Coinbase is reportedly preparing to launch its own prediction markets, powered by U.S.-based operator Kalshi, in a move that could expand the types of assets available on the exchange amid cooling investor interest in cryptocurrencies, according to reporting from Bloomberg and CNBC.

The announcement is expected to come next week, coinciding with Coinbase’s “Coinbase System Update” showcase on Dec. 17. While the exchange declined to confirm specifics, it encouraged users to tune into the livestream for updates.

Rumors of the new prediction markets have been circulating for nearly a month. In mid-November, tech researcher Jane Manchun Wong shared a screenshot of what appeared to be Coinbase’s prediction markets dashboard.

The Information first reported the planned launch on Nov. 19, and Bloomberg later cited a source saying the event would also feature the rollout of tokenized stocks.

Coinbase as an ‘everything’ exchange

Coinbase’s moves align with CEO Brian Armstrong’s long-stated vision of building an “everything exchange” — a single platform offering access to crypto tokens, tokenized equities, and event-based contracts.

Armstrong told investors in May that Coinbase aims to become a leading financial services app within the next decade.

The exchange is accelerating these initiatives amid rising competition from firms such as Robinhood, Gemini, and Kraken

Over the past year, these platforms have expanded tokenized stock offerings outside the U.S. and explored prediction markets, reflecting growing demand for alternative trading instruments.

The timing also comes as investor sentiment toward digital assets has cooled. A wave of liquidations in highly leveraged positions in mid-October triggered a crypto market pullback, prompting some investors to shift capital into safer assets.

For Kalshi, the partnership marks another step in its strategy to integrate event contracts into mainstream trading platforms.

Earlier this year, the company embedded its prediction markets into Robinhood, and it is reportedly in discussions with other brokers, including those in crypto, to expand its reach.

Prediction markets let users speculate on outcomes ranging from elections to sports games, and they have grown increasingly popular over the past year. Traditional exchanges and crypto platforms alike are now exploring them as a new way to engage traders.

Gemini recently received approval to roll out its own prediction markets, while Crypto.com has partnered with the Trump Media & Technology Group on similar initiatives.

Coinbase’s planned in-house tokenized stock offerings would put it on par with competitors like Robinhood and Kraken, which currently offer similar products outside the U.S.

The bitcoin price was trading in the $92,000 range earlier today but has now dropped back toward $90,000, reflecting continued volatility despite the U.S. Federal Reserve’s 25-basis-point rate cut.

After briefly spiking above $93,000 yesterday, the crypto fell below $90,000 and stabilized around $90,600 at the time of writing.

The pullback comes amid mixed signals from the Fed. While the rate cut to 3.50%–3.75% was widely anticipated, Fed Chair Jerome Powell’s cautious remarks and a 9–3 split among FOMC members — one favoring a deeper 50-basis-point cut and two opposing any reduction — tempered enthusiasm for risk assets, including BTC.

Analysts described the decline as a “sell the fact” reaction, since markets had already priced in the move.

On top of this, Vanguard Group has begun allowing clients to trade spot Bitcoin exchange-traded funds (ETFs), marking a notable expansion in access to crypto products for the $12 trillion asset manager’s investors.

Yet, Vanguard’s senior leadership emphasized that its fundamental view of BTC and other cryptocurrencies remains skeptical.

John Ameriks, Vanguard’s global head of quantitative equity, said Thursday at Bloomberg’s ETFs in Depth conference that Bitcoin is better seen as a speculative collectible than a productive asset.

Comparing it to a viral plush toy, Ameriks highlighted that BTC lacks income, compounding potential, and cash-flow generation — the core attributes Vanguard looks for in long-term investments.

“Absent clear evidence that the underlying technology delivers durable economic value, it’s difficult for me to think about Bitcoin as anything more than a digital Labubu,” he said, according to Bloomberg.

Despite this caution, Vanguard’s decision to allow trading of BTC ETFs on its platform was influenced by the growing track record of such products since the first BTC ETF launched in January 2024.

Ameriks said the firm wanted to ensure these ETFs accurately reflect their advertised holdings and perform as expected.

Banks engaging with bitcoin

Earlier this week, PNC Bank became the first major U.S. bank to offer direct spot bitcoin trading to eligible Private Bank clients through its digital platform, using Coinbase’s Crypto-as-a-Service infrastructure.

The launch follows a strategic partnership announced in July and reflects a growing trend among U.S. banks to integrate bitcoin into wealth management services.

Also last week, the Bank of America urged its wealth management clients to allocate 1% to 4% of their portfolios to digital assets, signaling a major shift in its approach to Bitcoin exposure.

As of today, Bitcoin is trading at approximately $90,115.85, with a circulating supply of nearly 19.96 million BTC and a market cap of $1.81 trillion.

Prices have fluctuated modestly over the past week, reflecting the broader market’s volatility.

The U.S. Office of the Comptroller of the Currency (OCC) has granted conditional approvals for five digital asset firms — Ripple, Circle, Fidelity Digital Assets, BitGo, and Paxos — to become federally chartered national trust banks, marking a major milestone in the integration of cryptocurrency into traditional finance.

Once finalized, these institutions will join roughly 60 other national trust banks regulated by the OCC, gaining the ability to offer fiduciary and custody services nationwide.

Unlike larger national banks, trust banks cannot accept cash deposits or make loans, but they can hold and manage customers’ digital assets.

‘Huge news’ for crypto

Circle, issuer of the $78 billion USDC stablecoin, said the charter would enhance the safety and regulatory oversight of its reserves while enabling fiduciary digital asset custody for institutional clients.

CEO Jeremy Allaire emphasized that the federal charter would provide “greater clarity and confidence” to institutions building on Circle’s platform as stablecoins gain mainstream adoption.

Paxos, known for PYUSD and the consortium-backed Global Dollar (USDG), said federal oversight would allow businesses to issue, custody, trade, and settle digital assets with clarity and confidence.

The firm, which has operated under a New York Department of Financial Services (NYDFS) charter since 2015, first applied for a federal charter in 2020.

BitGo, a South Dakota–based crypto custodian, said the federal charter would allow it to expand services nationwide, including trading, staking, stablecoin, and treasury offerings for institutions. BitGo has also filed to go public, reporting $4.19 billion in revenue for the first half of 2025, up from $1.12 billion during the same period in 2024.

The approvals reflect a broader trend toward federal oversight of digital assets, coming after Anchorage Digital became the first federally chartered crypto bank in the U.S. Other firms, including Coinbase, Bridge (owned by Stripe), and Crypto.com, have also applied for federal charters.

OCC Comptroller Jonathan V. Gould emphasized that new entrants into the federal banking sector benefit consumers, foster competition, and promote innovation.

“The OCC will continue to provide a path for both traditional and innovative approaches to financial services to ensure the federal banking system keeps pace with the evolution of finance and supports a modern economy,” Gould said.

