracks borrower performance, while blockchain ensures reward distribution through token-based lending systems. Borrowers build trust, lenders gain transparency.

In the old world of finance, risk management meant reactive measures — audits after losses, reports after defaults.

But in blockchain lending, AI-driven risk control is proactive. It monitors market volatility, borrower behavior, and on-chain activity 24/7. It detects red flags before they escalate — and can even auto-adjust collateral ratios via smart contracts.

This isn’t just safer — it’s smarter.

By combining AI blockchain finance tools with on-chain credit scoring, lenders can achieve near-zero fraud rates and instant compliance.

📊 The Benefits of AI-Blockchain Lending

When AI meets blockchain, lending transforms across every level of finance 👇

Speed: Instant decisions powered by automated smart contracts. Accuracy: AI eliminates human bias and uses data-driven insights. Transparency: Every transaction and credit event is recorded on-chain. Security: Immutable blockchain records prevent tampering or manipulation. Inclusion: Borrowers without traditional credit can prove trustworthiness through on-chain data.

For lenders, it means reduced operational costs and smarter risk modeling. For borrowers, it means fairer access and faster approvals. For the entire ecosystem — it means trust without friction.

NBFC blockchain integration for compliant digital lending

Scalable token-based lending systems with real-time risk visibility

Our mission is simple — to help financial innovators launch fintech blockchain solutions that are smarter, faster, and safer.

🔮 The Future: Intelligent Finance on the Blockchain

The next generation of financial systems will do more than just automate — they’ll think.

AI will predict borrower behavior, while blockchain guarantees every outcome. Decisions will be made in seconds, not days. Credit scoring will be earned through transparent activity, not paperwork.

In this future, AI blockchain finance becomes the foundation of trust — a global system where everyone has fair, data-driven access to credit.

The combination of AI and blockchain isn’t just innovation — it’s evolution. Together, they redefine how we see trust, risk, and opportunity in finance.

By integrating AI-driven risk control, on-chain credit scoring, and smart contract lending, financial institutions can move faster and smarter — without sacrificing security.

💼 At Duredev, we help turn that vision into reality — building blockchain finance infrastructure where intelligence meets transparency, and trust meets automation.

🔗 Important Links

Ready to create your own AI-powered lending ecosystem? Let’s build it together — with Duredev blockchain development at the core. 🤝

A combined obituary for TradFi’s (mis)understanding of bitcoin’s underlying value.

This article was written in response to a statement made by European Central Bank President Christine Lagarde in an October 7, 2025, interview, where she claimed that bitcoin has “no intrinsic” or “underlying value.”

When Christine Lagarde says Bitcoin has no “intrinsic” or “underlying value,” she’s (likely) referring to the fact that it — unlike an equity — doesn’t produce a cash flow. The classic critique that follows is that it’s “purely speculative”, meaning it’s only worth what someone else is willing to buy it for in the future.

She further dismisses Bitcoin as a form of “digital gold” and seems to suggest that physical gold is somehow different — presumably because she assigns it value for its use cases beyond its function as money (if I had to guess).

To say that Bitcoin doesn’t have a cash flow is factually correct — but as nonsensical as saying “language” or “mathematics” have no cash flow.

One could, of course, counter Lagarde’s statement by appealing to the subjective value proposition — arguing that there’s no such thing as intrinsic value, since all value is subjective, and that anything can only ever be worth what someone else is willing to pay for it in the future.

But instead of taking that route, I’ll go the roundabout (and more entertaining) way of showing why she’s not only wrong, but also inconsistent by her own logic.

Let’s start with gold and the idea that something supposedly has “intrinsic value” because it has a use case beyond its function as money — to get that out of the way.

Gold

We’ll start with a forum excerpt from Satoshi themselves:

The entire point of money is to be one step removed from bartering — to serve as a neutral medium that communicates the underlying economic reality between supply and demand in an economy, allowing participants to make maximally informed decisions.

For this reason, throughout history, the evolution of money has consistently trended toward what cannot be easily recreated at will. The reason is simple: it’s within everyone’s self-interest, and the economy as a whole (as we will see), that the money being used and accepted cannot be diluted.

If gold were assumed for a moment to be absolutely scarce and used solely as money, the price of an apple becomes a pure function of supply and demand. The price, expressed in gold, could only change if the real supply or demand for apples changed. In this setup, all market participants are maximally informed and economic reality is upheld.

Apple price = f(Apple supply, Apple demand)

If, however, gold all of a sudden gained demand for some other purpose, such as being used for jewellery, the dynamics change. The price of an apple now becomes a function not only of the supply and demand for apples, but also the jewellery demand, as it’s causing a change in the denominator (money) itself. The result is a less-than-ideal form of money, where economic reality is distorted and market participants are presented with compromised information.

Apple price = f(Apple supply, Apple demand, Jewellery demand)

Note that this is materially different from a setup where, as in the real economy, billions of participants want billions of different things while still using the same money.

Money is merely the measuring stick, which means that the demand for bananas isn’t going to affect the price of apples just because both prices are expressed in the same unit of account. What is going to distort prices is if people start demanding the good being used as money for something other than its monetary function.

The irony here, of course, is that gold’s supposed “usefulness” — beyond money — its role in jewellery or industry — which supposedly makes it an exception to the rule of having underlying value, actually makes it less perfect as money. By having a non-monetary use, gold introduces an additional demand parameter into what’s meant to be a neutral measuring stick.

The ideal money, as Satoshi pointed out, would be a kind of “grey metal” — something with no other purpose than being perfect money itself. That “grey metal” is, of course, Bitcoin.

Let’s now move on to cash flows — the main topic of discussion whenever TradFi talks about “underlying” or “intrinsic” value.

After all, many of the same people who point out that Bitcoin doesn’t have any aren’t as internally conflicted as Lagarde, and extend the same judgment to gold (that it doesn’t have intrinsic value)— which, at the very least, is a more consistent position.

Cash flows

Last year, Meta (Facebook), Google, and Amazon reported combined cash flows of roughly $160 billion. If someone asked Lagarde whether these equities had an underlying value, she would of course say yes. Each company sits on billion-dollar assets and billion-dollar expected future cash flows that can be discounted to generate an equity valuation.

Bitcoin, on the other hand, has no comparable cash flows to speak of — no disagreement there.

But before we go further, let’s ask: Where do those cash flows actually come from? In other words, what is the driver of those cash flows fromMeta, Google, and Amazon?

We’ve all used Facebook. It offers a global platform for people to connect, message, and share. Its revenue comes from selling ads on top of user attention. Why do people use Facebook? Because everyone else does. Because it offers the best experience. It’s a social network, meaning every new user adds value to everyone else.

What about Google? Same logic. It’s the world’s leading search engine — the front door of the internet. It also monetises through targeted advertising. Why do you use Google instead of Yahoo or Bing? Because everyone else does. The more data it gathers, the better it gets for everyone. Another network effect (often leading to winner-take-all outcomes).

Amazon? Same principle, different domain. It’s the default marketplace of the world, connecting buyers and sellers on a global scale. Amazon profits from subscriptions and logistics fees. Consumers use it because every supplier is there; suppliers use it because every consumer is there. Every new participant makes the network more useful. It started with books — now it sells everything.

Now, imagine each of these companies woke up one morning after a collective bump to the head, decided profit was overrated, and poured their fortunes into an endowment run entirely by an AI workforce — keeping the networks running exactly as before, just without the monetisation.

Shareholder value would immediately drop to zero.

But what about the network? Would people still use Facebook, Google and Amazon? Of course!

Because the underlying value to the users was never the company itself — it was the network it monetised (which they had no other way of accessing without going through that monetisation). The fact that the network now costs nothing or very little to use wouldn’t make it less valuable for them, now would it?

The equity value and the network value are two different things.

The Bitcoin Company

Now, imagine another startup with a single vision: “We’re going to build the best money in the world.”

Its service is to launch a global network for value transfer and storage, promising a monetary asset with a fixed supply of 21 million units forever — no dilution, no exceptions (pinky promise). The monetisation model: small transaction fees, 10x lower than competitors.

We call it “The Bitcoin Company”.

Imagine it miraculously gained some early traction. Why would people continue or grow interested in using it? Well, because more and more people does. And as they do, both the equity value of those owning the company (as they collect fees) and the network value to the users would grow.

There you’d have your cash flows.

Ironically, this is the same “business model” that underpins the central banking system, only they defaulted on their original promise. By positioning themselves as issuers atop the fiat monetary network, central banks and megabanks monetise it through two layers.