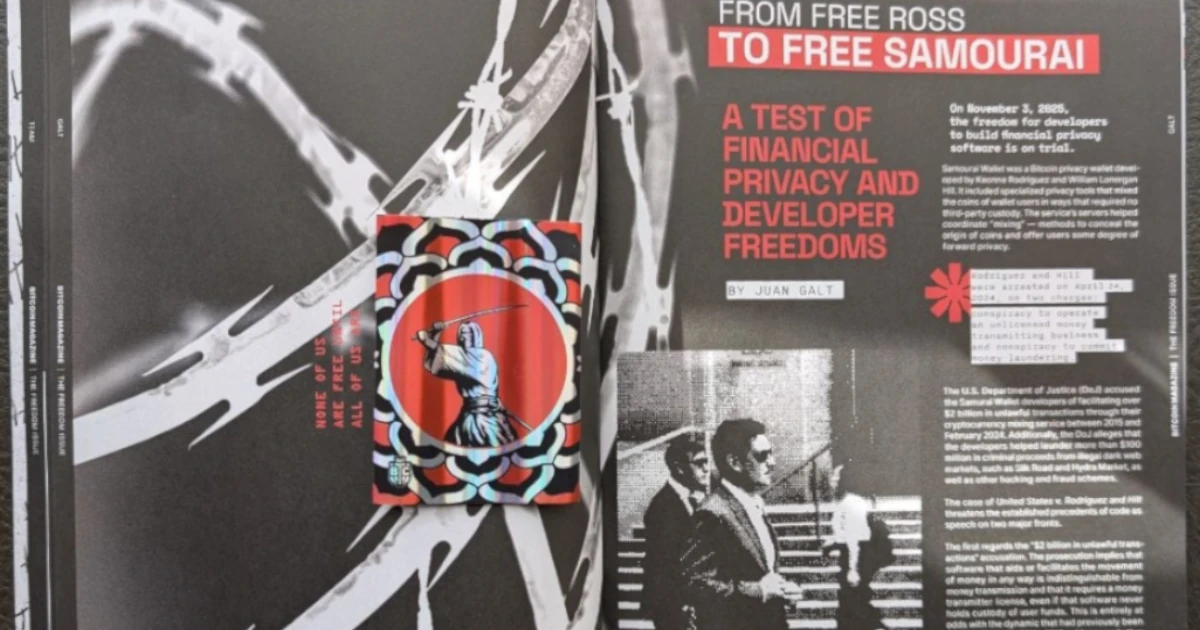

On December 18th, days before Christmas, Keonne Rodriguez, co-founder of the Bitcoin Samourai Wallet, will have to surrender to prison. His crime? Creating a software tool that gave Bitcoin users comparable privacy to that which banks are expected to provide. Samourai Wallet, the brand and technology stack built by Rodriguez and William Lonergan Hill, was shut down by the U.S. Government in April 2024 on a variety of charges, including money laundering, but only one charge stuck after a high-profile trial, the weakest charge of all, “unlicensed money transmission”.

What does it mean to transmit money? According to prosecutors, custodial control over user funds is no longer a requirement to need an MSB license; “a USB cable transfers data from one device to another, and a frying pan transfers heat from a stove to the contents of the pan, although neither situation involves exercising ‘control’ over what is being transferred.” If the DoJ can indict a frying pan, then USB manufacturers better lawyer up!

While I’m no genius, the Supreme Court has emphasized that laws should be clear enough for an AVERAGE PERSON to understand

Let’s get into the minutiae of the specific subsection of the charge they pled to

Remarkably, even FinCEN disagrees with the DoJ’s novel legal interpretation of what constitutes a money transmitter, as guidance at the time said non-custodial services could not be money transmitters because they do not exert control over money flows. FinCEN reasserted this fact to the DoJ prosecutors in a written statement, but they went forward with the charges anyway. This critical fact was withheld from the defense for almost a year, when it was finally revealed, “the judge denied the motion to present this evidence in the hearings, without even any argument,” according to Rodriguez. Critics argue this misconduct by the DoJ prosecutors is a violation of Brady v. Maryland, denying access to material that could have undermined the unlicensed money transmission charges, or, as Donald J. Trump would put it, this prosecution was rigged.

Zack Shapiro, head of policy at the Bitcoin Policy Institute, warns the Trump administration and American software industry about the potential ramifications of this legal case, arguing that “collapsing the distinction between developing a tool and operating a service would introduce an untenable level of risk for anyone building privacy-enhancing or security-critical software.”

“Rodriguez and Hill ultimately accepted plea agreements in the face of substantial sentencing exposure, even though government records undermined the central regulatory theory of the case,” Shapiro added in a letter published on the BPI website, asking the Trump admin to pardon the Samourai Wallet devs.

Fundamentally, the prosecutorial approach in the Samourai Wallet case risks establishing an influential precedent that threatens the financial privacy of American citizens and stifles innovation in the U.S. crypto industry. It could shape future prosecutions and regulatory developments, potentially reclassifying non-custodial services as money transmitters under federal law—requiring national MSB registration with FinCEN—and prompting stricter state-level licensing in jurisdictions like New York or California.

Echoing the trial against Ross Ulbricht a decade earlier, this rigged case against Samourai Wallet was set up during the Biden administration with support from anti-crypto politicians whom Trump defeated in the 2025 elections with the popular mandate. During his campaign at the 2024 Bitcoin Nashville speech, Trump said, “I will always defend the right to self-custody,” and got major support from the Bitcoin and crypto industries through the shared vision of making the United States the crypto capital of the world.

“I pledge to the Bitcoin community that the day I take the oath of office, Joe Biden and Kamala Harris’ anti-crypto crusade will be over,” – Donald J. Trump, Nashville 2024.

David Sacks, the venture capitalist and White House A.I. & Crypto Czar, should also pay attention to this issue; otherwise, what does it even mean to be the Crypto Czar? If Bitcoin wallets end up regulated the same as banks, despite having no counterparty risk, then whose interests are really being served, Mainstreet’s or Wallstreet’s?

While the Trump admin has been very conservative during the DoJ’s prosecution and trial of the Samourai Wallet devs — and perhaps, understandably so — that stage of the legal battle is over.

It is time for the Trump administration to meet its promise to the American public and defend self-custody and the crypto industry in America. It is time for Trump to set the record straight and pardon Keonne Rodriguez and William Lonergan Hill, as well as the Tornado Cash devs, while we are at it, lest we have another Ross Ulbricht-style miscarriage of justice.

The Bitcoin and crypto industry is well behind this effort and has begun gathering signatures at Change.org, totaling over 5000 so far and growing, with the only official fundraising campaign at GiveSendGo.

Should Trump pardon the Samourai Wallet devs, he would be sending a clear signal to those who want surveillance-based, central bank digital currency systems to enslave Americans and the world that Americans will not stand for it. That the United States stands with the fundamental human right to privacy, dignity, due process, and the presumption of innocence, and not the tactics of intimidation developed by the likes of Joseph Gorbles, where privacy is a crime. Mass, indiscriminate surveillance, without a warrant, without due process, that is the real crime.

Sangha Renewables announced the energization of its 19.9-megawatt bitcoin mining facility in Ector County, West Texas today, in partnership with Links Genco and TotalEnergies.

The project operates behind-the-meter on a 150-megawatt solar farm, combining renewable energy generation with digital infrastructure to explore new revenue streams for the energy sector.

The facility, developed with support from Links Genco, uses bitcoin mining to provide dispatchable industrial demand that aligns with variable renewable output.

Links Genco provided energy structuring and grid compliance services, helping Sangha configure a load profile that complements solar generation while mitigating exposure to transmission constraints and local curtailment, according to a note shared with Bitcoin Magazine.

Back in May, Sangha broke ground on the bitcoin mining facility. The project, developed with an independent power producer, now known as TotalEnergies, was built on an existing solar site in efforts to turn underutilized renewable assets into profitable bitcoin-generating operations.

The opening was marked by a ribbon-cutting ceremony that just wrapped up in West Texas. The event brought together company representatives, local officials, and industry partners, including Links Genco and TotalEnergies.

Under the project agreement, Sangha will own and operate the mining data center, deploy high-efficiency hardware, and manage the load to maximize utilization during periods of excess solar generation.

TotalEnergies will supply comprehensive retail power solutions, including balancing services, supplemental grid power during non-solar hours, and structured energy products designed to address price volatility while maintaining operational reliability.

By situating the mining facility at the point of generation, Sangha is trying to capture value that may otherwise be lost in areas with transmission congestion.

Bitcoin mining as a means for new energy value streams

The approach also offers a framework for scalable, location-agnostic load, potentially providing additional revenue streams for renewable energy producers and supporting broader grid stability.

“This project highlights how bitcoin mining can become a tool to unlock new value streams for the energy sector,” said Spencer Marr, co-founder and president of Sangha Renewables.

Marr emphasized that partnerships with energy providers like TotalEnergies demonstrate how digital infrastructure can be integrated into long-term energy planning.

Simon Binet, vice president of Trading U.S. Gas & Power at TotalEnergies, described the arrangement as aligned with the company’s goals to provide innovative energy solutions that support decarbonization efforts in energy-intensive industries.

The ribbon-cutting ceremony included opening remarks from Sangha Renewables, Links Genco, and Judge Dustin Fawcett of Ector County, followed by a guided tour of the mining facility, press interviews, and a photoshoot.

Pakistan is moving to formalize its place in the global digital-asset economy, signing a memorandum of understanding with Binance to explore the tokenization of up to $2 billion in state-owned assets while granting early regulatory clearances to both Binance and HTX.