At the base lies the fiat monetary network, consisting of state-backed money. Central banks monetise this layer by issuing the very units the network runs on and indirectly financing government deficits. Above them, megabanks monetise the same network through credit creation, earning profits from interest on loans, and now increasingly from stablecoins (which is like credit on top of credit.).

Lagarde insists stablecoins are “different” because she views them as network expanders that amplify the monetary network she controls. Just as Facebook’s advertising revenue grows with its user base, the spread of stablecoins enlarges the euro monetary network, giving central banks greater room for monetary expansion.

From her perspective, this expansion of units as the network grows functions like “cash flow” in the business model of central banking — and, in her eyes, that’s what constitutes its underlying value.

The fiat monetary network stack. Stablecoins has the potential to expand the fiat monetary network.

Now imagine the same twist: the Bitcoin Company dissolves. No CEO. No board. No office, anymore. The equity value and the cash flows immediately go to zero, but the Bitcoin Network remains —operations henceforth run without rulers (according to some “decentralised consensus protocol” dreamt up one night by some mysterious entity called Satoshi).

Ask yourself: would that make the network more or less valuable?

To be clear — we’ve just removed all counterparty risk. No late-night CEO tweets. No offices to raid. No conflict of interest. No Coldplay scandals.

The network just became (1) even cheaper to use, and (2) even the tiniest worry about that pinky promise was just erased (which, to be fair, you probably should have been pretty worried about).

So yes, from the user’s perspective, the network just became more valuable.

Equity value vs Network value

Christine Lagarde simply hasn’t done the intellectual groundwork needed to understand what she’s critiquing. Like so many others before her, she’s mistaking equity value (which generates cash flows) for the network value — without recognising the path dependency between them: there would be no cash flows without the network in the first place (!)

The wrong question: What is the equity value of the company monetising the network? The right question: What is the network’s value to the users?

In other words:

What is the value of being able to speak with anyone in the world, for free, instantly, across borders and cultures? (Facebook)

What is the value of instantly accessing the world’s knowledge? (Google)

What is the value of finding, comparing, and receiving any product from anywhere on Earth, delivered in a day? (Amazon)

What is the value of moving your money — across borders and across time? Perhaps even more refined, what is the value of undistorted price signals in an economy? (Bitcoin)

The Bitcoin network isn’t valuable despite not being a company — it’s more valuable because it isn’t.

Unlike Meta, Google, or Amazon — whose networks power applications and commerce —the Bitcoin network provides the monetary foundation beneath them all. Its total addressable market is every transaction on Earth.

Now, you could try to build a straw man argument by claiming that the Bitcoin network isn’t truly a monetary network, since it isn’t “widely accepted” by your standards. The problem with that line of reasoning is (1) it implies that nothing new could ever emerge under the sun unless the entire world agreed on it in advance (pretty unreasonable), and (2) it would, by your own logic, require you to dismiss over 90% of the world’s sovereign currencies as money — including the Canadian dollar, the Swedish krona, and the Swiss franc — since Bitcoin’s market capitalisation already surpasses them many times over and would likely be accepted as payment by far more people globally.

The Bitcoin Network ranks 8 out of 108 fiat currencies. Source.

Returning to the initial claim, to say that Bitcoin doesn’t have a cash flow is factually correct — but as nonsensical as saying “language” or “mathematics” have no cash flow. True enough, not in themselves — but they’re indispensable tools for creating everything that does.

In fact, if the money you’re using did offer cash flows (an interest rate yield), that would be a sign you were dealing with defective money.

Let me explain why in the simplest terms:

Suppose the total money supply is $100,000, and ten depositors each place $10,000 into a bank. The bank offers them 4% interest and lends out the full amount to borrowers at 5%. After a year, the borrowers owe $105,000 in total (principal plus interest).

Do you see the problem?

The borrowers owe more money than exists in the entire system. Where does the extra $5000 come from?

No amount of productivity or hard work can solve this mathematical impossibility. The only thing that can is the creation of new money to fill the gap. For the system to keep running, the money supply would have to grow at par with, or faster than, the interest rate being offered to depositors. It’s the only way the math can work out. That means the supposed “cash flow” being offered in the form of an interest rate is being paid for by diluting the very money it’s denominated in, which is the very definition of a Ponzi scheme (!)

The result is a lesser form of money — one that must constantly lose value for the math to work out.

It would now appear we’re at a paradoxical intersection: on one hand, Lagarde and others dismiss Bitcoin’s underlying value on the grounds that it has no cash flow; on the other, we can now see that if it did have a cash flow, it would by definition be flawed money.