Together, the initiatives reflect one of the country’s most ambitious pushes yet to merge sovereign finance with blockchain-based infrastructure.

According to Pakistan’s finance ministry, the MoU with Binance will allow the government to assess tokenising sovereign bonds, treasury bills, and commodity reserves — including oil, gas, and metals — as it seeks new tools to boost liquidity and expand market reach.

Tokenization would create digital representations of real-world assets on blockchain networks, potentially widening investor access and supporting secondary-market efficiency.

JUST IN: Binance founder CZ met with Pakistan’s Finance Minister and Minister of State.

Finance Minister Muhammad Aurangzeb described the agreement as a signal of Pakistan’s reform trajectory and a step toward a “long-term partnership” aimed at drawing global participation into the country’s debt and commodity markets, according to Reuters.

Binance founder Changpeng “CZ” Zhao called the MoU an important marker for both Pakistan and the broader blockchain sector, suggesting it clears the way for deeper experimentation with digital asset rails at the sovereign level.

Pakistan is embracing bitcoin and crypto

The tokenisation initiative comes in parallel with a regulatory milestone. Pakistan’s newly formed Virtual Assets Regulatory Authority (PVARA) has issued No Objection Certificates (NOCs) to Binance and HTX after a multi-agency review of each exchange’s governance, compliance, and risk-management systems.

The NOCs allow both firms to register with the Financial Monitoring Unit’s goAML platform, begin local incorporation, and prepare full license applications once the country finalizes its virtual-asset framework.

PVARA emphasized that the early clearances are not operating licenses but the first step in a phased, FATF-aligned path toward full authorization.

“Strong governance, AML and CFT compliance remain central as Pakistan builds a trusted digital-asset ecosystem,” the regulator said. Chair Bilal bin Saqib added that compliance rigor—not size—will determine which exchanges advance through the licensing process.

The developments are part of a broader digital-finance overhaul that the country has compressed into a few months.

That includes establishing PVARA, forming the Pakistan Crypto Council (PCC), drafting licensing and taxation rules, and laying groundwork for a central bank digital currency pilot in 2025.

The country has also signed a letter of intent with U.S.-based World Liberty Financial to explore stablecoin infrastructure and tokenised financial rails.

Saqib’s thoughts at Bitcoin MENA

Saqib, who serves as minister of state for digital assets, has repeatedly argued that Pakistan must treat Bitcoin, tokenization, and blockchain as foundational elements of future financial architecture.

At the Bitcoin MENA conference, Saqib argued that bitcoin serves as a practical tool for millions of Pakistanis rather than a speculative bet.

His case was grounded in everyday economic realities. With the Pakistani rupee losing more than half its value in five years, he said people aren’t seeking lessons in monetary theory — they’re looking for protection.

For many, “bitcoin is not theory, it’s a relief,” offering a hedge against inflation driven by political decisions and chronic currency mismanagement.

Access is the other major issue. Pakistan has a population of about 240 million, yet more than 100 million people remain unbanked. In that context, Bin Saqib said bitcoin provides a pathway to basic financial services that the traditional system has failed to deliver.

At a fireside chat, Saqib tied these grassroots use cases to a broader national strategy. Pakistan, he said, is not trying to “chase the future” but to build a new one. With roughly 70% of the population under the age of 30, the country cannot rely on outdated economic models.

Saqib said Bitcoin and blockchain-based payment rails enable Pakistani workers to get paid globally without friction, delays or excessive fees. Digital assets, and bitcoin in particular, are being viewed as infrastructure rather than speculation — new financial rails for the Global South.

The Bitcoin Magazine Pro Price Forecast Tools chart provides a comprehensive framework for identifying potential price floors during bear cycles and forecasting upside targets based on on-chain fundamentals and network-derived data points. By aggregating multiple metrics, this methodology has historically called Bitcoin market cycle peaks and bottoms with remarkable accuracy. Can these tools continue to provide a basis for reliable BTC price forecasting over the next 12 months and beyond?

The Cumulative Value Days Destroyed (CVDD) metric has historically called Bitcoin price cycle lows almost to perfection across every cycle since Bitcoin’s inception. This metric begins with Coin Days Destroyed, a measure that weights Bitcoin transfers by the duration they were held before movement. For example, holding 1 Bitcoin for 100 days produces 100 coin days destroyed when transferred, while holding 0.1 Bitcoin for the same result requires 1,000 days of holding. Large spikes indicate that the network’s most experienced long-term holders are transferring significant amounts of Bitcoin.

Figure 1: The convergence of the CVDD and Balanced Price with BTC price has historically aligned with bear market lows.View Live Chart

The CVDD takes this one step further by measuring the USD valuation at the time of transfer rather than just the coin days destroyed quantity alone. This value is then multiplied by 6 million to produce the final metric. When examined across Bitcoin’s entire history, the CVDD has indicated bear market lows with accuracy extending across every cycle. Currently, the CVDD sits at approximately $45,000, though this level trends upward over time as the metric naturally evolves with new transfers and Bitcoin’s price appreciation.

The Balanced Price metric complements this downside projection by subtracting the Transferred Price (its calculation methodology is explained later) from the Realized Price, the cost basis or average accumulation price for all bitcoin holders, providing another historically accurate bear cycle low signal.

The Top Cap metric begins with the all-time average cap, the cumulative sum of Bitcoin’s market capitalisation divided by the number of days Bitcoin has existed. This all-time weighted moving average is then multiplied by 35 to produce the Top Cap. Historically, this metric has been remarkably accurate for calling bull market peaks, though in recent cycles it has exceeded actual price action, currently projecting to a seemingly unattainable ~$620,000.

The Delta Top refines this approach by using the realized cap. The realized cap currently stands at approximately $1.1 trillion. Delta Top is calculated by subtracting the average cap from the realized cap and multiplying by 7. This metric has been accurate historically, though it was slightly off during the 2021 cycle, and it is looking more likely that it will not be reached in the current cycle, currently sitting at approximately $270,000.

Figure 2: Delta Top and Terminal Price metrics have frequently aligned with market tops.View Live Chart

The Terminal Price metric provides another layer of sophistication. It calculates the Transferred Price, the sum of Coin Days Destroyed divided by the Circulating Bitcoin Supply, and multiplies this by 21 (the maximum Bitcoin supply). This produces a price level based on the fundamental assumption of total network value distributed across all 21 million Bitcoins. Historically, the Terminal Price has been one of the most accurate top-calling tools, marking previous cycle peaks nearly to perfection. This metric currently sits at approximately $290,000, not too far above Delta Top’s current value.

Bitcoin Cycle Master: Aggregated Bitcoin Price Fair Value Framework

Integrating all these individual metrics into a unified framework produces the Bitcoin Cycle Master chart, which combines these on-chain forecast tools for confluence. This has helped to identify where Bitcoin may be in a cycle, either close to bull or bear market highs, or oscillating around its ‘Fair Market Value’.

Figure 3: The Bitcoin Cycle Master currently indicates a Fair Market Value of approximately $106,000.View Live Chart

Examining the past two cycles demonstrates the utility of this framework. When Bitcoin trades above the Fair Market Value band, bull markets have historically entered exponential growth phases. When beneath this band, Bitcoin typically signals bear market conditions where defensive positioning and aggressive accumulation become appropriate strategies.

By extracting raw data from the price forecast tools and projecting the slope of both the CVDD and Terminal Price forward to the end of 2026, two scenarios emerge. The CVDD, which has moved at a predictable rate of change over the past 90 days, projects to approximately $80,000 by December 31, 2026. This level could represent a potential bear cycle floor, though Bitcoin has already traded beneath this level during recent downward moves, suggesting current prices may already offer compelling value.

Figure 4: Extrapolating the CVDD and Terminal Price metrics across 2026 provides a considerable range for potential BTC price action.

The Terminal Price, extrapolating its current upward trend, could reach over $500,000 by the end of 2026, though this projection could only be a realistic outcome with a bullish macro environment with significant liquidity injections and broad realization of Bitcoin’s fundamental value proposition.

Conclusion: What Bitcoin Price Forecast Tools Are Signaling for 2025–2026

These Bitcoin price forecast tools, formulated using on-chain fundamental and network-derived data points rather than psychological levels or traditional technical analysis applicable to equities and commodities, have historically provided exceptional accuracy in calling market cycle peaks and bottoms. Forecasting based on their current values suggests a potential bear cycle floor in the $80,000 range by the end of 2026, with upside targets potentially reaching over $500,000, depending on macro conditions and capital flows.