It therefore seems that the very trait that makes Bitcoin perfect money — its inability to conjure fake cash flows out of thin air — is precisely what’s being used to dismiss it by those defending a system that only functions by doing exactly that. So how do we work this out?

Here lies the crucial insight that Lagarde, and many others, fail to grasp: something can possess underlying or intrinsic value in a roundabout way.

The roundabout way

Take car insurance (or any other insurance policy, for that matter). Judged in isolation, it has a negative expected value — you pay premiums every month, and it’s structurally priced so that you’ll never get rich buying infinite insurance policies (if that were possible, everyone would).

But when you combine the policy with the car you own and depend on — the picture changes. You’ve now removed the risk of potential ruin. Evaluated together, you now have a situation where the insurance policy explodes in value (generating a positive cash flow) precisely when you need it most — when the car breaks down. Viewed as a whole, you end up with a positive geometric return (that is, underlying value through the omission of ruin) when the accident eventually occurs, which, odds are, it eventually will.

Cash flow/usefulness of an insurance policy.

To illustrate this more practically, consider a scenario where a person depends on their car to get to work. Without insurance, a breakdown might mean they can’t afford the repair, resulting in the loss of both the car and their income. With insurance, however, the repair is covered, allowing them to maintain their income stream. In this way, the insurance policy has value far beyond its direct payoff, as it preserves the ability to keep generating cash flow.

Y axis = Cash flow from income.

This, as we shall now understand, is the entire logic behind money in the first place — and we could just as easily swap the insurance policy for a stack of cash (which is really just a more universal, unspecific form of insurance). You save money not because it generates a cash flow, but because it gives you future optionality and explodes in usefulness when you need it most, allowing you to quickly recover and adapt when the unexpected occurs.

This is not speculative behavior. The reason you hold money is not because you’re engaging in what critics accuse you of — the “greater fool” prediction business, but precisely because you want to avoid it! You hold money not because you’re making a prediction of the future, but because you know you can’t, and therefore want to be ready for whatever it brings. After all, why would you pay for car insurance if you knew you would never need it?

The “greater fool” argument collapses under closer scrutiny because it assumes every individual faces the same circumstances, preferences, and time horizons. It treats the economy as a zero-sum game in which one person’s prudence must come at another’s expense. But reality is the opposite: what’s rational for each participant depends on their unique position in time and space.

Someone sitting on a vast reserve of cash might rationally choose to exchange part of it for a new car with a better A/C that improve their comfort and quality of life. Someone else, with less savings or living in a colder climate, might rationally do the precise opposite — defer a new car purchase and strengthen their savings buffer. Both are acting rationally within their own context. The latter isn’t a “greater fool” for buying the money the former is selling for a car. They’re both winners! Otherwise they wouldn’t agree to the trade in the first place!

Markets exist precisely because we don’t share the same circumstances or needs. The value of money, then, isn’t born from finding a “greater fool”, but from coordinating billions of rational actors, each seeking to balance their own lives in their own way.

We can extend this observation to all the networks and protocols mentioned earlier. Whether it’s a monetary network, a social network, mathematics, or language — each derives its value in a roundabout way that continues to fly over the heads of people like Lagarde, whose job ironically is supposed to be an expert on these things.

Kraken and Deutsche Börse has announced a strategic partnership that will integrate crypto with traditional market infrastructure.

Kraken And Deutsche Börse Have Partnered Up

As announced in a press release, US-based digital asset exchange Kraken has teamed up with Deutsche Börse Group to bridge crypto and traditional finance and deliver institutional investors access across asset classes.

Headquartered in Frankfurt, Deutsche Börse Group is one of the biggest financial market infrastructure providers in the world. It operates the Frankfurt Stock Exchange, which ranks the 12th largest in market cap globally.

In the first phase of the partnership, Kraken will integrate directly with 360T, a subsidiary of the German multinational corporation that provides foreign-exchange trading services. This integration will provide Kraken clients access to the latter’s foreign-exchange liquidity.

The partnership will go the other way, as well. Via Crypto Finance, another Deutsche Börse subsidiary, and Kraken, Deutsche Börse Group clients will be able to trade cryptocurrencies and derivatives.

The two firms also plan to leverage Kraken Embed, the crypto trading infrastructure solution created by Kraken, to provide institutions in Deutsche Börse Group’s network with digital asset access.