While these projections represent extrapolations of current trends rather than certainties, the historical accuracy and on-chain foundation of these metrics warrant serious consideration. Investors and traders should continue monitoring both the raw price forecast tools and the aggregated Bitcoin Cycle Master framework to identify fair valuation levels, extreme overvaluation warnings, and attractive accumulation zones within the current cycle. However, all projections change daily as new data emerges, making reactive analysis superior to long-term prediction.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always do your own research before making any investment decisions.

A major rule change is being considered by MSCI, one of the most influential index providers in global markets. If adopted, it would materially alter how public companies that hold digital assets—particularly Bitcoin—are classified and included in major equity indexes.

For companies, investors, asset managers, and anyone who depends on index-based benchmarks, this proposal raises fundamental questions about how markets define operating businesses and what role balance sheets should play in index eligibility.

Join the call for MSCI to withdraw its digital asset exclusion rule.

Here’s what’s at stake—and why it matters.

1. MSCI Is Proposing a New 50% Balance-Sheet Threshold

At the center of the proposal is a simple rule:

If digital assets make up 50% or more of a company’s total assets, that company would be excluded from MSCI’s Global Investable Market Indexes.

MSCI’s rationale is that crossing this threshold allegedly changes the company’s “primary business,” making it more fund-like rather than operational.

This single ratio would override all other indicators of what the company actually does.

2. The Proposal Misclassifies Operating Companies as Investment Funds

The core objection is straightforward: holding Bitcoin on a balance sheet does not transform an operating company into an investment fund.

Operating companies generate revenue from products and services

They employ people, invest in R&D, and serve customers

Treasury assets exist to support long-term capital strategy

By contrast, investment funds exist solely to manage portfolios for return.

Treating these two structures as equivalent—based on a balance-sheet ratio alone—collapses a distinction that has long been foundational to corporate and securities law.

If your organization relies on clear, fundamentals-based definitions of operating companies, this misclassification matters. Bitcoin For Corporations is asking MSCI to withdraw the proposal and engage on a more principled framework. You can add your name to the open letter here.

3. Treasury Strategy Does Not Redefine Core Business Activity

A company can change how it stores excess capital without changing what it does.

A manufacturer that holds cash remains a manufacturer

A software firm holding foreign currency remains a software firm

A company holding Bitcoin as treasury reserve remains an operating company

Treasury allocation is a capital management decision, not a change in business model.

4. This Would Be a Radical Departure From Decades of Index Practice

Historically, index classification has been driven by operational reality, not asset composition alone.

Primary business determination has relied on:

Revenue sources

Earnings contribution

Ongoing commercial activity

This proposal replaces that holistic approach with a single market-price-driven metric on the asset side of the balance sheet—something never applied consistently across asset classes before.

5. Digital Assets Are Being Singled Out—Uniquely

Under the proposal:

A company with 51% of assets in Bitcoin → excluded

A company with 51% in real estate → included

A company with 51% in equities or commodities → included

No equivalent rule exists for other treasury assets.

This lack of neutrality directly conflicts with the principles that global indexes are supposed to uphold.

6. The Proposal Conflicts With Core Index Principles

MSCI’s benchmarks are built on three foundational ideas:

Neutrality – no asset-class favoritism

Representativeness – reflecting real economic activity

Stability – avoiding unnecessary churn

A rule that reclassifies companies based on volatile market prices undermines all three.

7. The Rule Would Introduce Structural Instability Into Indexes

Consider a company with:

45% of assets in digital form → eligible

No operational change

Normal market appreciation pushes it to 51%

Under the proposal, that company would suddenly be excluded—despite:

No change in revenue

No change in operations

No change in business strategy

This creates a scenario where companies could flip in and out of indexes purely due to price movement, forcing unnecessary rebalancing, costs, and tracking error for index-linked funds.

This kind of mechanical instability would impose real costs on index-tracking funds, issuers, and long-term investors—without improving market clarity. That’s why companies and market participants are urging MSCI to withdraw the proposal and revisit it with industry input. Join the call for MSCI to withdraw this rule proposal, and add your signature to the open letter here.

8. A More Robust Alternative Already Exists

The issue is not classification—it’s how classification is done.

A principles-based, multi-factor framework would evaluate:

Revenue and earnings mix

Legal and regulatory status

Core corporate activities (employees, R&D, capex)

Public disclosures and stated strategy

This approach reflects the entire business, not a single fluctuating ratio.

9. The Coalition’s Ask Is Clear and Constructive

Market participants are calling for a two-step solution:

Withdraw the current proposal due to its structural flaws

Engage with the market to develop a neutral, principles-based framework that preserves index integrity

The goal is not special treatment—but consistent treatment aligned with long-standing market norms.

Why This Matters

Indexes are not academic exercises. They:

Guide trillions of dollars in capital allocation

Shape passive investment flows

Influence cost of capital for public companies

If index rules become arbitrary, unstable, or asset-specific, they stop reflecting the real economy—and start distorting it.

Final Thought

If your organization depends on fundamentals-based equity benchmarks, this proposal affects you—whether or not you hold digital assets today.

Indexes only work when they remain neutral, stable, and grounded in operating reality. Market participants are asking MSCI to withdraw the proposed digital asset rule and work toward a principles-based alternative.If you or your organization depend on fair and consistent equity benchmarks, adding your signature to the open letter helps ensure those standards are preserved.

Index integrity relies on clear principles, not price-driven thresholds.

Engagement now helps ensure global benchmarks remain neutral, stable, and representative for everyone who relies on them.

Disclaimer: This content was prepared on behalf of Bitcoin For Corporations for informational purposes only. It reflects the author’s own analysis and opinion and should not be relied upon as investment advice. Nothing in this article constitutes an offer, invitation, or solicitation to purchase, sell, or subscribe for any security or financial product.

Bitcoin is no longer just a grassroots monetary revolution. It’s in the process of moving from the periphery of finance into its centre. The rise of Bitcoin treasury companies is a major force behind this shift. These are firms that accumulate bitcoin not as a side bet, but as a core balance sheet holding. In doing so, they provide access to capital markets, offer yield-bearing instruments, and reshape how companies think about monetary preservation.

This article explores what Bitcoin treasury companies are, how they operate, and why their emergence matters, for both corporate finance and Bitcoin’s long-term trajectory.

Key Takeaways

Bitcoin treasury companies hold bitcoin as a long-term treasury reserve, often replacing fiat cash or short-term bonds.

These companies expand bitcoin’s investable capital base by enabling access through public equity or corporate debt.

Public treasury firms may trade at a premium to their bitcoin holdings due to market access, regulatory arbitrage, and capital efficiency.

Some companies issue bitcoin-backed financial products such as yield notes or strategic reserves.

What is a Treasury Company?

A Bitcoin treasury company business model, whereby a business integrates bitcoin into its treasury management framework. This approach prioritizes monetary certainty over fiat liquidity. The company treats bitcoin as a base-layer reserve asset superior to sovereign currency, rather than a hedge or speculative position.

Treasury companies may be public or private. Public companies often use their regulatory status to issue stock or debt, which is then converted into bitcoin. Private firms generally rely on retained earnings. Regardless of structure, the key factor is that bitcoin becomes the foundation of the corporate treasury, not a side asset.

These companies use bitcoin to manage long-term purchasing power, defend against monetary debasement, and unlock investor access in regions or structures where direct exposure is restricted. The treasury strategy shapes their business identity and capital allocation, often attracting shareholders who value monetary independence.

For a deeper look at the three operating models—pure play, hybrid operator, and strategic holder—see this breakdown from Michael Saylor.

What Purpose Does It Serve?

Bitcoin treasury companies restructure their balance sheets to reflect a predictable monetary strategy championing absolute scarcity over fiat stability. Holding bitcoin allows them to escape the inflationary decay of sovereign currency while signaling long-term capital discipline.

The strategy serves two core purposes:

it defends shareholder value by shifting reserves into a scarce, non-counterparty asset.

it creates financial access for investors who cannot hold bitcoin directly. Through their equity or debt instruments, treasury companies channel restricted capital into the Bitcoin ecosystem.