The press release noted:

Together, the companies will develop advanced white-label solutions enabling banks, fintechs, and other financial institutions to offer secure, compliant crypto trading and custody services to clients across Europe and the U.S.

Another thing Kraken and Deutsche Börse Group are collaborating on is integration of xStocks in the ecosystem of 360X, Deutsche Börse’s tokenized trading venue. xStocks is a stock tokenization standard that has been gaining adoption. Kraken announced the acquisition of Backed, the company behind xStocks, just this Tuesday.

Arjun Sethi, Kraken Co-CEO, said:

By linking traditional and digital markets across a wide range of asset classes, we’re building a holistic foundation for the next generation of financial innovation: defined by efficiency, openness, and client access.

The companies are also looking to make derivatives listed on Deutsche Börse Group’s Eurex, the largest futures and options marketplace in Europe, available on Kraken, if regulators provide the nod.

Stephan Leithner, Deutsche Börse CEO, noted:

This collaboration with Kraken is a great strategic fit for Deutsche Börse Group. It underscores our ongoing commitment to shaping the future of financial markets by combining the trust and resilience of our regulated infrastructure with the innovation of the digital asset ecosystem.

Back in October, the German organization also announced another crypto partnership, this one with USDC issuer Circle. The collaboration aimed to integrate the latter’s USD and EUR stablecoins in the former’s infrastructure to boost stablecoin adoption in Europe.

Bitcoin Price

At the time of writing, Bitcoin is trading around $92,500, up 1% over the last week.

Yearn Finance has taken its first major step toward repairing the damage from its recent yETH exploit after securing a partial recovery. Yearn Finance has recovered $2.4 million from the $9 million yETH exploit that hit the protocol at the…

Yearn Finance reported that a legacy yETH product was hit by an exploit that allowed an attacker to mint a massive amount of fake tokens and swap them for real assets.

According to on-chain alerts and protocol statements, the attacker created a near-infinite supply of yETH in a single transaction, then used those tokens to pull ETH and liquid-staking derivatives from liquidity pools.

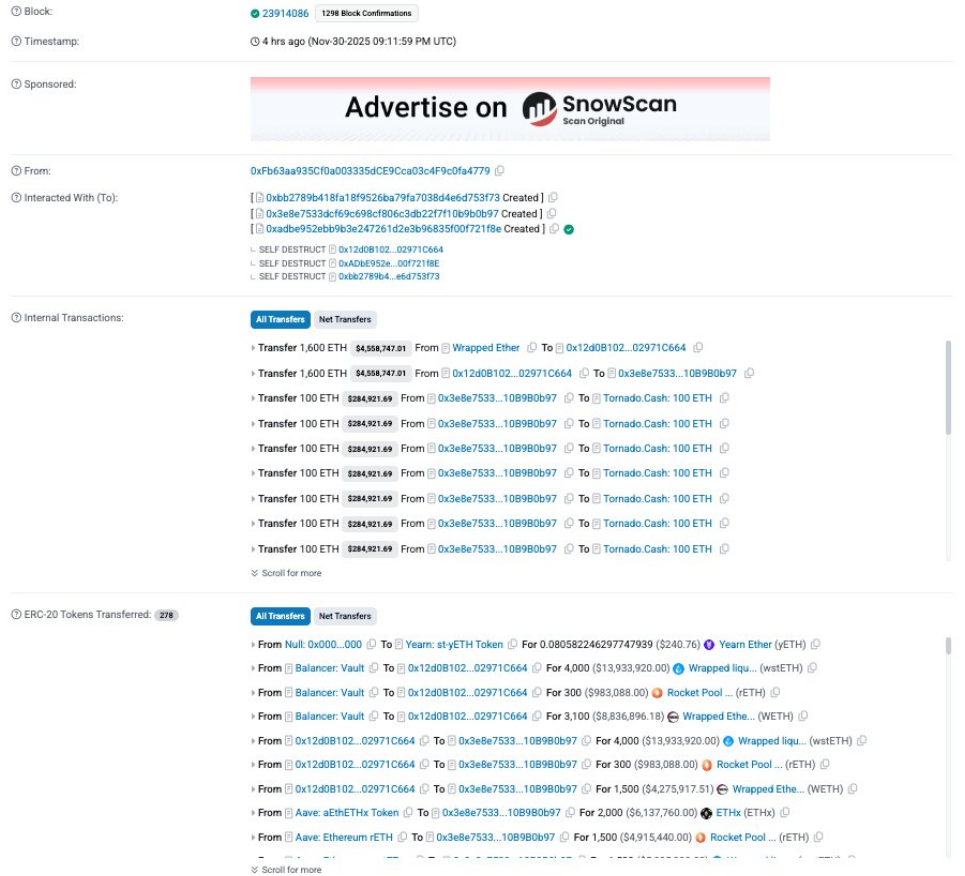

The incident was first flagged on November 30, 2025, and the total impact has been reported at roughly $9 million.