These firms also develop financial products around their holdings. Bitcoin-backed notes, interest-bearing instruments, and convertible structures create yield opportunities. In these cases, the treasury company acts as a financial services platform as well as a capital allocator.

Expanding Bitcoin’s Capital Base

Bitcoin treasury companies serve as access points to the asset for capital that would otherwise remain on the sidelines. As Steven Lubka put it, they are “fundamentally expanding the amount of capital that can flow into bitcoin… They are not competing for the same pool of dollars; they are making the pool larger.”

Most institutional allocators are still trapped inside structures that prohibit direct bitcoin exposure. Their mandates require them to hold equities, bonds, or fund shares—not bearer assets. Treasury companies bypass that restriction. By holding bitcoin and offering tradable equity or fixed income products, they act as financial bridges that translate bitcoin exposure into forms institutions can legally hold.

This approach allows adoption to scale without waiting for regulatory charters or compliance approval. This is infrastructure that routes around the choke points.

Mechanics: How It Works

While each company operates within its own legal, regulatory, and financial constraints, most follow a similar operational structure. The details may vary, but the following components form the backbone of how they operate.

Acquisition – The company acquires bitcoin using excess cash or proceeds from capital raises. This is typically done through over-the-counter (OTC) trading desks or institutional-grade exchanges. Some firms that operate in the mining space may allocate mined bitcoin directly to treasury, removing market exposure altogether.

Custody – Firms must decide between self-custody and third-party custodians. Institutional custodians like Fidelity Digital Assets, Anchorage, or Coinbase Custody offer compliance and insurance options, while self-custody provides sovereignty at the cost of internal security complexity. Custody decisions affect not just risk, but also regulatory posture.

Accounting – Under current US GAAP rules, bitcoin is classified as an intangible asset. Impairments are recognized if market value drops below the acquisition cost, but gains are not recorded unless realized through a sale. This creates an asymmetric treatment that can distort quarterly earnings and force conservative reporting, even if treasury value increases.

Reporting – Public treasury companies are required to disclose bitcoin holdings and changes in treasury structure through filings, earnings reports, and shareholder updates. Some choose to go further, publishing regular updates or dedicating resources to explaining their bitcoin strategy in detail.

Security – Private key management is without question, a critical part of the operation. Companies typically use multisignature wallets, geographic key separation, cold storage, and internal controls to secure holdings. Firms with large positions may employ Shamir’s Secret Sharing or multiple independent signers to ensure redundancy and resilience.

Governance – Policies must define how bitcoin is acquired, secured, and reported. This includes buy thresholds, custody control frameworks, access rights, key management protocols, and recovery plans. Strong governance ensures the strategy survives beyond the initial executive vision and becomes embedded in company operations.

Bitcoin treasury companies operate within a regulatory environment where public firms enjoy broader access to capital markets than individuals or funds. This creates a structural advantage. A public company can issue equity or debt, raise fiat capital efficiently, and convert it to bitcoin. In contrast, many institutional investors face custodial, legal, or charter-based constraints that prevent them from holding bitcoin directly.

This dynamic creates a form of regulatory arbitrage. The company acts as a wrapper for bitcoin exposure, allowing capital to enter the market through familiar financial instruments like stocks and bonds. Investors gain indirect access to bitcoin, often through vehicles they are already authorized to hold.

This mechanism is similar to financial innovations of the past. In the 1980s, Salomon Brothers restructured the bond market by slicing and repackaging fixed-income assets to match investor demand. Other sectors used wrappers to route capital around institutional constraints. Bitcoin treasury companies apply the same principle: they turn capital markets into a funnel and aim it at a harder monetary asset.

Regulatory Arbitrage: Why These Companies Even Exist

Bitcoin treasury companies operate in a unique zone of regulatory asymmetry. As Lubka notes on p39, of issue 39 of Bitcoin Magazine, “What bitcoin treasury companies are doing is engaging in regulatory arbitrage.”

Public companies can access large pools of capital through stock and debt issuance. They can then deploy that capital into bitcoin. Retail investors, pension funds, and even many hedge funds cannot hold bitcoin directly—but they can buy shares in public companies.

This is not a technicality. It’s a structural end-run around the gatekeepers of capital. While a retirement fund can’t buy spot bitcoin, it can buy shares in a firm like MicroStrategy. That dynamic turns treasury companies into Trojan horses—pulling bitcoin exposure into portfolios that would otherwise be prohibited from touching it.

Background and Origins

The treasury model gained serious traction in August 2020, when MicroStrategy ($MSTR) allocated $250 million of its reserves to bitcoin. CEO Michael Saylor framed the move as a rational response to fiat debasement and falling real yields. The firm continued raising capital through debt and equity issuance to expand its position, ultimately acquiring over 650,000 BTC.

Other public companies followed. Tahini’s began stacking bitcoin a mere days after MicroStrategy. Tesla ($TSLA) added $1.5 billion in bitcoin to its treasury in early 2021. Square ($SQ), now Block, also made an allocation, citing long-term purchasing power as the key motivation. These high-profile moves signaled that bitcoin was gaining legitimacy as a treasury reserve among large-cap firms.

To support institutional adoption, MicroStrategy, in partnership with BTC Inc launched Bitcoin for Corporations, an annual event aimed at guiding CFOs, legal teams, and boards through the process of integrating bitcoin into treasury strategy. The event helped normalize bitcoin discussions inside traditional corporate structures.

A major barrier to adoption—accounting treatment—began to shift in 2023. The FASB approved new rules allowing companies to report bitcoin holdings at fair market value. This replaced the outdated impairment model and removed one of the most cited objections among public company CFOs. The change went into effect in 2025.

MicroStrategy ($MSTR) is the most established treasury company in the market. It has redefined its corporate identity around bitcoin accumulation and capital efficiency. The company has raised billions through convertible notes and direct equity issuance, with proceeds allocated to bitcoin. Shareholders now view the firm as a long-term access vehicle to bitcoin’s monetary appreciation.

MetaPlanet ($3350.T) is a Japanese firm that executes a similar game plan to Strategy. Operating within Japan’s distinct regulatory environment, it adapts the treasury playbook to fit regional constraints. MetaPlanet illustrates how treasury adoption can be localized without losing strategic focus.

Smarter Web Company ($MCP), based in the UAE, blends infrastructure development with bitcoin accumulation. Its jurisdiction allows more flexibility in treasury construction, enabling a hybrid model that integrates operational revenue with bitcoin reserves.

Nakamoto Holdings ($NAKA), a subsidiary of KindlyMD, has built a vertically integrated treasury strategy that includes internal capital management and structured products. The firm was profiled by Steven Lubka as an example of how smaller organizations can implement bitcoin treasury models with institutional rigor.

Evaluating a Treasury Company and Measuring Success

The success of a bitcoin treasury company depends on more than just the size of its holdings. Investors should evaluate how efficiently the company acquires bitcoin, whether it increases bitcoin per share over time, and how effectively it monetizes its position.

A key metric is mNAV, or multiple of net asset value. This measures the company’s market capitalization relative to its bitcoin holdings. A high mNAV suggests that the market values not just the bitcoin, but also the company’s capital efficiency, access, and ability to grow its holdings faster than the open market.

Companies that compound bitcoin holdings through accretive financing deserve to trade at a premium. This premium reflects future expectations of value creation. However, poorly managed firms can destroy per-share bitcoin by issuing too much equity or overpaying for marginal gains.

Evaluating treasury companies requires examining their capital structure, acquisition timing, product issuance, and accounting treatment.

Bitcoin treasury companies operate within a set of structural risks that are distinct from simple asset volatility. These risks are operational, regulatory, reputational and political. There’s also a fifth opposing risk, which is the risk of not holding or having exposure to bitcoin at all.

Operational Risk

Managing a bitcoin treasury introduces technical and procedural risks. Custody is not a service you can outsource without trust tradeoffs, and self-custody requires enterprise-grade key management practices. Multisignature configurations, geographic key separation, internal access controls, and incident recovery protocols must be implemented with precision. Any compromise in key security, whether from internal error or external attack, can result in unrecoverable losses. For companies holding hundreds of millions or billions in bitcoin, this becomes a single point of existential failure.

Regulatory Risk

Bitcoin exists outside the traditional financial system, and many jurisdictions still lack a clear legal framework for its treatment. Treasury companies must navigate unclear tax rules, evolving securities classifications, cross-border restrictions, and ambiguous corporate governance expectations. Regulatory risk is amplified for public companies, which face additional scrutiny from auditors, exchanges, and shareholders. In many regions, bitcoin remains classified as a speculative asset, limiting how it can be reported or deployed within treasury operations.

Reputational Risk

Corporate media, ESG pressure groups, and risk-averse investors typically view bitcoin adoption as speculative or irresponsible, especially during periods of price drawdown. Even competent treasury execution can be framed as reckless if narrative conditions turn. Leadership teams must be prepared to defend the strategy publicly and educate stakeholders who may not yet grasp the long-term monetary thesis.

Political Risk

One of the most insidious risks facing treasury companies is the growing institutional pushback from legacy finance. In 2025, MSCI, BlackRock, and Goldman Sachs’ Datonomy index excluded MicroStrategy and Coinbase from digital asset classifications, despite bitcoin representing a majority of their balance sheet exposure.

These companies were strategically removed because their alignment with bitcoin poses a structural threat to the existing banking order. Their inclusion in major indexes would legitimize bitcoin as a competing monetary system and weaken the financial establishment’s control over capital allocation.

This index engineering reduces investor access and protects legacy institutions. It is designed to suppress entities that store capital in an asset that cannot be debased, seized, or rehypothecated.

Monetary Risk of Not Holding Bitcoin

A more widespread risk facing corporate treasuries is the cost of continuing to rely on fiat-based strategies. Inflation erodes capital over time by reducing purchasing power. Treasury strategies that depend on short-term government bonds or bank deposits are exposed to monetary policy decisions that guarantee devaluation over time. Choosing to avoid bitcoin leads to long-term capital deterioration and the progressive weakening of the balance sheet. For companies that operate in inflation-prone environments or that sit on large fiat reserves, this becomes structural loss.

Holding cash yields nothing. The U.S. M2 money supply has grown by more than 7 percent annually since 1971, with recent years far exceeding that rate. A company holding idle dollars is losing 7 percent of purchasing power each year.

U.S. Treasuries yield between 1 and 3 percent in most cycles. Compared to 7 percent monetary expansion, this results in a real loss of 4 to 6 percent per year. These figures may widen as governments and central banks continue expanding credit to support growing debt obligations.

Stock buybacks are often framed as shareholder-friendly but rely on equity valuations inflated by the same monetary expansion that devalues cash. Once the capital is spent, it cannot be reallocated or used to defend the balance sheet. Buybacks might boost earnings per share but do nothing to preserve long-term monetary value.

Bitcoin provides a structurally different outcome. It has no issuer, no credit risk, and a fixed supply of 21 million. It is the only asset that has consistently outpaced M2 expansion over time. Michael Saylor projects a 29 percent annual return over the next 20 years. If that projection proves accurate, a modest allocation to a bitcoin treasury could fully offset fiat debasement.

As little as 2 percent in bitcoin may be enough to break even in real terms. With regular rebalancing, an allocation between 5 and 30 percent could preserve or grow purchasing power while still maintaining fiat liquidity. This is a strategic hedge against fiat decay and should be evaluated as a treasury defense mechanism, not a speculative bet.

Bitcoin ETF – A regulated investment product that tracks the price of bitcoin. ETFs offer simplicity but no direct control over bitcoin custody or strategic usage.

Bitcoin Strategic Reserve – A deliberate long-term allocation of bitcoin used to defend against fiat dilution and preserve capital over time. Treasury companies typically build this into their core strategy.

Further Reading

For readers looking to explore this topic in greater depth, two standout resources offer high-signal material:

BitcoinForCorporations.com – A curated collection of articles, videos, and resources tailored for executive teams, CFOs, and corporate strategists evaluating bitcoin treasury models.

Bitcoin treasury companies do more than store reserves in a the worlds best money. They restructure balance sheets around monetary certainty, offer regulated access to bitcoin, and create financial instruments anchored to absolute scarcity.

As inflation accelerates and fiat-based finance becomes more unstable, treasury companies may become lifeboats for capital seeking long-term preservation.

The Commodity Futures Trading Commission (CFTC) is rolling back legacy policy on digital assets, marking another step in its reorientation toward regulated crypto markets.

Acting CFTC Chairman Caroline D. Pham said the agency is withdrawing its years-old guidance on the “actual delivery” of virtual currencies, a document that had shaped how firms could custody and settle digital asset transactions since 2020.

The decision clears a path for new guidance that reflects the rise of tokenized markets, recent legislation and the CFTC’s growing oversight of spot crypto trading.

“Eliminating outdated and overly complex guidance that penalizes the crypto industry and stifles innovation is exactly what the Administration has set out to do this year,” Pham said.

Pham added that the move shows the agency can protect U.S. traders while supporting broader access to regulated markets.

The withdrawn advisory outlined the conditions under which virtual currency could be considered “delivered” in retail commodity transactions. The framework was drafted in an era when regulated digital asset infrastructure was limited and focused on Bitcoin custody and settlement.

Since then, Congress passed the GENIUS Act, the CFTC opened the door to regulated spot trading, and tokenization has become a core focus across major financial institutions. Staff now views the 2020 advisory as out of step with current market realities.

The withdrawal also advances the CFTC’s effort to implement recommendations from the President’s Working Group on Digital Asset Markets.

The CFTC’s broader crypto policy turn

The announcement builds on a series of steps taken in early December that signal an effort to bring crypto activity onshore and under federal supervision.

Earlier this month, the agency launched a pilot program that permits Bitcoin and other crypto to serve as collateral in regulated derivatives markets. The program includes detailed reporting and risk-management requirements for futures commission merchants, along with updated guidance on how tokenized assets fit within existing CFTC rules.

Under the pilot, firms must submit weekly reports that itemize the digital assets held in customer accounts and notify regulators of any material incidents tied to tokenized collateral.

The structure is meant to provide the CFTC with visibility into operational and custody risks while firms test the use of crypto in margin accounts.

The agency also issued a no-action position for FCMs that accept non-securities digital assets, including payment stablecoins, clarifying how capital and segregation requirements apply. At the same time, staff withdrew restrictions from 2020 that had limited the use of digital assets as collateral.

CFTC’s guidance with U.S. spot crypto markets

The CFTC also approved federally regulated spot Bitcoin and crypto trading for the first time. Bitnomial, a U.S. derivatives platform, will begin offering spot, perpetuals, futures and options on a single exchange under full CFTC supervision next week.

The exchange’s structure supports unified margin and net settlement across product types, reducing redundant collateral requirements for traders.

Pham said the expansion of spot trading under CFTC oversight offers U.S. traders a secure alternative to offshore venues and creates an environment where domestic firms can operate without state-by-state uncertainty.

The agency’s shift extends beyond trading. Polymarket, a crypto-based prediction market, secured approval to relaunch in the U.S. after upgrading its compliance systems and acquiring a registered platform.

The CFTC has said its broader goal is to strengthen oversight of digital markets without blocking the adoption of new technology.

In other news, the CFTC has approved Gemini’s application for a Designated Contract Market license, clearing the way for the exchange to launch a prediction market and potentially expand into crypto futures, options, and perpetual swaps.

Gemini first applied for the license in 2020, well before the recent surge of interest in prediction markets and platforms.

The bitcoin price fell on Wednesday night into Thursday, even after the U.S. Federal Reserve lowered interest rates, as Fed Chair Jerome Powell signaled a cautious approach heading into 2026.

On Wednesday, the Fed cut its benchmark rate by 25 basis points to 3.50%–3.75%, a move widely expected by markets. However, the 9–3 split among Federal Open Market Committee (FOMC) members and Powell’s hawkish remarks during the press conference tempered investor enthusiasm for risk assets, including cryptocurrencies.

One official favored a deeper 50-basis-point cut, while two voted against any reduction.

The Bitcoin price briefly jumped over $94,000 but then dropped below $90,000 and stabilized around $89,730 at the time of writing.

Bitfinex analysts shared with Bitcoin Magazine that the Fed’s unexpectedly hawkish tone surprised markets, causing a price reversal and kept risk appetites in check.