Based on reports, the attacker took advantage of a flaw in the yETH minting logic and produced tokens on the order of 235 trillion in one go.

Those worthless tokens were then swapped for real assets from Balancer and Curve pools tied to the product, emptying liquidity in minutes. Chain monitors and security researchers showed the mint and subsequent swaps unfolding very quickly on the blockchain.

At 21:11 UTC on Nov 30, an incident occurred involving the yETH stableswap pool that resulted in the minting of a large amount of yETH. The contract impacted is a custom version of popular stableswap code, unrelated to other Yearn products. Yearn V2/V3 vaults are not at risk.

Reports have disclosed that roughly $8 million was pulled from the main yETH stable-swap pool, while about $0.9 million was taken from a yETH–WETH pool.

In addition, roughly 1,000 ETH—valued at about $3 million at the time of movement—was sent to Tornado Cash in attempts to obscure the trail. The attacker converted fake yETH into a mix of ETH and liquid staking tokens before attempting to launder funds.

Impact On Yearn’s Core Products

According to Yearn officials and follow-up coverage, the breach was limited to an older, legacy implementation of the yETH product and did not affect Yearn’s main V2 and V3 vaults.

Deposits into the affected pool were isolated while the team and outside experts began an investigation. This isolation is said to have kept the bulk of user funds in active vaults from being touched.

Market Reaction And Wider Concerns

Crypto markets saw selling pressure as the news spread, with traders weighing the risk that comes from combining liquid staking tokens with custom swap code.

Yearn Finance said it is working with outside security teams to run a post-mortem and to patch the vulnerability. Based on reports, teams named in coverage include external auditors and blockchain investigators who are tracking the stolen funds and advising on recovery options.

The protocol’s notice warned users about the affected legacy product and urged caution while the review continues.

Featured image from Unsplash, chart from TradingView

According to blockchain data, the exploit generated a near-infinite number of yETH, draining millions from Balancer pools. Attackers roughly profited 1,000 ETH, worth $3 million, which was routed through the Tornado Cash mixer, Chinese journalist Colin Wu noted.

yETH is an index token consisting of several different liquid staked versions of ETH, in other terms, Ethereum Liquid Staking Derivatives (LSTs). The attack was first flagged by an X user Togbe, who highlighted “heavy transactions” on LSTs, including yearn, rocket pool, origin and dinero.

yETH Incident Puts DeFi Security Under Lens

The incident apparently involved several newly deployed smart contracts, which self-destructed after the transaction, per blockchain data. The total financial losses remain unclear; however, the yETH pool had a total value around $11 million prior to the attack, Dexscreener data shows.

Following the exploit, mixed reactions came from the community, with some expressing concern over the continued use of outdated contracts.

Besides, Yearn Finance suffered a hack in 2021, affecting its yDAI vault and losing $11 million in value. The hacker apparently got away with $2.8 million at that time. Later, that protocol flagged a faulty script in December 2023, wiping out 63% of a position in its treasury.

Crypto Lost $127M to Hacks, Scams in November Alone

Meanwhile, blockchain security firm CertiK confirmed on Sunday that the crypto industry suffered an estimated $127 million in losses to hacks and exploits.

The company’s monthly threat report noted that the actual affected funds were more than $172 million. However, the numbers reduced by $45 million after some of the stolen funds were recovered.

Yearn Finance is dealing with a fresh security breach after an attacker exploited its yETH token contract and drained millions in ETH and liquid staking assets from Balancer pools. The incident unfolded late on Nov. 30 when an attacker triggered…

The timing is awful. The breach occurred just hours after its parent company, Dunamu Inc., unveiled a massive $10.3 billion takeover by tech giant Naver Corp.

The timing is awful. The breach occurred just hours after its parent company, Dunamu Inc., unveiled a massive $10.3 billion takeover by tech giant Naver Corp.