The Fed’s updated “dot plot” shows little consensus for more than a single 25-basis-point cut in 2026, with stronger growth forecasts and shifting tax policy limiting near-term easing.

Timot Lamarre, director of market research at Unchained, wrote to Bitcoin Magazine that “ There is so much to be bullish about in the bitcoin space – from Square facilitating bitcoin payments to large institutions like Vanguard now allowing their clients access to bitcoin ETFs to quantitative tightening coming to an end.”

Lamarre said that bitcoin’s recent price movements show a gap between growing adoption and the price increase that usually comes with higher demand.

Bitcoin price decline and broader market pullback

Bitcoin price’s recent pullback also reflects broader market concerns. Technology stocks, including Oracle, suffered after disappointing earnings and warnings about slower-than-expected AI-related profits.

Oracle shares fell 11% in after-hours trading following revenue and profit forecasts below analysts’ expectations.

The Fed’s outlook for 2026 suggests only one additional rate cut, fewer than markets had anticipated. Asian stock markets declined, and U.S. equity futures pointed lower, while European trading remained subdued.

Standard Chartered recently revised its year-end Bitcoin forecast, lowering its target from $200,000 to $100,000, citing a slowdown in corporate treasury buying and reliance on ETF inflows to support future price gains.

Bernstein analysts recently said that they see a structural shift in Bitcoin’s market cycle, meaning that the traditional four-year pattern has broken. They forecast an elongated bull cycle driven by steady institutional buying, which offsets retail selling, and minimal ETF outflows.

The bank raised its 2026 price target to $150,000 and expects the cycle to peak near $200,000 in 2027, maintaining a long-term 2033 target of roughly $1 million per BTC.

Meanwhile, JPMorgan remains bullish over the next year, projecting a gold-linked, volatility-adjusted Bitcoin target of $170,000 within six to twelve months, factoring in market fluctuations and mining costs.

Analysts say Bitcoin’s decline after the Fed announcement reflects a “sell the fact” dynamic. “The market had fully priced in the cut ahead of time,” said Tim Sun, senior researcher at HashKey Group. “Concerns over political and economic developments in 2026, combined with potential inflation from AI-driven capital expenditure, are weighing on risk sentiment.”

Last week, Bitcoin price saw a volatile ride, dipping to $84,000 before bulls pushed it up to $94,000, then dropping slightly below $88,000, and closing the week at $90,429.

The market now faces key support at $87,200 and $84,000, with deeper support zones around $72,000–$68,000 and $57,700.

Resistance levels stand at $94,000, $101,000, $104,000, and a thick zone between $107,000–$110,000, with momentum likely slowing above $96,000.

Typically, rate cuts lead to bullish momentum, but the market may have already priced in this month’s rate cut. The bitcoin price has fallen roughly 28% since its October all-time high.

At the time of publishing, the bitcoin price is at $90,114.

Just weeks after announcing a stablecoin, Swedish fintech giant Klarna is taking another step into crypto. The company has teamed up with Privy, a wallet infrastructure platform owned by Stripe, to explore digital asset solutions for its users.

The partnership will focus on research and development of crypto wallet features, the company said. The two aim to make it easier for everyday users to store, use, and send digital assets. The move builds on the company’s recent launch of KlarnaUSD, a U.S. dollar-backed stablecoin issued on the Tempo blockchain.

“Millions already trust Klarna to manage everyday spending, saving, and shopping,” said Sebastian Siemiatkowski, CEO and co-founder. “That puts us in a unique position to bring crypto into the financial lives of normal people, not just early adopters. With Privy, we plan to build products that feel as intuitive as any other Klarna feature.”

KlarnaUSD was launched with Tempo and Bridge, a Stripe-backed stablecoin infrastructure provider.

The token is live on Tempo’s testnet and expected to launch on mainnet in 2026. The fintech giant said the stablecoin could reduce global cross-border payment costs, currently estimated at $120 billion annually.

JUST IN: Fintech giant Klarna to develop #Bitcoin and crypto wallet features within its financial products.

Privy powers over 100 million accounts for more than 1,500 developers. The platform supports crypto-native applications like OpenSea and Hyperliquid.

Henri Stern, CEO and co-founder of Privy, said the partnership will allow users to hold a wide variety of digital assets, trade safely, and transact with friends anywhere in the world.

“We’re proud to partner with world-class fintechs like Klarna, providing the secure, enterprise-ready infrastructure they need,” Stern said. “Privy aims to be the backbone for any business that wants to harness the exciting capabilities crypto and stablecoins offer.”

The initiative reflects a growing trend. Traditional fintechs are now testing ways to integrate crypto tools into everyday consumer finance. The company said any future wallet or crypto product would require the necessary regulatory approvals before launch.

Venture capital firm a16z estimates that 716 million people globally hold cryptocurrencies. Between 40 million and 70 million transact with crypto each month. That figure grows by roughly 10 million users a year.

Klarna’s push into crypto marks a sharp turn for the company. CEO Siemiatkowski was once a vocal skeptic of digital currencies.

He said the market’s maturity and Klarna’s global reach now justify this entry. Klarna serves 114 million customers and processes $112 billion in annual gross merchandise volume.

The company plans to explore further crypto initiatives. A blog post on Thursday hinted at a new announcement “in a week or so,” suggesting more developments are coming soon.

Satsuma Technology (LSE: SATS) sold nearly half its bitcoin treasury and announced major board changes as it prepares for a planned uplisting to the London Stock Exchange’s main market.

The U.K.-based company sold 579 BTC out of its 1,199 BTC holdings, raising about £40 million ($53 million) in net proceeds, according to a Thursday announcement. The move leaves Satsuma with 620 BTC and roughly £90 million in cash.

The sale is designed to ensure the company has enough liquidity to repay £78 million in convertible loan notes due on Dec. 31, 2025.

Some noteholders have not yet committed to converting their debt into equity once Satsuma publishes its prospectus for the uplisting. The company said it wants to hold sufficient cash in case those conversions do not occur.

Alongside the treasury move, Satsuma proposed appointing Ranald McGregor-Smith as Chair and Clive Carver as Senior Independent Director. Both would join upon completion of the uplisting.

McGregor-Smith spent his career advising FTSE100 and FTSE250 firms and co-founded corporate broker Whitman Howard. He also sits on the board of Sabien Technology Group. Carver, a chartered accountant, has chaired and served as a non-executive director at several listed companies over the past decade and will also chair Satsuma’s Audit Committee.

Current Chair Matt Lodge will step down after the uplisting but remain on the board. Non-executive director Darcy Taylor resigned immediately as part of the restructuring.

CEO Henry K. Elder said the board changes bring stronger PLC governance at a key transition point. He also said the bitcoin sale positions the company for “stability and growth” as it advances its broader strategy.

Satsuma shares edged up to 1.05 pence following the announcement. The stock remains down nearly 30% over the past month.After the sale, Satsuma ranks as the 61st largest publicly traded bitcoin holder.

The report, covering 100+ companies, shows large treasuries like Strategy and Strive dominated net purchases, while early signs of selling emerged, led by Sequans.

Quarterly accumulation slowed but remains steady, with Q4 2025 on track for ~40,000 BTC added. Mining companies now hold 12% of corporate BTC.

Public and private treasuries bought over 12,644 BTC in November, bringing total holdings past 4 million BTC. Global diversification and disciplined buying continue despite volatility.

Corporate Bitcoin treasuries faced mark-to-market losses in November, according to an exclusive Corporate Adoption Report from Bitcoin Treasuries.

The report, covering more than 100 companies, offers a systematic look at how last month’s price drop affected public company holdings.

Bitcoin briefly fell below $90,000 in late November. The decline pushed many 2025 buyers into the red. Of the 100 companies for which cost basis is measurable, about two-thirds now sit on unrealized losses at current prices, per the report.

Despite the volatility, large balance sheets continued to dominate net Bitcoin buying. Strategy, Strive, and a small cohort of high-conviction buyers accounted for most net additions.

Public Bitcoin treasury equities remain weak versus BTC and broad indices. Still, a minority of companies delivered at least 10% gains over the past 6–12 months.

Early signs of corporate Bitcoin selling also emerged. At least five companies reduced BTC exposure in November. Sequans led the group, selling roughly one-third of its holdings. While small in aggregate, these moves suggest some management teams are willing to crystallize losses or de-risk when volatility spikes.

Quarterly Bitcoin accumulation is slowing, but not collapsing. Q4 2025 is on track for roughly 40,000 BTC in net additions to public company balance sheets. This is below the last four quarters but broadly in line with Q3 2024, as companies normalize to a slower, more selective accumulation pace.

In November, public and private treasuries purchased, added, or disclosed over 12,644 BTC in November and the total BTC held across all tracked entities surpassed 4 million by month’s end.

Bitcoin purchases

Big treasuries know for their bitcoin buying continue to dominate purchases. Strategy added 9,062 BTC across three transactions in November, per the report.

Its largest buy, 8,178 BTC, came on Nov. 17. Strategy ended the month with 649,870 BTC, worth about $59 billion. Currently, the company has 660,624 after some December purchases.

Strive added 1,567 BTC at an average price of $103,315 per BTC in November. The purchase brought its month-end holdings to 7,525 BTC, or $684 million. The company funds its Bitcoin strategy primarily through perpetual preferred equity.

Mining companies remain significant players. Cango and Riot added 508 BTC and 37 BTC, respectively, from mining operations. American Bitcoin added 139 BTC through combined purchase and mining strategies.

Per the report, mining companies now account for 12% of public company BTC holdings.

Bitcoin selling and rebalancing

Sales were limited but notable. As mentioned earlier, Sequans sold nearly one-third of its holdings, to reduce convertible debt. Hut 8 reduced holdings by 389 BTC. KindlyMD and Genius Group also trimmed exposure.

Some companies added small amounts even amid the downturn. DDC Enterprise Limited picked up 100 BTC during the pullback.

Metaplanet continued “additional purchase” filings on the Tokyo exchange. ETF flows returned to net inflows after a month of redemptions.

The data suggests a barbell pattern: small distressed sellers versus programmatic buyers and disciplined treasuries. Investors see BTC increasingly used as collateral or for cash flow, rather than just as a speculative asset.

Global trends and future outlook

Corporate Bitcoin holdings are increasingly global. U.S. companies dominate the top 20, but Japan, China, Europe, and other regions are growing.

Non-U.S. public company holdings rose 3,180 BTC from two months prior, now representing about 9% of all public company BTC. Analysts say this geographic diversification reduces regulatory risk.

Despite November’s volatility, corporate adoption of Bitcoin continues. Large treasuries are still buying aggressively. The quarterly pace of accumulation is slower than earlier in 2025, the report noted, but steady growth persists.

Those interested in reading the full report can do so below:

This piece is featured in the print edition of Bitcoin Magazine, The Freedom Issue. We’re sharing it here as a sample of the ideas explored throughout the full issue.

On November 3, 2025, the freedom for developers to build financial privacy software is on trial.

Samourai Wallet was a Bitcoin privacy wallet developed by Keonne Rodriguez and William Lonergan Hill. It included specialized privacy tools that mixed the coins of wallet users in ways that required no third-party custody. The service’s servers helped coordinate “mixing” — methods to conceal the origin of coins and offer users some degree of forward privacy.

Rodriguez and Hill were arrested on April 24, 2024, on two charges: conspiracy to operate an unlicensed money transmitting business and conspiracy to commit money laundering.

The U.S. Department of Justice (DoJ) accused the Samurai Wallet developers of facilitating over $2 billion in unlawful transactions through their cryptocurrency mixing service between 2015 and February 2024. Additionally, the DoJ alleges that the developers helped launder more than $100 million in criminal proceeds from illegal dark web markets, such as Silk Road and Hydra Market, as well as other hacking and fraud schemes.

The case of United States v. Rodriguez and Hill threatens the established precedents of code as speech on two major fronts.

The first regards the “$2 billion in unlawful transactions” accusation. The prosecution implies that software that aids or facilitates the movement of money in any way is indistinguishable from money transmission and that it requires a money transmitter license, even if that software never holds custody of user funds. This is entirely at odds with the dynamic that had previously been established by FinCEN’s 2019 guidance and other legacy financial regulations.

The second implication is that software that defends the privacy of communications or transfer of value is not protected speech under the United States’ First Amendment.

Code is Speech

The United States has a long and unique tradition of defending freedom of speech.

Over the years, many court cases have reinforced these values, creating precedents that let developers create great software and share it online. That kind of software has made the United States the technological epicenter of the world, from AI to cryptographic finance; the freedom to build software today is critical to the economic success of the nation.

Texas v. Johnson (1989), for example, established that burning the U.S. flag in protest was indeed protected speech even though the “speech” in this case was “functional”, i.e., expressed in the destruction of the flag.

In the 1990s, with the rise of the internet, landmark cases like Bernstein v. United States (1996-1999) established that discussions about cryptography — specifically the sharing of source code involving cryptographic algorithms — was not a “munition” governed and regulated by the Arms Export Control Act and the International Traffic in Arms Regulations. On the contrary, the publication of source code explaining how cryptography worked was expressive speech and thus fully protected under the First Amendment.

The Bernstein case marked a critical victory for the Cypherpunks of the ’90s, whose contributions to open source software laid the foundations for Bitcoin: Many of the technologies that Satoshi Nakamoto used in its construction were indeed invented in the internet forums of the time. It was there that the Cypherpunks discussed the application of cryptography to the defense of freedom of speech, digital privacy, and civil rights.

In the Universal City Studios v. Corley (2001) case, however, something shifted slightly. Jon Lech Johansen, a Norwegian teenager, wrote software that jail-broke copyrighted movies from software locks placed there by Universal Studios, making movies playable in Linux systems. Eric Corley, a U.S. journalist, published the software online, which led to a massive lawsuit spearheaded by Universal Studios.

This landmark case turned on the question of whether something is speech or conduct in the realm of software. It established that when speech in the form of software gained “function”, such as the breaking of a DVD encryption lock, it suddenly became a tool and could become subject to regulation.

While Corley’s free speech protections were eventually reaffirmed in the Second Circuit Court of Appeals, the distinction between source code publications as a form of expression and functional software as a tool that can be regulated was established.

Despite the rulings — Corley even removed the copy of the DeCSS piracy software from his website — the damage was done. Internet civil disobedience spread the software far and wide, and the piracy wars of the 2000s raged on for years. They demonstrated not just the limits of free speech protections but also the limits of trying to enforce digital censorship.

Information simply wants to be free.

The Samourai case could face a similar challenge, and it is unclear whether “code is speech” can be a sufficient defense for Rodriguez and Hill.

Chink in the Armor

A controversial project that created as many loyal superusers as it did haters and critics is now on the front lines of the Biden-era lawfare, and the principle that code is speech appears to be at stake once again.

As a result, it has forced critics — myself included — to rise to the defense of a wallet that, while quite successful in its adoption, made many design choices that were questionable and for which they may be judged harshly in the coming months.

One potential weak point in their defense is their alleged enabling of sanctioned parties to “launder money” through their coin-mixing service. The U.S. Attorney’s Office for the Southern District of New York (SDNY) went as far as to embed a screenshot of the Samourai wallet account welcoming sanctioned oligarchs:

Coin mixers are akin to the virtual private networks (VPNs) used by law-abiding citizens and criminals alike. For privacy to exist, one must be able to hide in a crowd, their choices and personal information shielded from prying eyes, and to be revealed or judged after due process.

With that, the Samourai Wallet founders did not make themselves a difficult target. If the allegations by the prosecution are true, and they knowingly helped dress up wolves in sheep’s clothing, then they likely will have to pay a price for violating sanctions doctrines. A deeply chilling legal precedent could then be set, shaping the future of digital finance and directly harming the proliferation of such technology in the United States.

However, there may be hope in the change to a more crypto-friendly administration under the leadership of President Trump.

“I Will Defend Your Right to Self Custody” – Trump

During his keynote speech at the Bitcoin Conference in Nashville in 2024, Trump made a promise, one that he still has the opportunity to keep.

He promised to “defend the right to self custody”.

Without financial privacy, self custody is dramatically weakened, as seen by the growing wave of physical attacks on Bitcoiners in recent years. The liberty previously enjoyed by software developers to build self-custodial Bitcoin tools like Samourai Wallet, is on trial.

The chilling effect